SpaceX Joins the Nasdaq-100 on July 7 — Can $4.3B in Forced Buying Save the Slide?

Recently, if you've been watching $SpaceX (SPCX.US), you're probably a little confused: the stock has been sliding for almost a month. On June 16 it hit an all-time high of $225.64, and now it's down to just $162 — a 28% drop.

Against that backdrop of a relentless slide, something big happens on July 7: SpaceX will officially be added to the Nasdaq-100 Index. In theory this should be bullish for the stock, but how the mechanism actually works is something most people have never really understood. I've broken it down into five questions and will walk through them one by one.

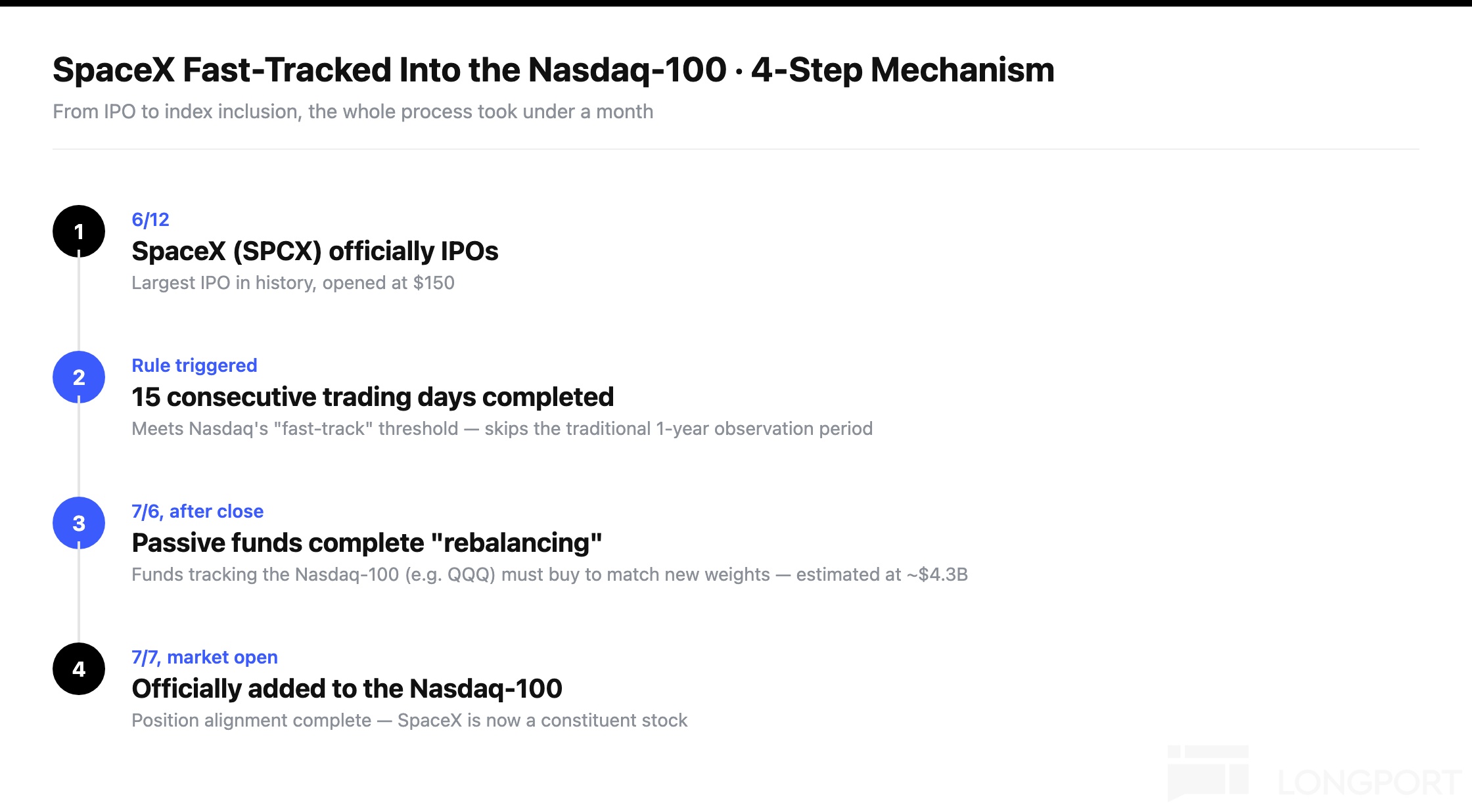

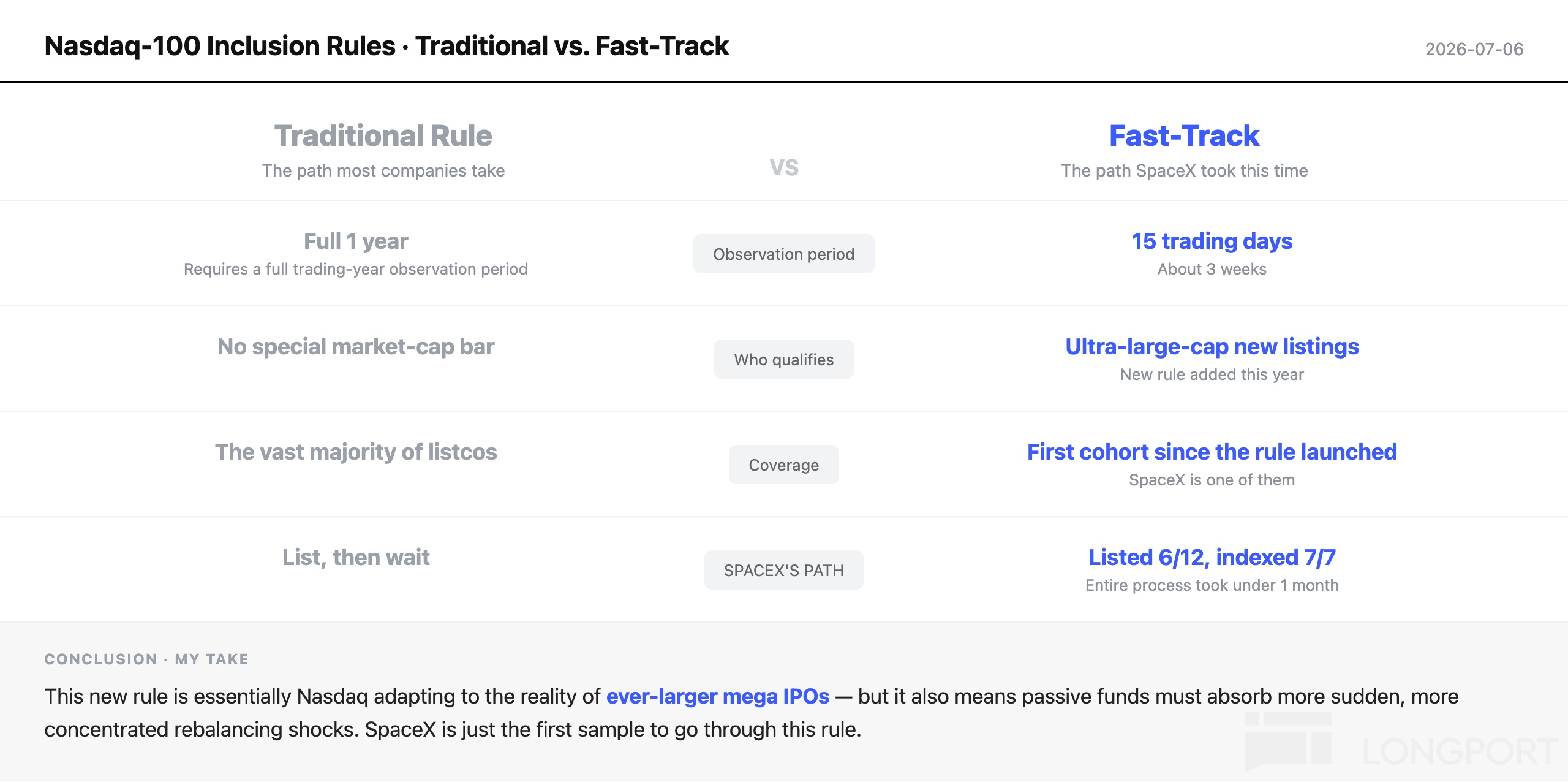

Question 1: What are the rules for fast-track inclusion?

For a company to be added to the Nasdaq-100 under normal circumstances, it typically needs to have been listed for about 3 months and wait for a quarterly/annual rebalancing window. SpaceX only needed 15 trading days — thanks to a new rule Nasdaq introduced this year: an extremely large-cap new listing only needs to trade for 15 consecutive trading days to qualify for early "fast-track" inclusion, without waiting a full year. SpaceX is among the first companies to benefit from this new rule since it was introduced.

Question 2: Who's actually doing this triggered passive buying?

This "buying" isn't some fund manager subjectively deciding "I think SpaceX is worth buying" — it's mechanical buying mandated by the rules. Every passive fund tracking the Nasdaq-100 — the most familiar example being ETFs like QQQ — must strictly hold positions matching the index's latest constituents and weights. Once SpaceX is added to the index, these funds are required to buy the corresponding proportion of SpaceX shares. Not buying means "tracking error," which they'd be held accountable for — so they have no choice in the matter.

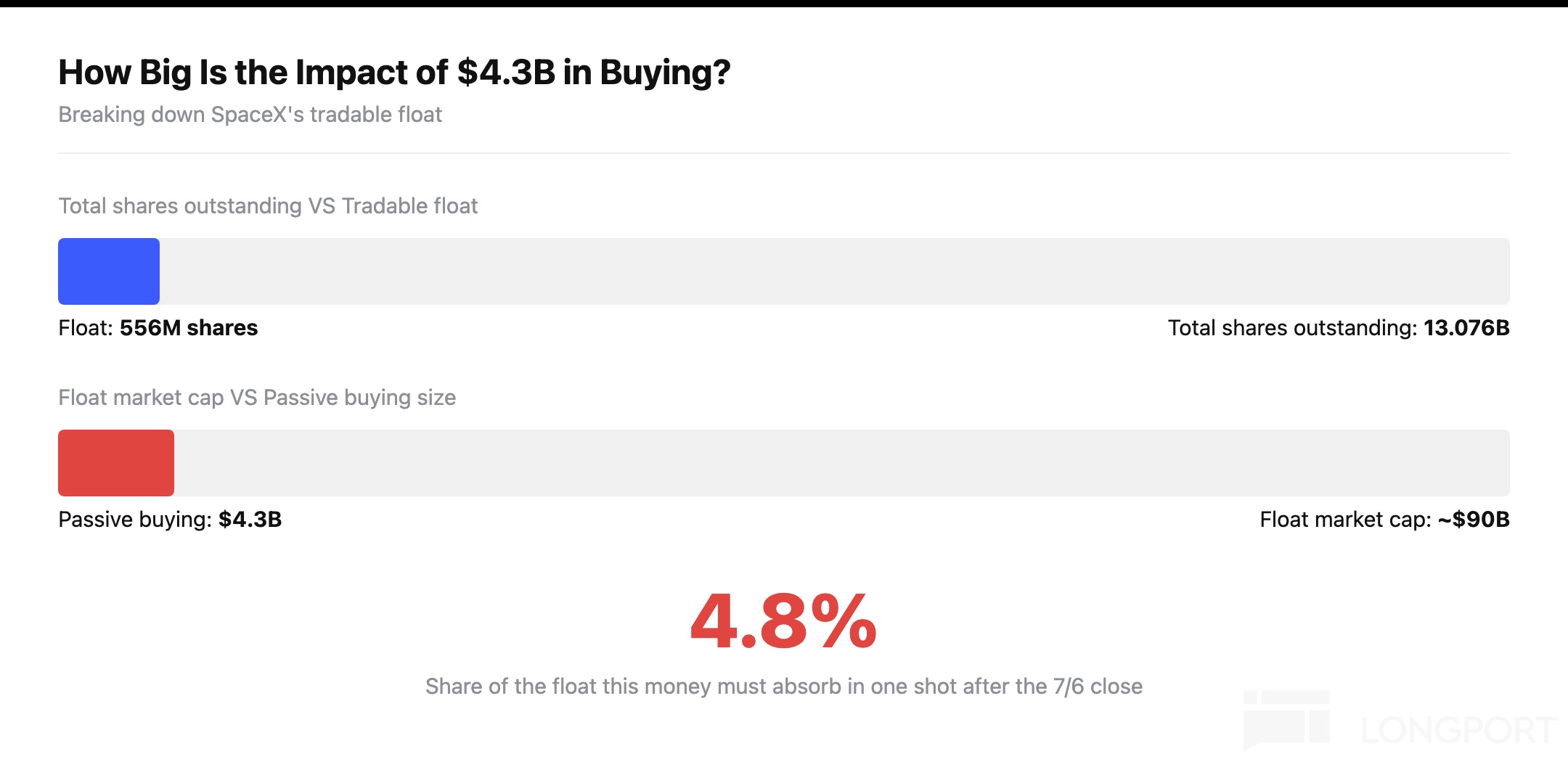

Question 3: How big is this relative to SpaceX's tradable float?

JPMorgan estimates that these passive funds will collectively buy about $4.3 billion worth of SpaceX stock — and that's just the money tracking the Nasdaq-100, not counting funds tracking other indices. That number sounds large, but what matters more is its size relative to SpaceX's "tradable float." I looked into it: although SpaceX has over 13 billion shares outstanding, the vast majority are locked up by Musk and early shareholders — the actual free float available for trading in the market is only about 556 million shares (under 4.3% of total shares outstanding). At the current price of $162, that's a free-float market cap of roughly $90 billion. $4.3 billion divided by $90 billion works out to about 4.8% of the float — in other words, this passive buying needs to absorb nearly 5% of the entire free float in a very short window. That's not a small proportion — it's real money that will make waves.

Question 4: Roughly when does this happen?

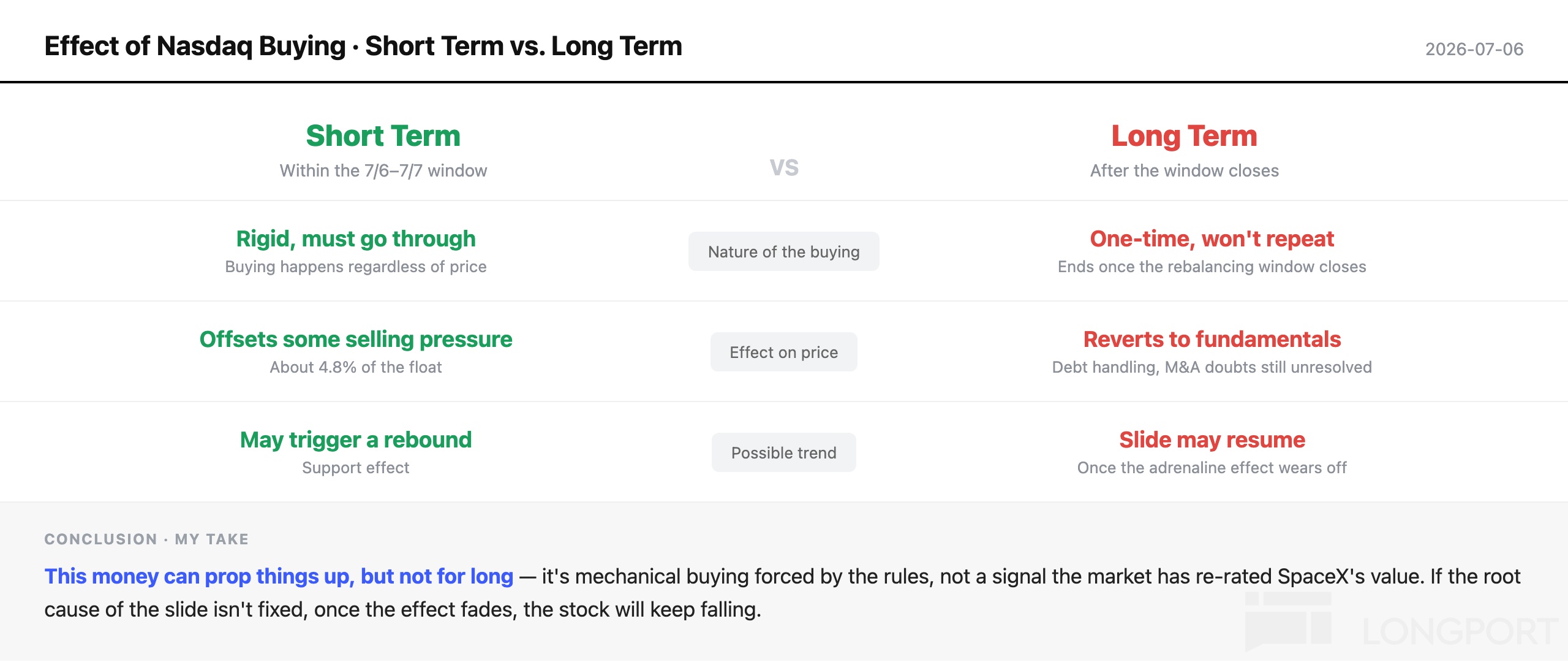

This buying isn't spread out gradually over several days — it's a highly concentrated, one-time event. Per standard index-rebalancing convention, funds complete their "rebalancing" at the close of the trading day before the effective date — that is, after the close on July 6, fund managers have to get their positions aligned at the last minute, to make sure that by the open on July 7 their holdings fully match the new index weights.

Question 5: What might this mean for the stock price?

Put simply, this money is more like a shot of adrenaline — in the short term it can genuinely provide real, concentrated support for the stock, and might even drive a rebound, because it's rigid buying that has to happen regardless of price, with nothing to do with sentiment or fundamentals. But adrenaline is never long-term nourishment. It doesn't solve SpaceX's own problems (like how it's handling its debt and the high-priced acquisitions that have raised market doubts). Once this one-time buying is absorbed, the stock will go back to trading on fundamentals.

Back to the opening question:

Can this $4.3 billion save SpaceX from its relentless slide? My take: it can prop things up for a moment, but not forever.

To put it bluntly: this money isn't "the market falling in love with SpaceX" — it's the rules holding a knife to funds' throats, forcing them to buy. In the window from July 6 to July 7, it really can force the stock price up, even faking out a decent-looking rebound candle that convinces a lot of people they "bought the dip successfully." But once the adrenaline wears off, none of the underlying problems have gone away: the debt is still owed, the doubts about the high-priced share issuance are still unaddressed. If you're getting in for this "index-inclusion bonus," temper your expectations — it's more like force-feeding fever medication to someone running a high fever: the thermometer reading looks better, but the underlying illness is still in the body. The day the relentless slide actually stops for good won't be thanks to a $4.3 billion adrenaline shot — it'll be because SpaceX itself delivers answers that actually reassure the market.

$SpaceX(SPCX.US)

$Rocket Lab(RKLB.US)

$Tema Space Innovators ETF(NASA.US)

$Procure Space ETF(UFO.US)

$AST SpaceMobile(ASTS.US)

$Redwire(RDW.US)

$ LEVERAGE SHARES 2X SHORT SPCX DAILY ETF(SSPC.US)

$2 倍做多SpaceX ETF(SPCH.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.