Trending Creators in 2025

Trending Creators in 2025Lulu Q3 2025 业绩概览与数据整理

Revenue and Profit

Total Revenue: ~$2.6B (YoY +7%)

Diluted EPS: $2.59 (~10% decline YoY)

Regional Performance

Americas Net Revenue: ~2% decline

International Net Revenue: ~33% growth

Same-Store Sales: ~1% global growth (Americas -5%, International +18%)

Gross Margin & Operations

Gross Profit: ~$1.4B (+2%)

Gross Margin: ~55.6% (-290bps)

Operating Income: ~$435.9M (-11%)

Operating Margin: 17.0% (-350bps)

Stores & Inventory

Total Company-Operated Stores: ~796

Inventory: $2.0B (~11% YoY growth)

Cash & Equivalents: ~$1.0B

Shareholder Returns

Share Repurchase: Board approved increase to ~$1.6B authorization (including new $1.0B)

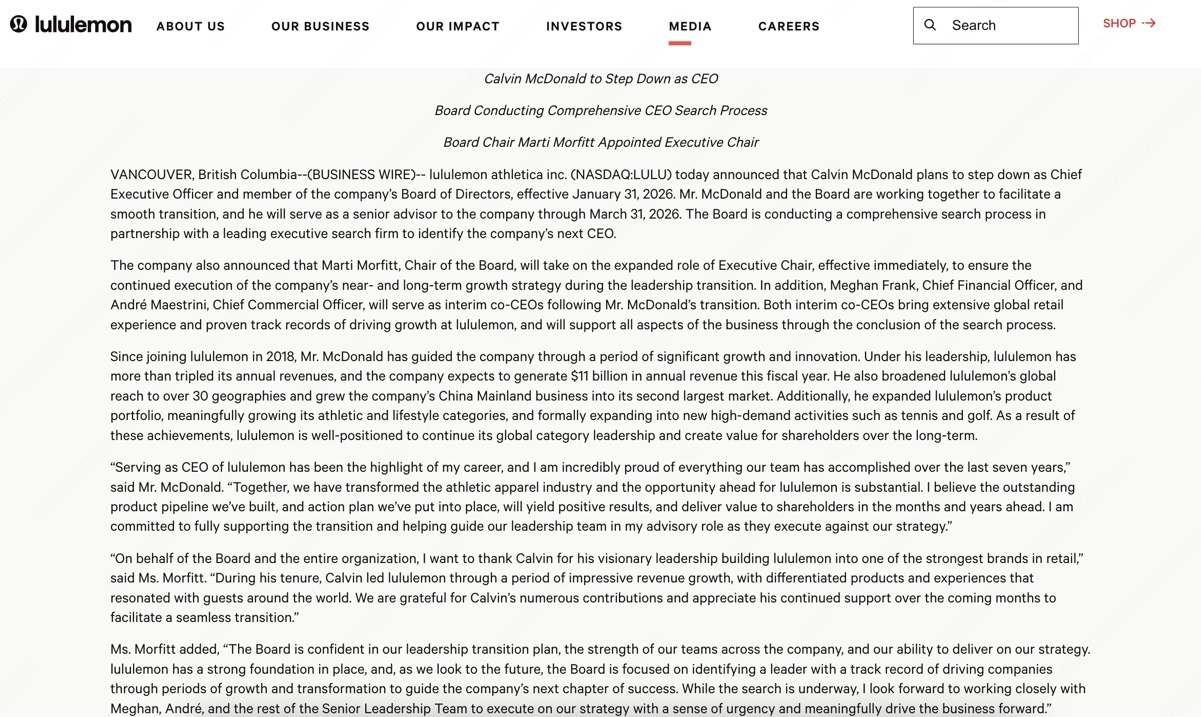

Notes: International growth remains strong, aligning with prior "international expansion as the long-term narrative" expectations; Negative sentiment pre-earnings set up the revenue/EPS beat; McDonald's departure was somewhat unexpected - need to monitor succession plan. Ongoing concerns remain margin compression and inventory growth.

$Lululemon(LULU.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.