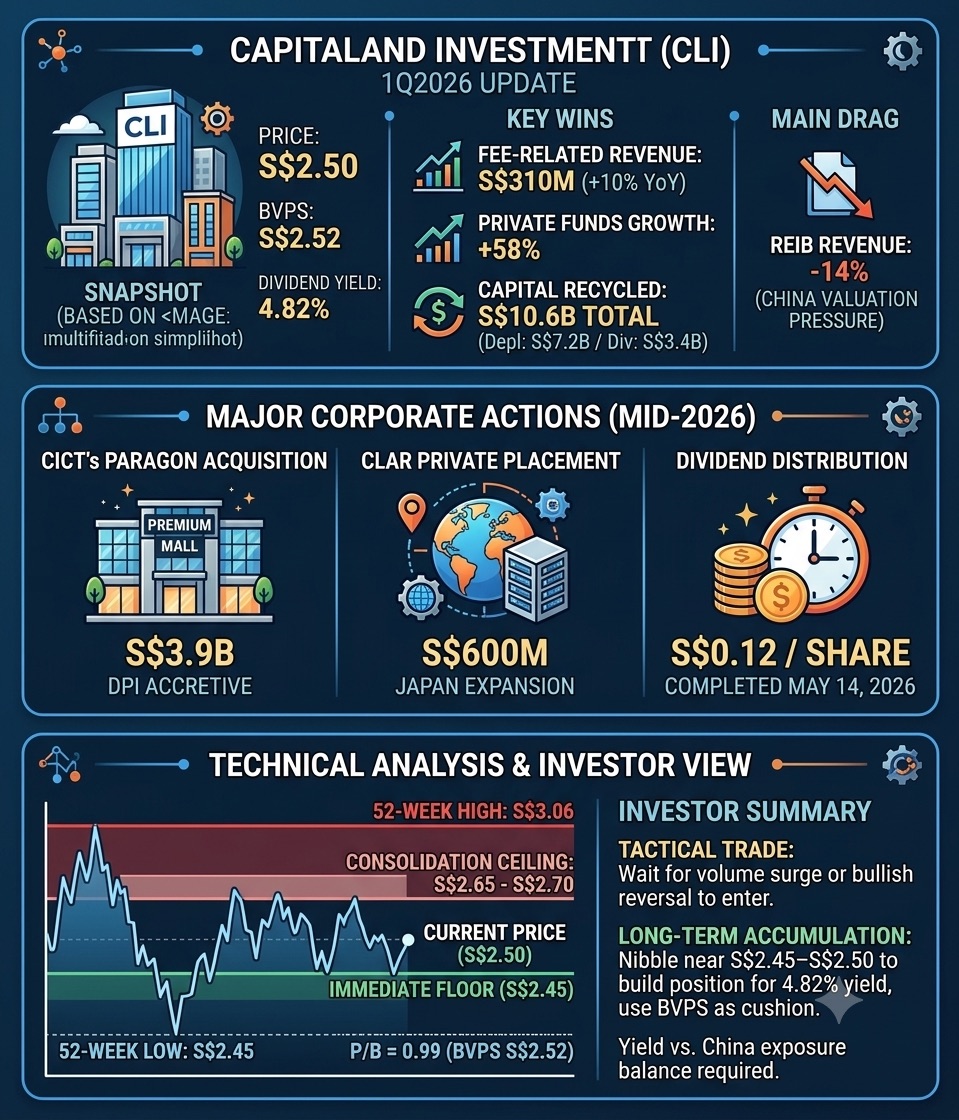

$CapitaLandInvest(9CI.SG)

I have been tracking CapitaLand Investment (CLI) closely since its peak at 3.17 on 10 Feb 2026, it has been trending downward. Quite disappointing. I am still waiting patiently for the right time to enter. 🤭

If you follow Singapore markets, “old bird”, you will know that CLI is a genuine blue‑chip giant backed by Temasek.

Looking at its latest 1Q2026 results, the shift to an asset‑light model is clearly delivering results:

🟢 Fee‑Related Revenue rose 10% YoY to S$310 million, driven by a 58% jump in private funds under management.

🟢 Active capital recycling: invested S$7.2 billion into high‑growth areas while divesting S$3.4 billion of assets.

🟢 The main drag remains its Real Estate Investment Business, down 14% due to valuation pressure in China.

Major moves are also underway: CICT’s S$3.9 billion acquisition of Paragon mall and CLAR’s S$600 million expansion into Japan.

Why I am seriously considering buying now?

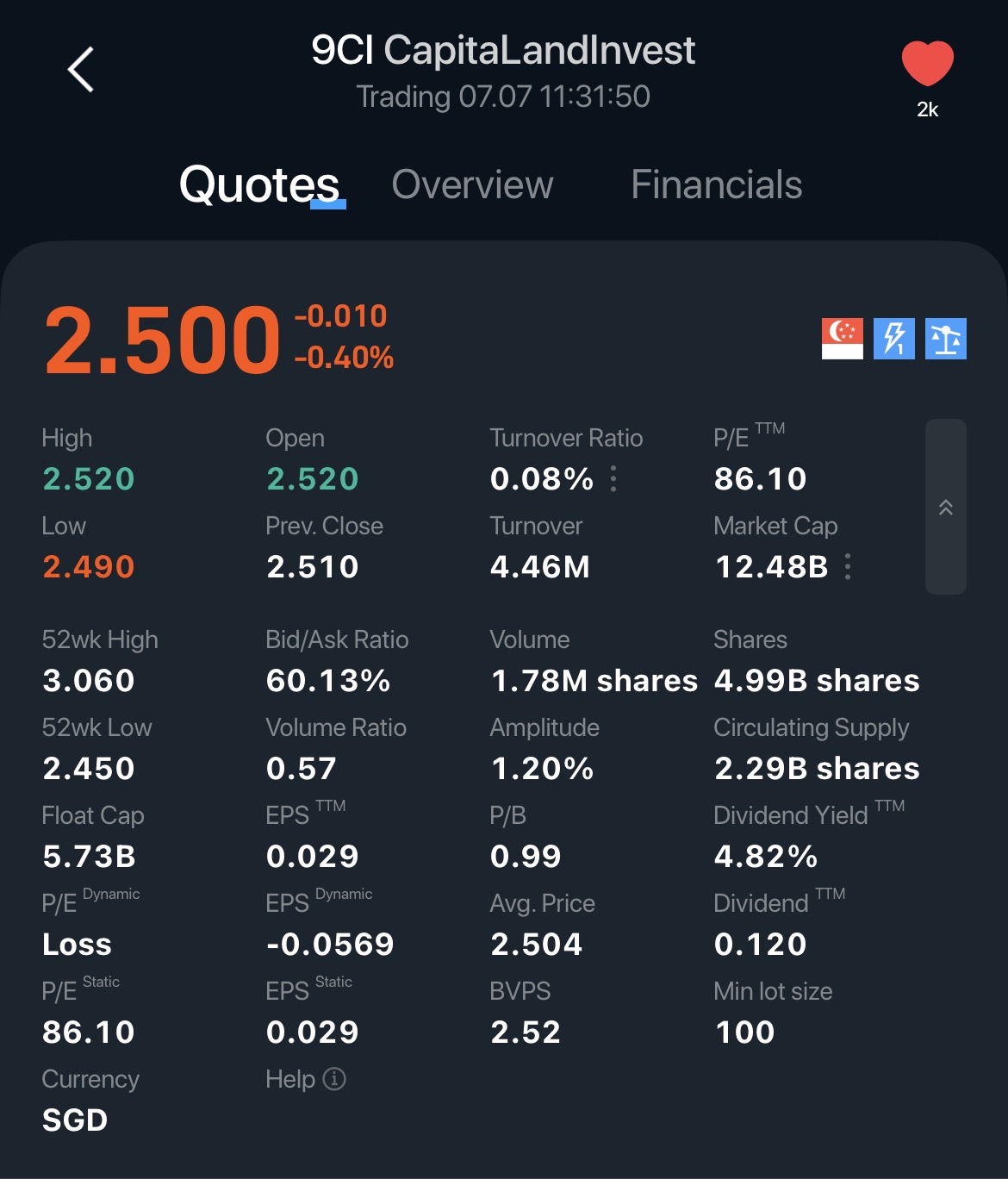

Technically, CLI is holding firm right at S$2.45–2.50 .

It is almost exactly matching its book value per share of S$2.52. Trading at P/B 0.99, the market has stripped away all premium for its underlying growth.

On top of that, the 4.82% dividend yield offers solid support while you wait for conditions to improve.

For short‑term trades, I do like to see strong volume to confirm a trend reversal.

But for long‑term accumulation, buying near book value looks like a very attractive setup with favourable risk‑reward.

Watch out for the 1st half result announcement on Thursday 13 August 2026.

What is your view on CLI around S$2.50? 👇

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.