AI Internet: 2026 ByteDance vs. BABA vs. Tencent — Three-Way Showdown

$Alibaba(BABA.US) $ByteDance(BYTED.NA) $TENCENT(00700.HK) $Baidu(BIDU.US)

In prior discussions on the AI value chain, Dolphin Research focused on North America and unpacked the tangled profit tug-of-war across upstream players. Those dynamics remain the baseline for understanding incentives across the stack.

China’s consumer AI only truly broke out last year. With a consumer market geared toward pragmatism, and after DeepSeek cracked the compute-cost logjam, local players converged on an application-first path to compete, making cost-effectiveness a hard constraint.

Compared with North America’s heavy spending, China’s tech majors stayed more disciplined on upfront capex. At the same time, their focus on end-user rollout led them to push both mature and still-experimental AI products to mass audiences, accelerating user penetration materially within a year.

From an application lens, this note reviews where AI adoption stands after the past year and how China’s Big Tech are positioned. This piece covers industry shifts and competition; company deep-dives will follow.

I. Consumer Internet in the AI era: bytes step aside, tokens are the future

Before the China AI showdown, note the quiet reset of production factors in the AI age. This reset is reshaping who pays and how value accrues.

Pre‑AI, consumers accessed search, short video, shopping and more via apps or the web essentially for free, aside from their own data plan or broadband. On the supply side, developers provisioned four commodity-like inputs at scale: compute (CPU), storage, network bandwidth, and power.

In the AI internet, what looks like ‘human-like’ reasoning layered on search and content forces a wholesale rebuild of that base. For developers, all four inputs are being retooled.

Compute: GPUs surged to dominance, with leaders leveraging technical moats to harvest outsized margins. Storage: larger models, longer context windows, and fast multi‑modal growth drive capacity and performance needs.

Network: upgrades concentrate in DC networking gear and materials. Power: AI data centers are voracious energy consumers.

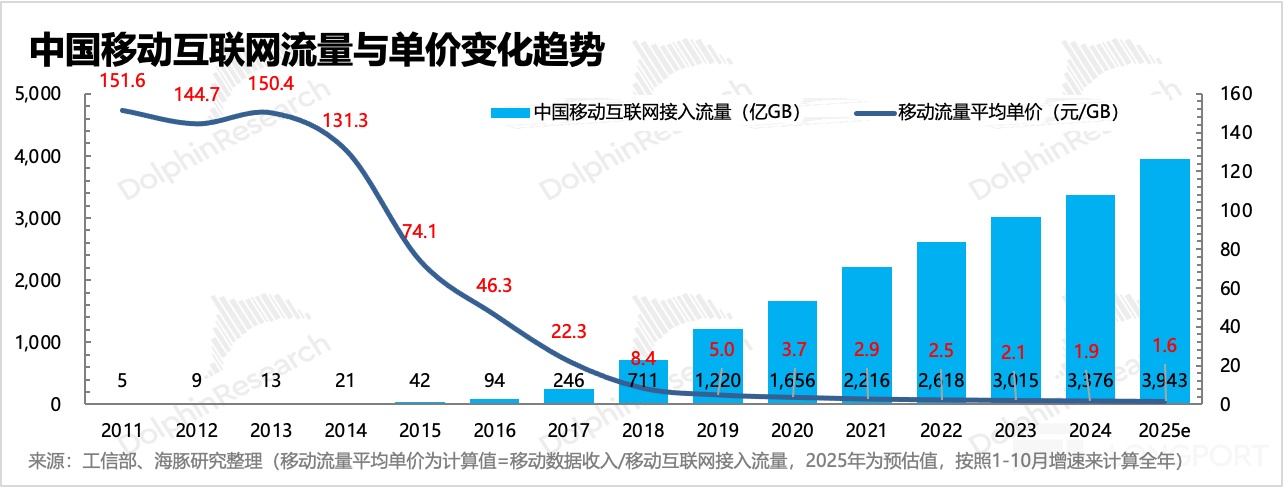

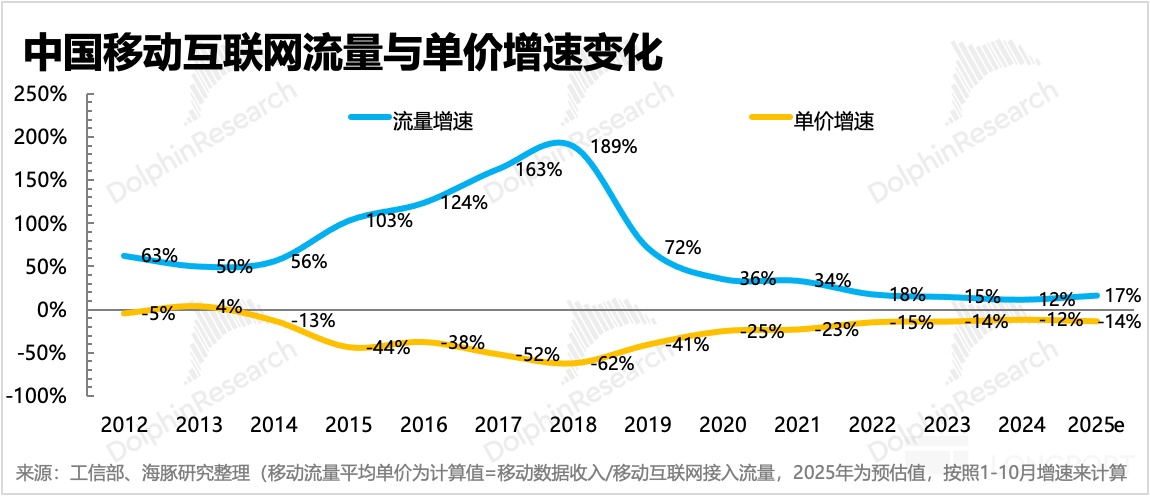

This shift collides with consumers’ deeply ingrained ‘free’ mindset. Historically, you paid for connectivity measured in bytes; in the AI era, a parallel token‑meter may emerge for inference, from device ‘AI chat’ subscriptions to ChatGPT plans that are, in essence, token bundles.

Meanwhile in mobile internet, data plans—cellular and broadband—fell to rock‑bottom pricing in China amid aggressive Gov. push for faster, cheaper access. That anchored expectations around near-zero marginal cost for usage.

Before DeepSeek, China’s models lacked sufficient autonomy and the supply chain faced chip constraints. Asking users to pay tokens for a still‑immature ‘AI assistant’—when basic search was free—meant trial without conversion, as seen in early paid attempts like BIDU’s Wenxin Yiyan.

That’s why, even as ChatGPT soared in the West, China lacked a mass‑market AI chat app with comparable global scale. The production‑factor reset was simply too expensive, leaving app developers to shoulder costs even with strong paid uptake overseas, forcing usage caps to curb runaway inference bills.

Service providers had to optimize architectures, scale revenue, and seek cheaper compute—bypassing margin‑taking CSP middlemen where possible—to narrow the cost‑revenue gap and chip away at the GPU premium. (For value chain profit splits, cf. ‘AI 泡沫原罪:英伟达是 AI 戒不掉的毒丸?’)

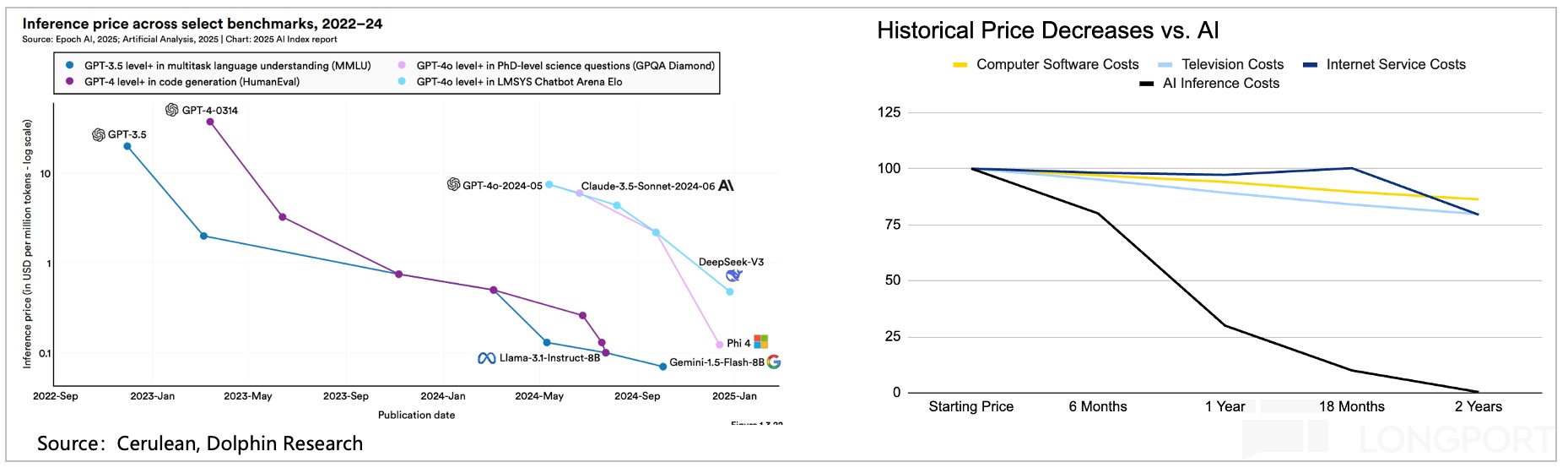

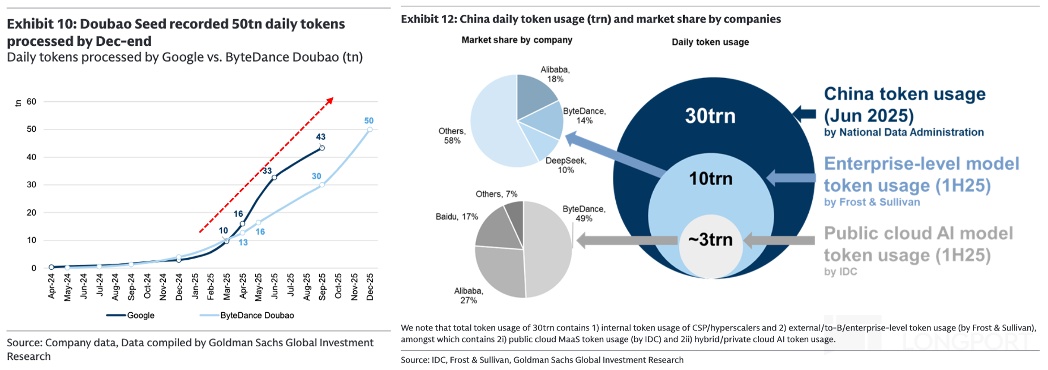

As of late 2025, token consumption is still exploding and total inference opex remains high. Yet unit inference costs have dropped 90%+ over two years on GPU iteration and more diverse accelerator supply.

II. Mobile internet x AI: the speed gap between China and the U.S.

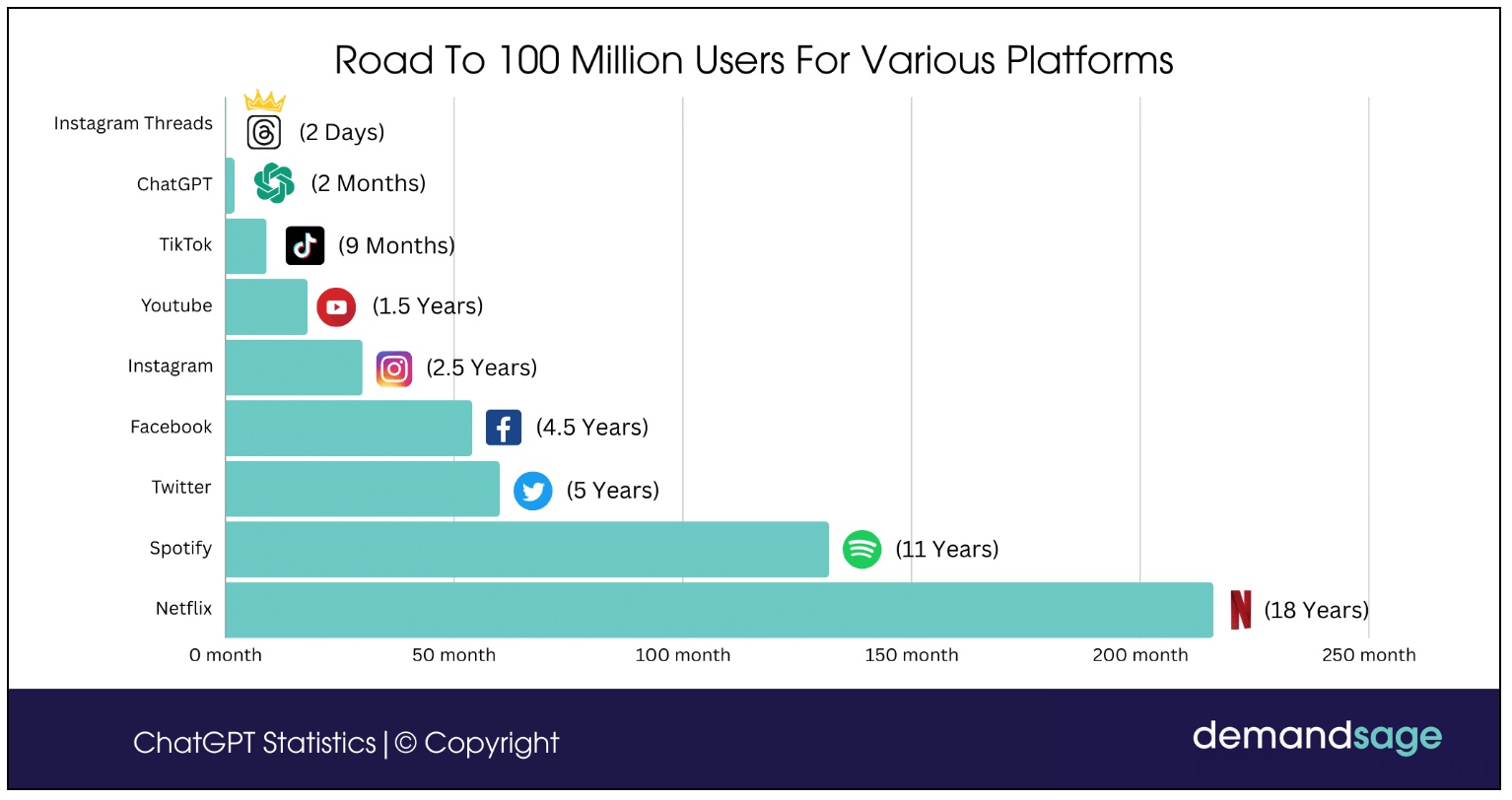

With AI infra in place, GenAI user education has been far faster than in prior PC, mobile or video cycles. ChatGPT hit 100mn users in two months—about six months faster than TikTok—amid a global sprint among frontier models, with China’s model builders staying competitive.

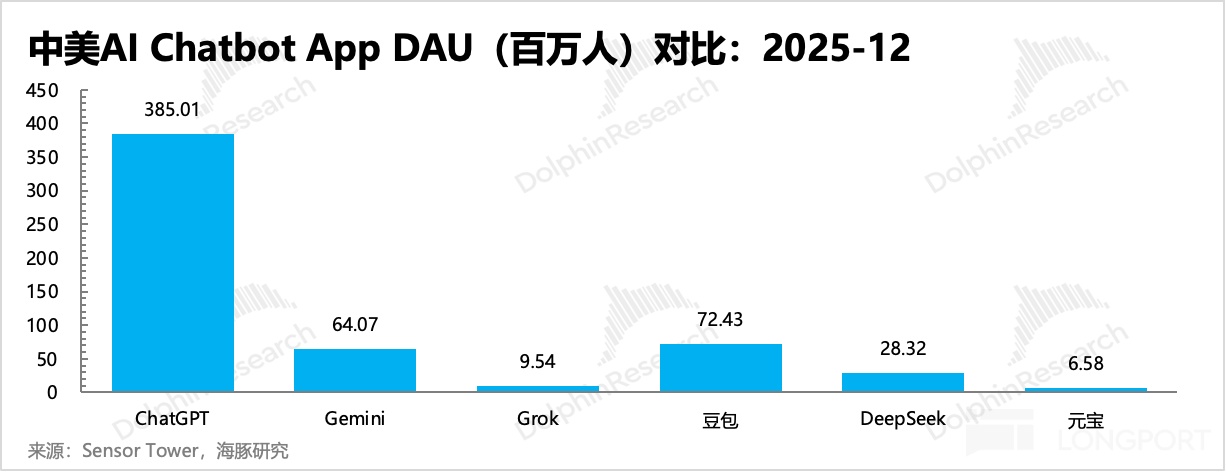

But on AI‑to‑C, China lags visibly. ChatGPT’s MAU has reached ~800–900mn since GPT‑3’s release in 2022, while China’s leading general AI app Doubao is a bit above 200mn, a multi‑fold gap.

One could argue market by market the gap narrows: ChatGPT’s ~70–80mn U.S. users imply ~25% penetration of ~300mn mobile internet users, while Doubao’s ~220mn implies ~20% of China’s ~1.15bn users. Penetration in each home market looks comparable.

In reality, China is still behind in AI‑to‑C adoption. International expansion has been slow, and domestic penetration relies heavily on free access for products that are paid elsewhere.

By early 2026, three forces set the stage for a China AI consumer app battle. Models are now smart enough, with Qwen, DeepSeek, Kimi and Doubao highly ranked globally; and at the inference phase, chip bottlenecks have eased with usable domestic accelerators and importable H200s, reducing scarcity pressure.

With both gaps narrowing—and ChatGPT as a proven general AI‑to‑C template—China’s internet majors, slow out of the gate, are now poised for an all‑out AI app melee in 2026. Expect rapid escalation.

III. The war hasn’t started, but firepower is maxed

On competition, China Big Tech spent a year in low‑gear, then surged after DeepSeek’s ‘compute equality’ moment, reminiscent of 2015 when policy‑driven traffic cost cuts catalyzed mobile internet’s boom. AI evolves faster than classic internet, making competition harsher; even typically reserved Tencent unleashed aggressive marketing in Q2, and the landscape has already shifted in under two years.

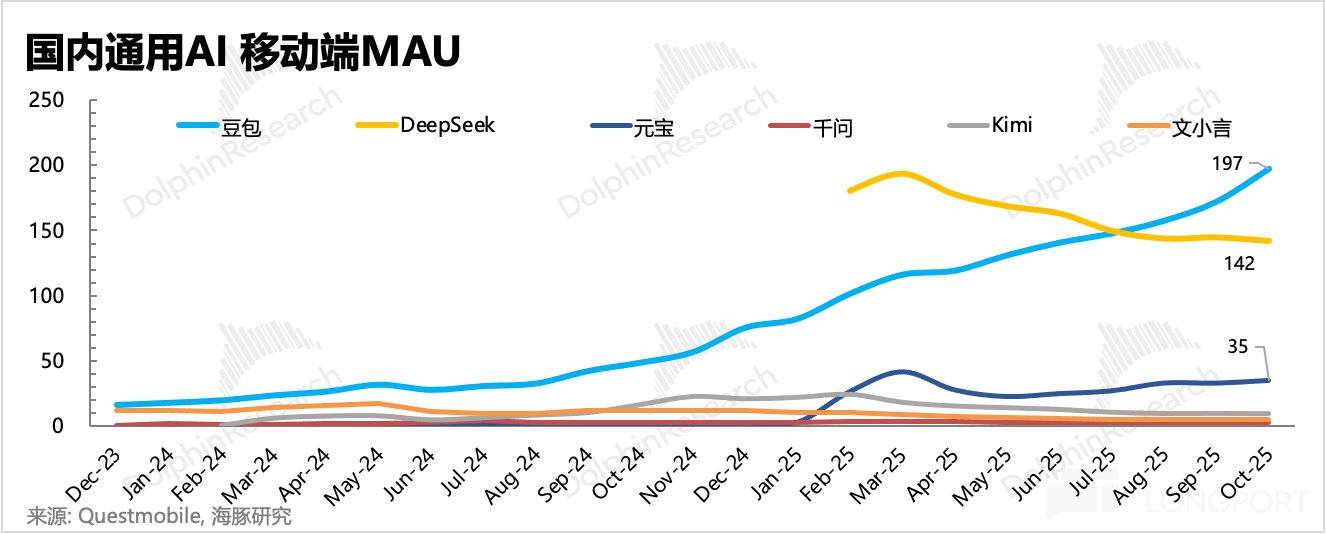

In general AI apps, Doubao has overtaken early mover Wenxiaoyan and widened its lead, yielding a classic 6:3:1 structure. By MAU, Doubao holds ~60%, DeepSeek ~30%, and the remaining ~10% is led by Yuanbao at roughly one‑sixth of Doubao’s scale; Qwen ramped only from Nov, but per official data hit 30mn MAU in 23 days, up nearly 10x in just over a month.

It’s far from over. Both challengers’ urgency and leaders’ refusal to ease off suggest 2026 will remain a slugfest.

Doubao, despite its lead, is still pressing—securing the Spring Festival Gala sponsorship to widen the gap. Qwen is in full‑throttle promotion and won’t concede; Yuanbao’s surface calm masks steady iteration, and a year‑end hiring spree signals Tencent’s 2026 won’t be quiet.

China AI is still nascent, making end‑state structures hard to call. Two questions may frame the thinking.

1) Why do internet majors insist on building a standalone, general AI entry rather than embedding AI solely within existing gateways? 2) What do their ecosystem shapes imply about strategy?

1. Big Tech AI rollouts: head‑to‑head

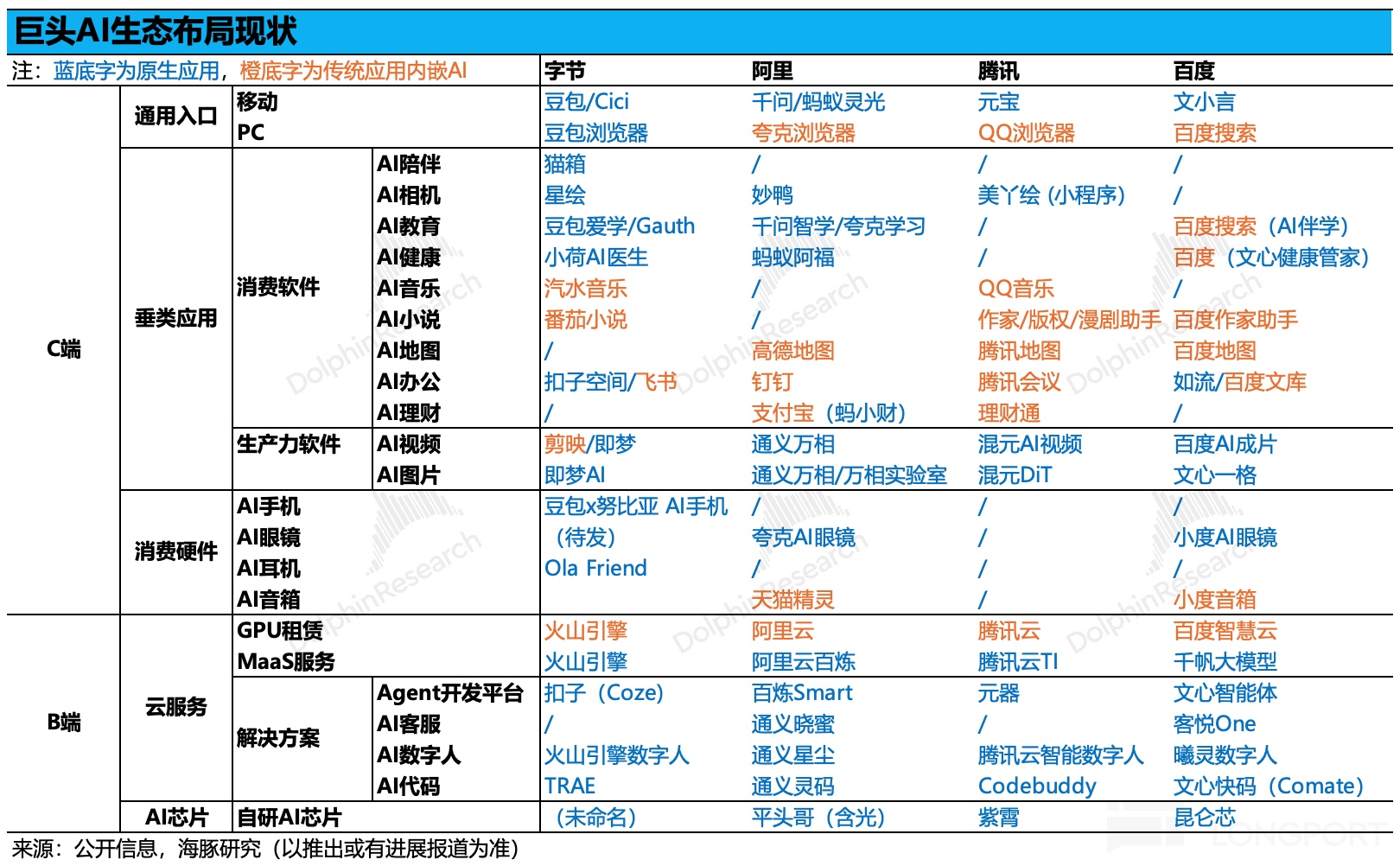

Across the four giants’ AI ecosystems, progress varies. A few patterns stand out.

(1) ByteDance is the fastest on To‑C, leveraging Douyin’s massive exposure and pushing both software and hardware. On To‑B, it is catching up; while its model benchmarks are unexceptional, Volcengine’s MaaS influence keeps rising on vertical focus and value.

(2) Alibaba is broader on To‑B, underpinned by strong model capabilities. It has also stepped up To‑C in 2H, relaunching general AI such as Qwen and Lingguang, but without a Douyin‑scale in‑house channel, it leans on external buying and model reputation.

(3) Tencent appears more restrained on native AI. Its model is middling, To‑B has few standouts, and To‑C centers on Yuanbao; the market pins hopes on a ‘training’ WeChat Agent, keeping 2025 messaging low‑key. Despite heavy early‑year buying for Yuanbao, most spend stayed within ‘Goose‑verse’ channels, with limited external traffic buys.

2. Strategic logic behind the plays

AI ecosystems mirror the internet’s ‘1+N’ structure, but routes to market differ. Execution reflects each firm’s asset base.

2.1 General use cases: the inevitability of a new entry point

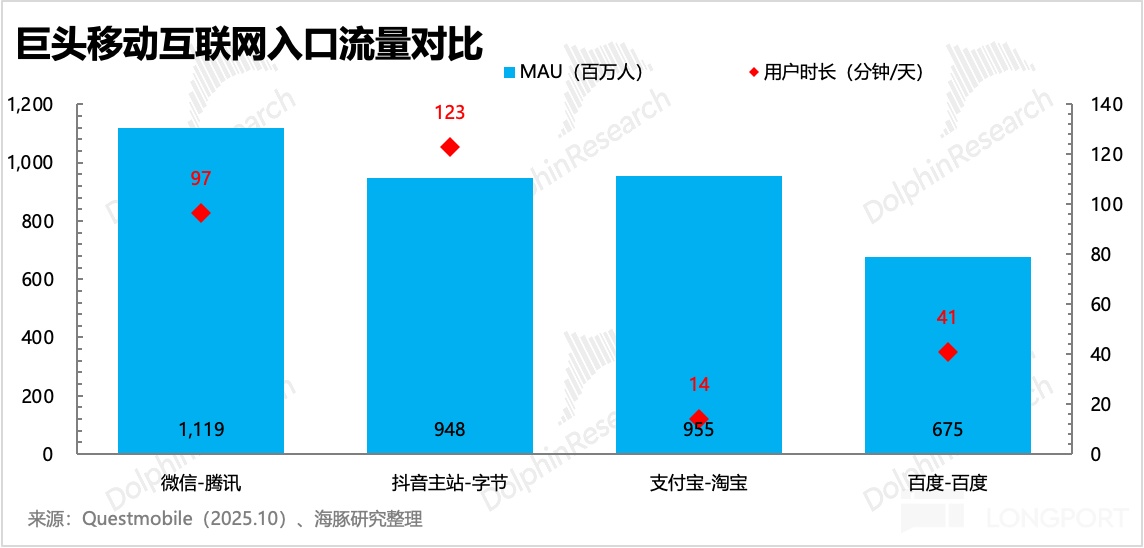

All four launched new, native general AI gateways. Define a ‘super entry’ in mobile internet as high traffic plus long duration—say, 600mn MAU and 30+ mins daily time—then assess today’s candidates against that bar.

Alibaba’s push for a new gateway is straightforward. Its largest apps, Taobao and Alipay, aren’t high‑duration, and each faces a heavyweight rival in core use cases (PDD and WeChat Pay), making Qwen’s early traction a morale boost driven by both traffic tactics and truly ‘usable’ model quality.

BIDU likewise seeks an AI reset. Mobile Baidu technically qualifies as a super entry at ~700mn MAU and ~40 minutes a day, but its influence has visibly eroded, creating urgency for a successor.

Why would ByteDance and WeChat—near‑universal coverage with 100–120 minutes daily time—still build a brand‑new gateway? Two reasons stand out.

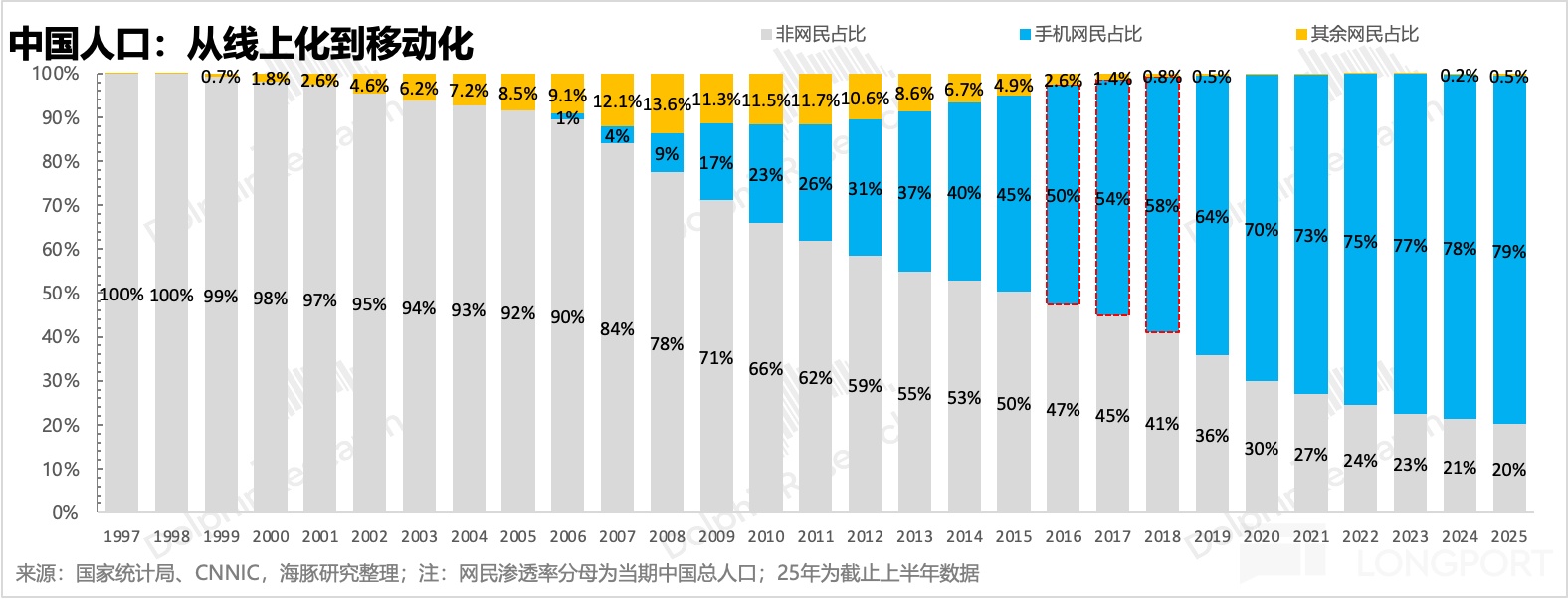

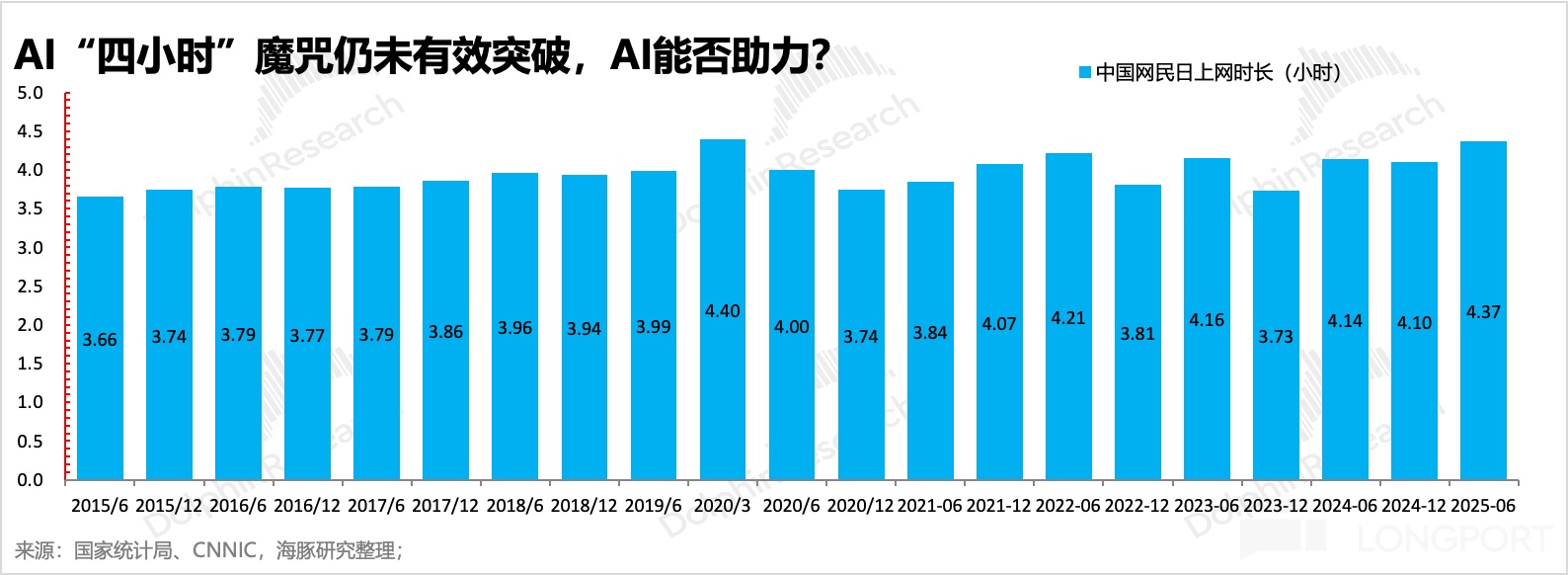

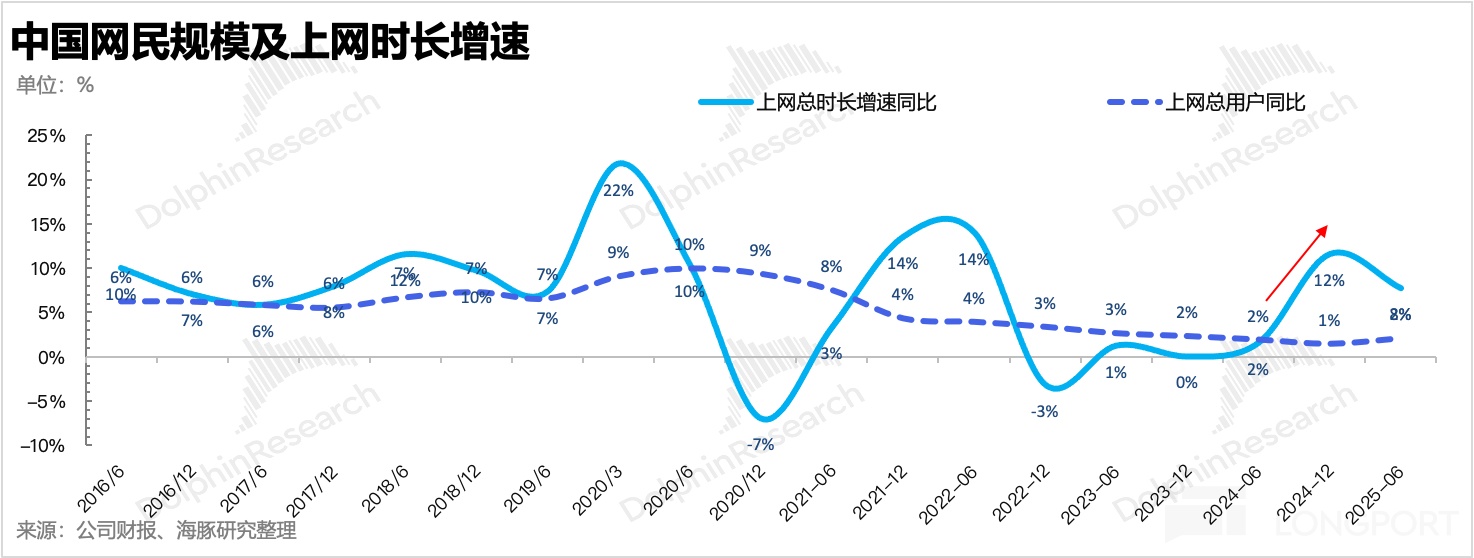

(1) The old interaction paradigm is showing its age. After 20 years, mobile internet has near‑saturation at ~80% of the population and ~4 hours daily time stuck for three years; short video gained share but is now embedded across apps, pushing ecosystems toward a new steady state.

AI brings a step‑change in HCI and a perceived upgrade, pulling some post‑COVID offline time back online. In H2‑2024 to H1‑2025, both user count and time per user ticked up.

Yet stability remains an issue, and it’s unclear if AI fits most users and scenarios today. Giants fear both erosion from new AI gateways and breakage if they over‑modify incumbents too soon; a standalone app as a ‘test field’ is the prudent path.

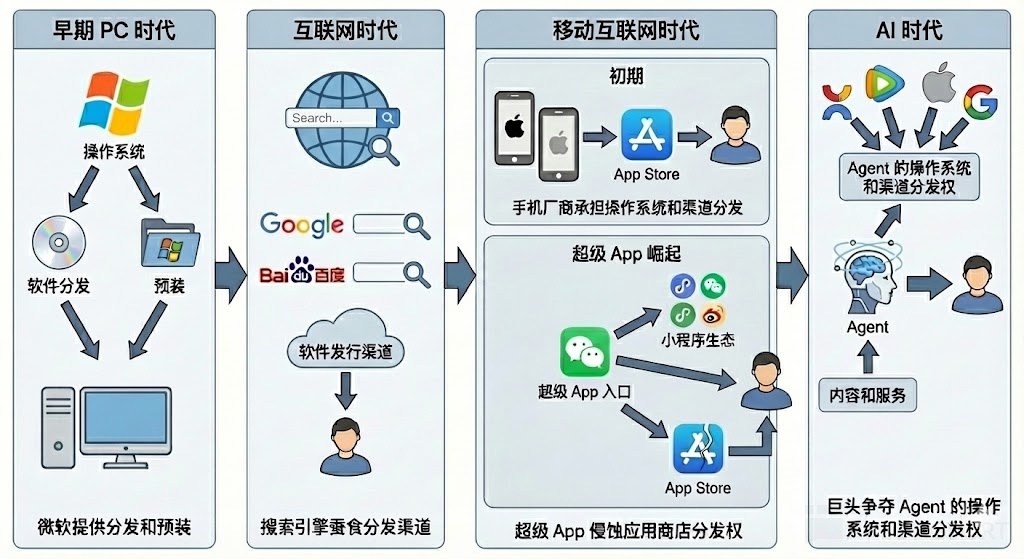

(2) The prize is the next OS‑level gateway. PC era OS distribution sat with Microsoft; search engines like Google and BIDU diverted software distribution in the web era; mobile OS and app stores shifted power to handset OEMs, until super apps like WeChat—with mini‑program ecosystems—started to erode OEM distribution, acting OS‑like in practice, as did Douyin and Alipay in their domains.

Each OS shift rode an HCI change—hardware or the software shell that directly touches users. If AI content and services are delivered via Agents, the new ‘OS’ is the Agent runtime and its distribution rails; that’s what the giants must seize with full commitment.

Source: Dolphin Research

2.2 Verticals: app factory vs. classic enablement

For verticals, strategies diverge. A firm can launch standalone AI apps or embed AI into existing apps; ByteDance favors the former with its ‘app factory’ playbook, Alibaba leans that way too, while BIDU and WeChat prefer AI plug‑ins for legacy apps.

These choices are rooted in core strengths. Tencent, Alibaba, and BIDU all hold vertical footholds from PC‑internet days—Tencent via build + invest and WeChat mini‑programs, Alibaba via investments extending beyond commerce, and BIDU across search, news, cloud drive and finance.

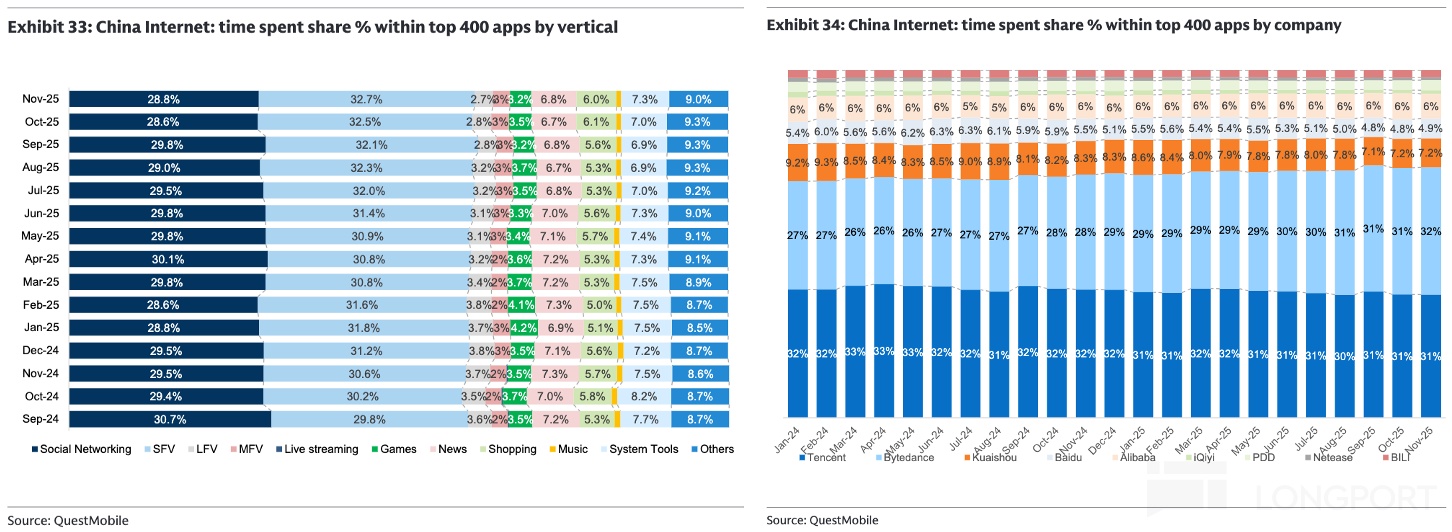

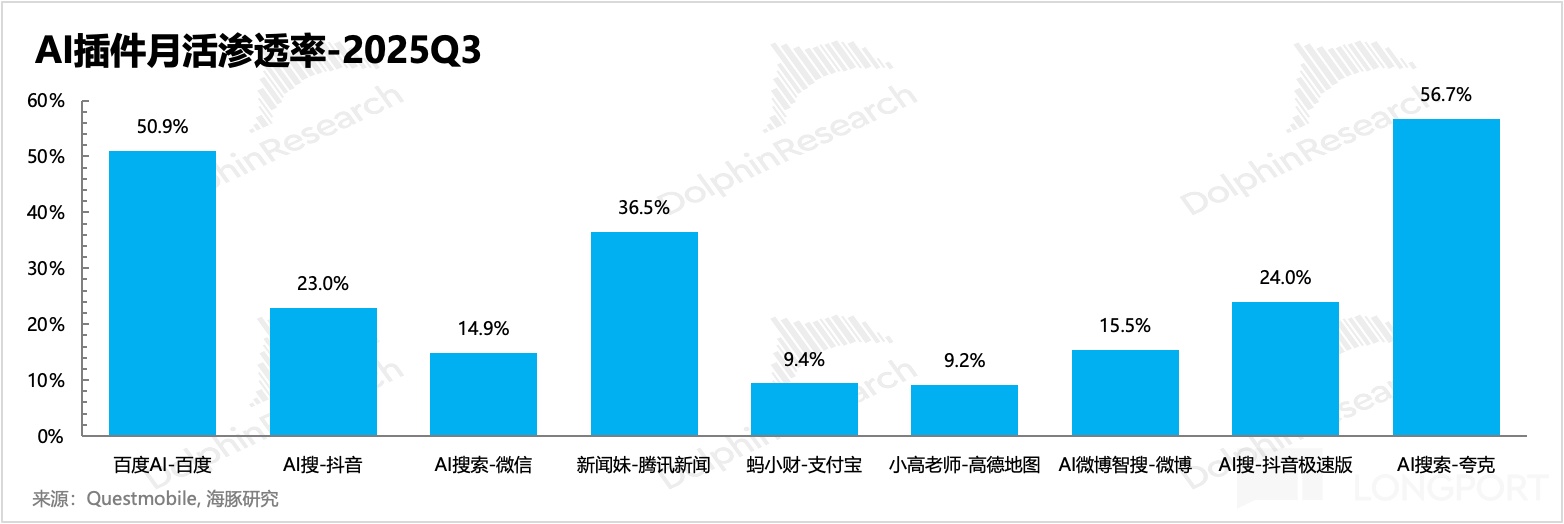

From their vantage point, AI is a logical way to harden and reactivate incumbents. QM data show AI plug‑in penetration inside apps at ~20–30% by end‑Q3‑2025, with chatbot‑style AI search leading.

If everyone enables AI in place, competition resets to status quo, but all vertical gateways inherit higher opex. That is, short‑term ROI looks mismatched, but the spend may be necessary to defend long‑term competitiveness at lower monetization efficiency.

Could AI reshuffle the vertical deck instead? Alibaba seems to pursue a dual path—AI plug‑ins plus new standalone apps. ByteDance, with fewer entrenched verticals, has stronger incentive to disrupt; the Doubao AI phone makes that bet explicit by changing HCI to siphon traffic from incumbents.

The idea isn’t to do every vertical itself, e.g., food delivery. It is to reduce today’s vertical leaders to ‘service providers’ without private traffic, letting Doubao swap in new providers for low‑moat categories while even high offline‑moat verticals lose distribution power and margin.

Near term, verticals can resist by withholding user data via privacy authorization to blunt Agent execution. Ultimately, the outcome depends on who commands user attention; if Doubao ever replaces WeChat as the dominant AI‑era gateway, verticals’ resistance will matter far less.

3. Can Doubao celebrate at halftime?

Post Spring Festival Gala, Doubao—and ByteDance’s broader AI push—will likely cement advantages. But with 2026 set for heavier spend and resources from all sides, there is no final winner yet.

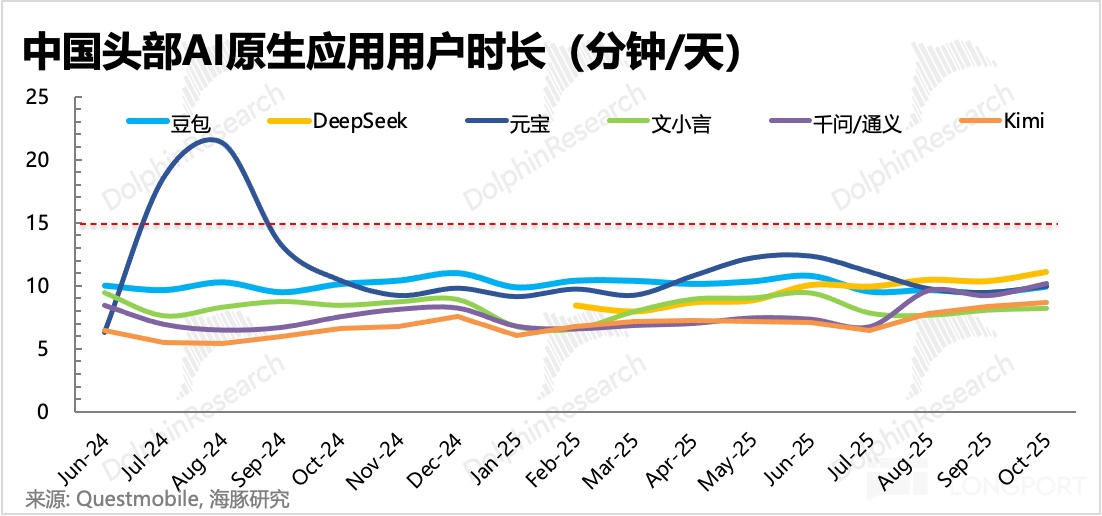

The tell is time spent: even the most penetrated general AI gateways see sub‑15‑minute daily time with no clear uptrend. Doubao, the most frequently used, is around 10 minutes per user per day, signaling ‘tool‑like’ usage for most users; UI and front‑end features remain highly similar across Doubao, Yuanbao, Qwen, and Wenxiaoyan.

Super gateways that won before did so by ‘leveling up’ through content, services, and social graph. WeChat—fundamentally a tool—drove time via content (Official Accounts, Channels), services (mini‑programs, Pay), and social (groups, Moments).

Douyin’s long time comes from precision content feeds, with services (e‑commerce, local) and social still forming. While passive content differs from users actively seeking services via AI, Agents can borrow this playbook to deepen stickiness.

Whoever secures user mindshare first—by wiring rich back‑end ecosystems (content + services) and adding social gravity—will lead. The rapid AI cycle also pushes China’s giants toward a ‘better to over‑invest than miss’ stance.

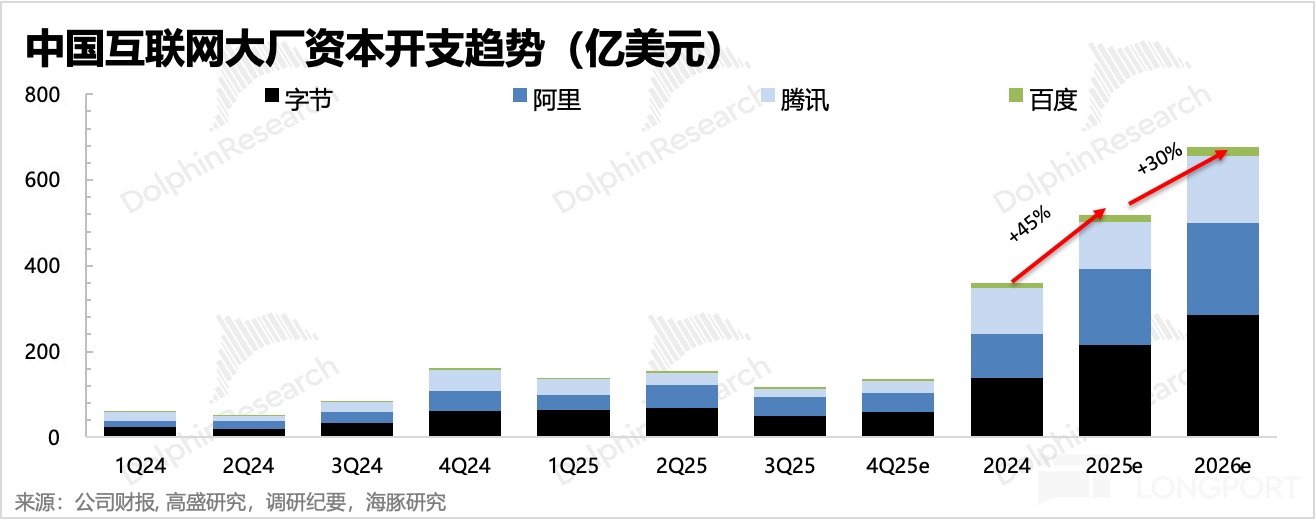

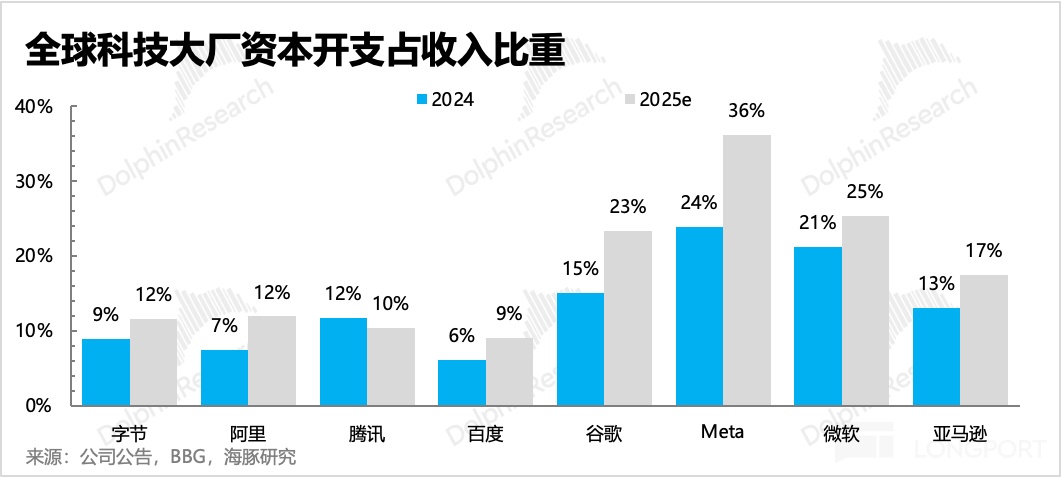

Across ByteDance, Tencent, Alibaba, and BIDU, capex rose ~45% in 2025, with 2026 expected to climb another ~30% per checks and market estimates. Given China’s focus on application rollout vs. U.S. focus on frontier models, and lower running costs (power, DC depreciation), capex as % of revenue is mostly ~10% in China vs. 20%+ at U.S. peers.

On similar 4–5 year depreciation, even with softer end‑demand, China majors’ AI ROI may hold up, giving them more runway to push applications. That could be a structural edge.

Bottom line, 2026 will be highly eventful, with marquee battles among the giants. Key takeaways:

1) With most production‑factor constraints eased in 2025, AI adoption accelerated; China compressed a decade of mobile‑internet user penetration into three years, implying competition will run several times faster than before.

2) ByteDance holds a clear lead today, but 2026 brings the real fights. Current AI gateways still lack complete ecosystems and social graphs, so no one owns the AI‑era ‘super entry’ yet; whoever best stitches content + services and builds social gravity will gain decisive advantage.

3) Versus U.S. peers, China’s giants are investing less aggressively, with more manageable ROI pressure—not yet at risk of cash‑flow or profit collapse.

4) In verticals, giants’ ecosystem edge is large, but their focus on base‑layer entry battles will be all‑consuming. This leaves room for SMEs in narrower, less‑contested niches.

Dolphin Research will next dive into each giant’s AI strategy (Tencent, ByteDance, Alibaba, BIDU) and smaller players’ progress, estimating earnings unlock and incremental value. The next piece starts with Tencent, whose AI strategy has drawn much debate.

Risk Disclosure and Disclaimer (Chinese only):海豚研究免责声明及一般披露

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.