Has the heavyweight competition taken turns to hit, leaving Disney with a hundred-year history unable to withstand it?

Hello everyone, I'm Dolphin Analyst!

On November 8th, US Eastern Time, Disney released its Q4 FY2022 (Q3 2022) earnings report after the U.S. stock market closed. As the last quarter of this fiscal year, Disney unexpectedly ended the year on a sour note. Based on the storyline of the first three quarters:

(1) The epidemic suppressed the industry for too long. Despite the rising prices of goods and loan costs, the demand for offline travel remained strong due to a decent job market and increasing wages. Even optional consumption services such as theme parks were not immune to this trend.

(2) Streaming media services are fighting a content war for users, burning through money and reaching a new high of losses.

(3) In summary, the traditional theme park business has made a comeback with the "plus" sign, covering losses in streaming media, declining cable television and content distribution, which was deliberately reduced for Disney+ exclusives, creating a new revenue structure and profit structure.

However, the risk lies in when the content cost continues to rise, will the "theme park fever" slow down? When will the streaming media losses be repaired? The turning points on both sides are opposite. Once the balance is broken, the profit that investors care about the most during a bear market may not be sustainable.

In Disney's final earnings report, it seems to be approaching the above risks. Although management has stated that the turning point for streaming media losses has arrived and will become profitable in 2024 as planned. Dolphin Analyst is worried that in order to ensure the exclusive content of streaming media, the revenue of traditional businesses will shrink first, leading to the continuation of low profits. It's also a mystery how long the theme park fever can last after the price increase. In the short term, only one "content cycle" can bring some anticipation to the market.

Returning to this season's financial report, the key points are as follows:

1. Total revenue is RMB 20.1 billion, with a YoY growth rate of 8.7%, a significant drop in double-digits compared to the consensus expectation of RMB 21.3 billion. With the exception of theme park operations, traditional businesses, including streaming media services, did not perform as well as expected based on the latest expectations of core investment banks.

Looking ahead to 1Q23FY, there's no need to be particularly pessimistic. On the one hand, there are movies like "Black Panther 2" and "Avatar 2" that have received good reviews scheduled for release. On the other hand, streaming media services may be improved through price increases and advertising subscription packages. At the same time, although there was a price increase in October and the impact of hurricanes, the demand for theme parks is still strong based on visitor numbers.

2. The main bright spot for streaming media subscriptions is that net additions of users exceeded expectations. Disney+ added 12.1 million new users this quarter, 2 million more than the market expected. ESPN+ and Hulu also did well despite their price increases.

The revenue performance of streaming media this quarter was poor, mainly due to weak advertising and more users opting for high-cost-effective bundled packages. However, from a strategic perspective, management will focus more on monetizing streaming media starting next quarter. The price increase (Disney+ will have a price increase in December), and advertising supported packages are all means to generate higher revenue and profitability. Management has promised that the goal of making the streaming media business profitable by 2024 remains unchanged. 3. Film and Television Content Business: Despite the success of Marvel movies like "Thor 4", the company has significantly reduced its content authorization to prioritize Disney+. In addition, some new movies will only be available on Disney+ or have faster online releases, which affects potential cinema box office and home television revenue. This ultimately resulted in revenue of 1.74 billion this quarter, a 15% year-on-year decline, which is significantly lower than the market's expected revenue of 2.06 billion.

4. Theme Park Business is Relatively Stable: Although the growth rate has slowed significantly, the base last year was not low, and this year was also affected by Hurricane "Ian". "Orlando Park" was closed for two days, and the management stated that the impact of Ian on the third-quarter profit was 65 million, accounting for about 4% of the current profit.

Looking ahead to 1Q23FY, there are many holidays, and although Hurricane "Nicholas" began to land in Florida in early November and is expected to affect the theme park business, since October 11, when park tickets and service products were raised by about 10% across the board, there seems to be no sign of weakening demand from the visitor entry tracking Deutsche Bank. Overall visitor entry data this year is better than 2019 before the outbreak.

In terms of international parks, the situation at Paris Disneyland is improving and recovering, offsetting some of the losses from Shanghai Disneyland.

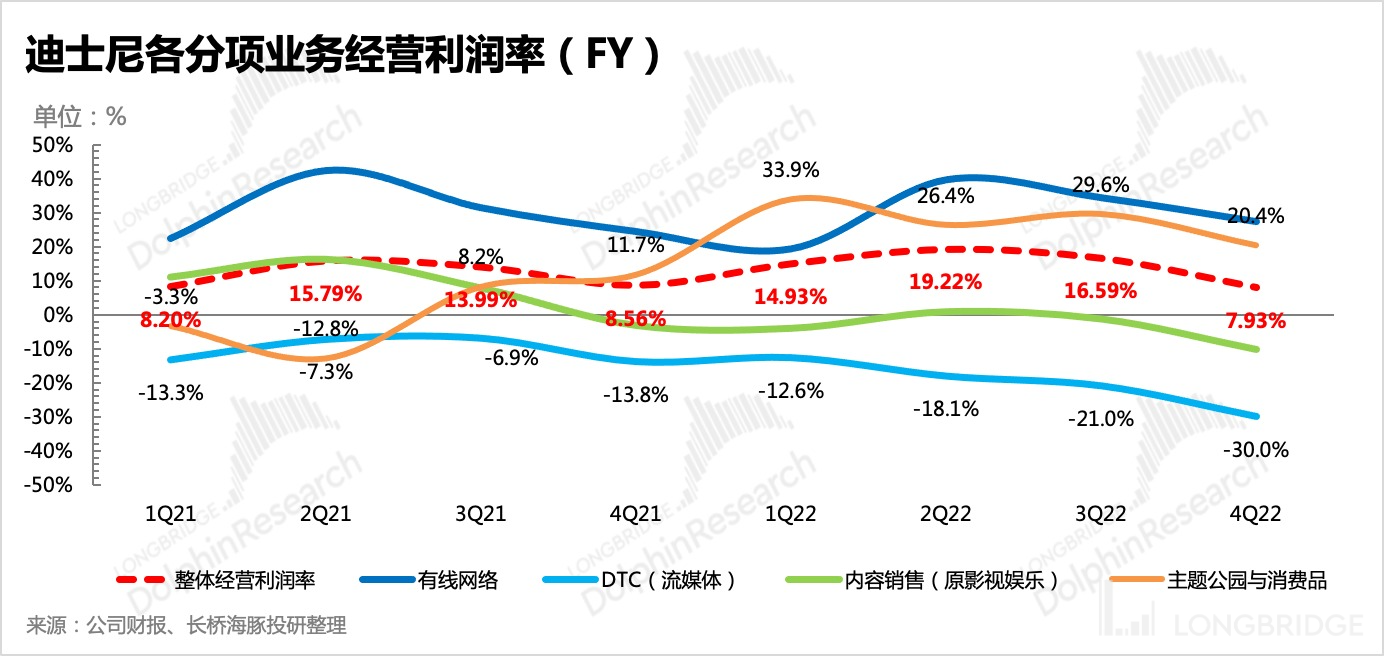

5. Profit was Crazy Cut by Content Costs: The operating profit for this quarter was 1.6 billion, which is basically unchanged from the same period last year, significantly weaker than the market's expected 2.05 billion. Apart from the soaring inflation and customer acquisition costs at theme parks, other businesses were mainly dragged down by high content costs. As blockbuster films launched successively on Disney+ this year, the streaming media loss has reached a new high, and the operating loss rate has reached 30%. However, the management stated that the turning point of streaming media losses has arrived, indicating that losses in the next quarter will improve.

6. The Seasonal "Overestimation" of Free Cash Flow: The free cash flow this quarter was a net inflow of 1.376 billion, mainly contributed by a net inflow of operating cash flow of 2.52 billion, which increased significantly compared to the previous quarter despite the compressed profits mainly due to an increase of nearly 1 billion in payables this quarter, whereas in the previous quarter it had decreased.

Looking back at history, such a period of overestimation occurs every fourth quarter, which may be related to the payment rhythm between suppliers, and cannot be simply regarded as a significant improvement in cash flow. Compared with the same period last year, free cash flow decreased by 10%.

As of October, the company had cash of 11.6 billion, which is considered sufficient.

Dolphin Analyst will share the call summary with the Dolphin user group through the Longbridge App. Interested users are welcome to add the WeChat account "dolphinR123" to join the Dolphin Research Group and get the call summary for the first time. Dolphin's Perspective

Disney's fourth quarter performance had only one highlight, "streaming media user growth far exceeded expectations." Compared to the strong performance of profitability exceeding expectations in the previous three quarters, the sacrifices made to traditional content businesses in order to maintain the growth of streaming media users in the fourth quarter were quite significant.

This makes us start to pay attention to whether the market has overestimated the contribution of Disney's content cycle to the final overall performance. Management also anticipated this unhealthy growth path, and began to focus on revenue and profits in the conference call, rather than just user metrics.

Relatively speaking, Dolphin Analyst is slightly more relieved by the theme park business. Although the revenue for this quarter did not meet expectations, it basically met the expectations of the core investment bank. From a normal year before the epidemic, the second and fourth quarters are not the peak season. The rising demand for consumer goods and the accelerated growth rate are not too surprising. Looking at the two businesses collectively, the year-on-year growth in the fourth quarter continued to reach historical highs in absolute value.

However, the company hopes to pass on the inflationary pressure to consumers. On October 11, the prices of three-year tickets at Disney parks in the United States that had remained the same began to rise, with an average increase of about 10%, and from the current customer traffic, there has been no resistance from consumers.

But if the high interest rate environment continues, companies will compromise and lay off employees one after another, and consumers' disposable income expectations will weaken, then the priority demand to be cut will also be for optional consumption such as entertainment. Therefore, for the strong theme park business this year, it is afraid that it will inevitably fall into a state of growth weakness. And this is also where the market may be too optimistic.

Therefore, from a macro perspective, there may be a turning point for Disney's overall performance in the future, but the arrival of the content cycle seems to give the company some risk resistance. Dolphin Analyst believes that the first quarter of the future 2023 fiscal year (4Q22CY) is probably the peak season of this round of content cycles. Afterwards, under the pressure of a high base and the macro economy, there will be a turning point for Disney's performance, but the profit turning point of streaming media may have to wait until the end of 2024. The change in revenue structure will cause the profit margin to go through an awkward period of slump.

Detailed interpretation of this quarter's financial report

I. Understanding Disney

As a kingdom of entertainment for nearly a hundred years, Disney's business structure has also undergone multiple adjustments. Dolphin Analyst has given a detailed introduction in "Disney: The "Beauty Secret" of a Hundred-Year-Old Princess". Here is the latest business structure situation, which is convenient for investors to read the financial report preliminarily.

(1) Disney's business structure mainly includes four parts: film and entertainment, cable television, streaming media, theme parks and merchandise retail.

(2) [Theme Parks and Merchandise Retail] have developed maturely over the years, with the first IP inventory support, Disney's theme park business has a leading position that is more affected by overall consumption. Under normal circumstances, it can be regarded as a stable cash flow. (3) [Film and Entertainment], [Cable TV], and [Streaming Media] essentially produce and distribute Disney films, so income changes are mainly related to Disney's film schedules and overall film market consumption.

Source: Disney Financial Report, Dolphin Research and Analysis

Two

Income: Significantly Lower Than Expected, Can Price Increases Save Next Season?

This quarter, Disney achieved a total revenue of 20.2 billion U.S. dollars, a year-on-year increase of a steep drop to 8.7%, and many reasons led to performance significantly lower than market expectations (~21.2 billion U.S. dollars).

From the perspective of income growth contribution, aside from theme parks which are relatively stable, cable TV and film and television content income are seriously lagging behind, and the trend of traditional business repair is significantly weakening. Although the growth of streaming media users is impressive, more bundled users and weaker advertising have dragged down overall revenue.

Although Marvel's "Thor 4" box office numbers are good, to ensure more exclusive content on streaming platform Disney+, content licensing to outside companies is decreasing, and offline films will be quickly placed online, resulting in reduced distribution income.

Cable TV was impacted by the high base effect of the NBA Finals in the same period last year. However, cable TV is essentially a sunset industry and there is a trend of migration by streaming media users.

Let's take a closer look at the specific business situation:

1. Streaming Media Business (DTC)

Although it does not contribute much to the company's current revenue and profit, the streaming media business is indeed the main logic supporting the company's growth and providing the main driving force for the market valuing Disney's future.

It achieved revenue of 4.9 billion yuan this quarter, a year-on-year increase of 7.6%. Although the growth in subscription users is impressive, with 12.1 million new Disney+ subscribers, 2 million more than the market expected, overall revenue was significantly lower than expected due to factors such as weaker advertising, user turning to high cost-effectiveness bundling, and exchange rates.

The increase in new Disney+ streaming users this quarter mainly comes from regions other than North America and India. Dolphin Analyst speculates that this might be related to Disney's recent push in Europe and Latin America. As of October, Disney+ has a total of 164 million users and a total of 236 million users across all platforms.

The increase in new Disney+ streaming users this quarter mainly comes from regions other than North America and India. Dolphin Analyst speculates that this might be related to Disney's recent push in Europe and Latin America. As of October, Disney+ has a total of 164 million users and a total of 236 million users across all platforms.

Although ESPN+ had a significant price increase (+43%) in August, its growth this quarter was still good, highlighting the competitiveness of ESPN+ products. In October and December, Hulu and Disney+ also chose to raise prices, and the increase was not small, especially for Disney+. In order to make way for their advertising package, Disney+ increased their price from $7.99 to $10.99, and $7.99 became the price for advertising packages on Disney+.

In terms of price alone, the price for the Disney+ advertising package with weaker show resources is more expensive than Netflix's $6.99, suggesting to pay more attention to the management's disclosure of more details about the advertising package plan in future phone meetings.

Although the ARPU per user price has been weakened by exchange rates and bundled prices, ESPN+‘s price increase has improved month-on-month.

The performance of theme parks this quarter was still relatively steady compared to other businesses, although not up to market expectations. However, unlike in the past, the operating profit margin in the fourth quarter has significantly declined. The company explained this was due to significant pressure brought on by high inflation in commodity procurement costs.

Revenue in this quarter was $7.43 billion, a year-on-year increase of 36%, with park experience revenue at $6.1 billion, a year-on-year growth rate of 46%, which has significantly slowed down. The slowdown in the growth rate for the domestic US market this time is quite evident, except for the effect of Hurricane Ian (decreasing profits by $0.65 billion). Dolphin believes that this may be related to the end of the offline traffic recovery this quarter.

On October 11, the company announced a price increase, hoping to pass on the pressure of inflation to consumers. Although from the current situation, tourist traffic is still high (exceeding the level of the same period in 2019), Dolphin believes that the future growth will need to be driven more by price increases.

However, Dolphin reminds us that after the effect of the "tourism peak season + centenary celebration" in the next quarter, there may be an inflection point in the growth rate and performance of theme parks. As the most significant business in terms of revenue contribution, it will bring short-term performance pressure to the company.

Apart from the price increases, with the gradual lifting of the Asian market's pandemic blockade, future growth can also be expected from the Japan, Shanghai, and Hong Kong Disneyland areas. In a normal year before the outbreak, revenue from international theme parks contributed to nearly a third of total revenue. Therefore, their repairs will also drive overall revenue growth, but due to exchange rate reasons, a discount may still be necessary.

3. Sale of film and television content

The income from content sales is mainly related to the performance of Disney's films in the current season, as well as the distribution and authorization of other television programs and fees for home TV on-demand. In this quarter, Disney released the Marvel blockbuster "Thor: Love and Thunder", which has a global box office revenue of 761 million as of now; in addition, "Hocus Pocus 2" chose to go directly to Disney+, and "Thor: Love and Thunder" also went online on Disney+ in early September after being shown in offline cinemas for more than a month.

Combined with the previous direct streaming of many animated movies and the simultaneous online and offline release of "Black Widow", it is expected that in the future, in order to ensure the growth of Disney+, Disney will guide more offline users to switch to streaming media.

However, this has resulted in a significant short-term sacrifice, with a large portion of the income from content sales being directly lost. Revenue from external licensing of TV series has decreased, and potential box office revenue from movies has also been compressed.

The revenue from film and television content in Q4 was nearly 1.74 billion, a year-on-year decrease of 15%, setting a new low for quarterly revenue in the past three years. But in fact, Disney is still in its own content cycle, with the end-of-year releases of "Black Panther 2", "Avatar 2" and the early release of "Ant-Man 3" being among the famous IPs under the company. As of now, the premiere of "Black Panther 2" and the feedback from the trailer of "Avatar 2" have been good, and the final box office is expected to be impressive, but it is worth noting that they have not been introduced to the mainland China, and have only been released in Hong Kong and Taiwan.

However, the question is whether sacrificing content distribution and cinema revenue in order to continue serving streaming media users indicates an overly optimistic market expectation. After all, streaming media is still in the competitive stage of fighting, and the content of Marvel, Lucas, and Pixar studios is the ace under their umbrella. The launch of Disney+ can ensure that Disney has a strong competitive advantage in the streaming media battlefield, but the sacrificed is the cashable short-term box office revenue.

However, the question is whether sacrificing content distribution and cinema revenue in order to continue serving streaming media users indicates an overly optimistic market expectation. After all, streaming media is still in the competitive stage of fighting, and the content of Marvel, Lucas, and Pixar studios is the ace under their umbrella. The launch of Disney+ can ensure that Disney has a strong competitive advantage in the streaming media battlefield, but the sacrificed is the cashable short-term box office revenue.

Disney+'s significant price increase and launch of advertising packages are all actions that the management hopes to quickly tap into the monetization capabilities of streaming media. Whether it can match the original film and television content revenue in the future is still a question mark. However, it can be seen that it is not easy in the short term, and in terms of profitability, it is afraid that it is not as good as the film and television content sales business which can maintain a 15-20% operating profit margin level under steady-state conditions.

While streaming media in the United States is investing heavily in exclusive content and cutting off mutual authorizations, the long video platform in China has already gone from competition to cooperation, and more and more content is being shared except for a few top works that need to be independently output. This belongs to the collective pursuit of industry efficiency. Under this situation, it can instead force the improvement and optimization of upstream content costs. However, obviously, the American streaming media industry, which has just begun to strike out, is still a long way from such "awareness."

4. Cable networks

Traditional broadcast and television media fell by 5% year-on-year this quarter, mainly due to the high base effect caused by the NBA Finals in the same period last year. However, the weakness of traditional cable television is the general trend, and various streaming media platforms can still expand "peacefully" in the content side under fierce competition, mainly dividing the user time of cable television.

3.

Profit side: All lines are weakening, and structural adjustments will continue.

The profit margin trend that was praised by the market in the previous quarter was fiercely overturned in the fourth quarter. The losses of streaming media have further increased, and traditional businesses seem to have a downward trend in their peak points. In addition to the slowdown in revenue growth and the increasing pressure on the cost of fixed-type expenditures, inflation has also been used by the company to explain the reason for the weakened profitability of theme park revenue. The fourth quarter achieved an operating profit of 1.6 billion, which is the same as last year, significantly weaker than the market's expected 2.05 billion.

Here, Dolphin Analyst suggests that everyone pay attention to the explanation of the management conference call. Dolphin Analyst will release the minutes of the meeting on the Longbridge app or investment research group for the first time. If you are interested, you can add the WeChat account dolphinR123 to access the minutes.

!

!

{kind=link}

However, Dolphin Analyst believes that the higher cost of content investment in businesses outside of theme parks has not resulted in the same increase in revenue, which is the main reason for the overall profit being suppressed. Essentially, this reflects the weakening of the company's profitability due to the rapid premium of the content side in the face of accelerated competition. In conjunction with Netflix's level of operating profit margin, the trend of optimizing three points annually was broken in the second half of last year when competition was highlighted, and it has been declining sequentially quarter by quarter. Even with the currency exchange rate as a factor, it is also in a state of stagnation.

Disney management has stated that it is about to reach the inflection point of streaming media losses. This is basically in line with the expectations of core investment banks, which is that the degree of loss in the fourth quarter is the highest point, followed by gradual improvement, until streaming media achieves profitability in 2024. However, Dolphin Analyst believes that it is difficult to avoid the overall weakening of Disney's profitability due to changes in revenue structure before this.

Dolphin "Disney" Related Articles

Financial Report Season

August 11, 2022 Telephone Conference "Disney: Strong Offline Demand, Lowering Medium- to Long-Term Streaming User Guidance (3Q22 Telephone Conference Minutes)"

August 15, 2022 "Disney: Theme Parks Remain Hot, Streaming Media Is Running for Expansion"

May 12, 2022 Telephone Conference "Disney: Strong Content in Second Half of the Year, Park Prosperity Continues, Lower Content Authorization and Asia Park Closures Are Disadvantages (2Q22 Telephone Conference Minutes)"

May 12, 2022 Financial Report Review "Disney: Accelerated Profit Release from Traditional Business, Striving to Inject Blood into Streaming Media"

February 10, 2022 Telephone Conference "Gradually Entering the Content Cycle, Management Is Confident in Growth Targets (Disney Conference Call Minutes)](https://longbridgeapp.com/topics/1908418)"

February 10, 2022 Financial Report Review "Disney: Streaming Media Growth Returns to Glory, Even More Beautiful Is the Theme Park" On-phone meeting on November 11, 2021: "Impact of the epidemic, Disney's content cycle in the second half of the 2022 fiscal year (minutes)"

Review of financial report on November 11, 2021: "Is Disney's long transformation road even harder with slow streaming growth?"

In-depth analysis: "Disney: The Bubble of streaming burst, returning to the roots of Theme Parks" on June 1, 2022: "Disney: The Bubble of streaming burst, returning to the roots of Theme Parks"

"Disney: The "Fountain of Youth" for Centenarian Princess" on October 10, 2021: "Disney: The "Fountain of Youth" for Centenarian Princess"

"Can Disney's Continuous 'Dream-making' Achieve a Dreamlike Valuation?" on October 15, 2021: "Can Disney's Continuous 'Dream-making' Achieve a Dreamlike Valuation?"

Risk Disclosure and Statement in This Article: Dolphin Research Center Disclaimer and General Disclosures

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.