TSM: The Real Boss of AI—Who Would Say No?

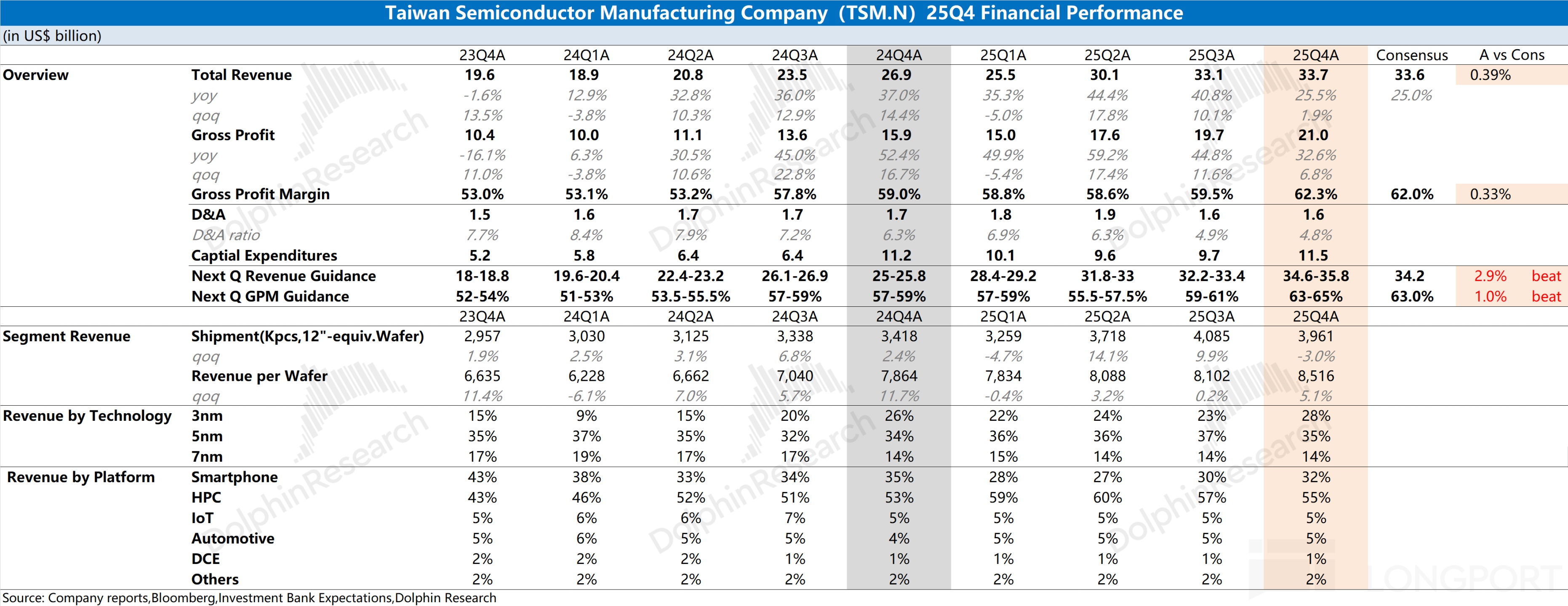

TSMC released its Q4 2025 results (quarter ended Dec 2025) on Jan 15, 2026 Beijing time, ahead of U.S. mkt open on Longbridge. Key takeaways:

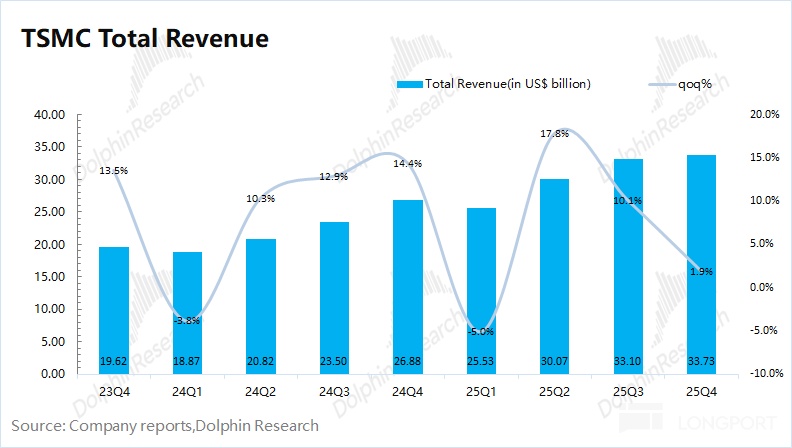

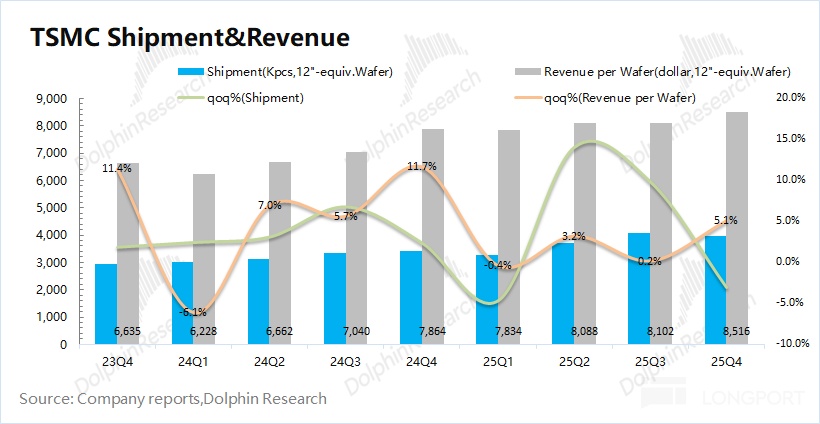

1) Revenue: Q4 revenue was $33.7bn, up 1.9% QoQ, driven by new iPhone shipments and stronger AI chip demand.Despite a stronger USD, revenue topped the high end of guidance ($32.2–33.4bn). In TWD terms, revenue rose 5.7% QoQ, well above the high end of guidance (+1% QoQ).

Volume/price (12-inch eq.) highlights: (i) Wafer shipments were 3,961k, down 3% QoQ; (ii) ASP per eq. 12-inch wafer was $8,516, up 5.1% QoQ.

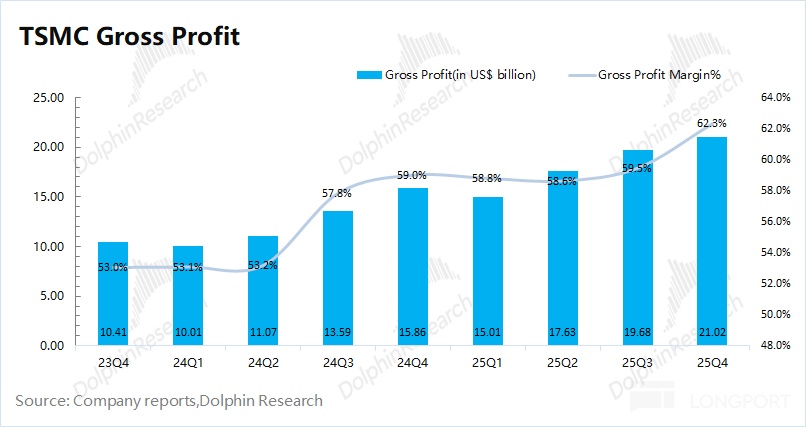

2) GPM: $Taiwan Semiconductor(TSM.US) Q4 GPM was 62.3%, above guidance (59–61%). The margin beat was primarily price-mix led, with a structurally higher 3nm mix lifting ASPs.With AI demand underpinning mix, GPM is now firmly above 60%, and the long-term GPM target was raised from 53% to 56%.

3) Biz. updates: nodes, end-markets, and regions

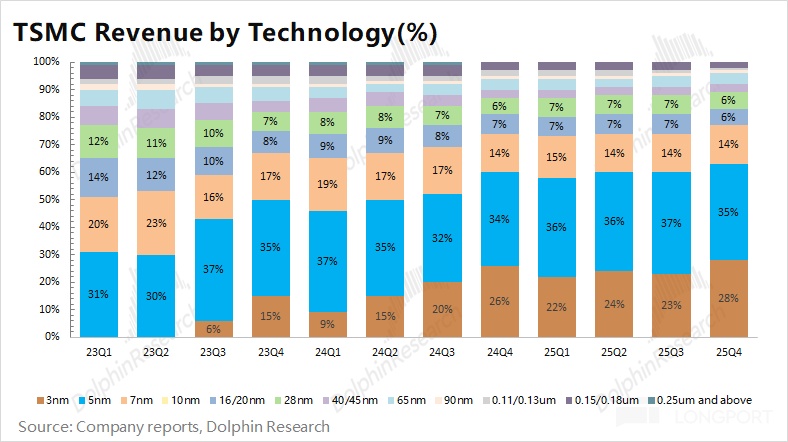

a) By node: Advanced nodes (<7nm) rose to 77% of revenue, a new high. 3nm and 5nm are both fully loaded, contributing 28% and 35%, respectively.As 2nm ramps, AI chips will migrate from 5nm to 3nm, further skewing mix to advanced nodes.

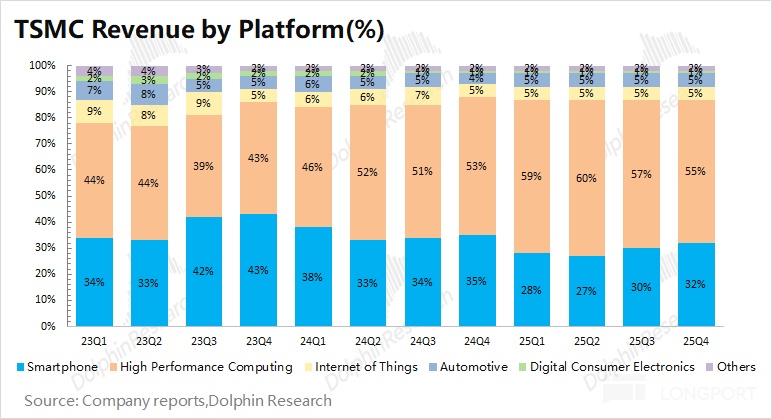

b) End-markets: QoQ growth was led by smartphones on new iPhone shipments. HPC remained the largest revenue driver at $18.55bn (55% mix), supported by demand from Nvidia, Broadcom and other AI chips.

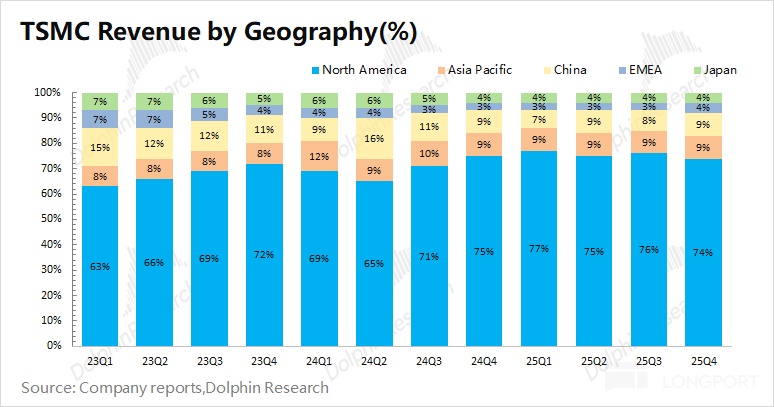

c) By region: North America remained the largest market at 74%, covering key customers such as Nvidia, Apple and AMD.China revenue was Approx. $3.0bn (9% mix), still the No. 3 region.

4) Capex: Q4 capex was $11.5bn, broadly in line. FY2025 capex is $40.9bn, up $11.0bn YoY, within the raised guidance range ($40–42bn).

5) Outlook: Q1 2026 revenue guidance is $34.6–35.8bn (vs. buyside $34.2bn) with GPM at 63–65% (vs. buyside 63%), still driven by AI chip shipment growth.

Dolphin Research view: Guidance shines; TSMC remains dominant

This was a solid print, with revenue trends already visible in monthly disclosures. Reported QoQ growth of 1.9% was dampened by USD strength.In TWD, revenue rose 5.7% QoQ. More importantly, guidance for GPM, capex, and operating outlook stood out.

i) GPM: Q4 GPM of 62.3% beat the raised buyside bar (~62%), mainly on higher 3nm mix lifting ASPs.Next-quarter GPM guidance was raised to 63–65%, ahead of buyside (~63%). As mix tilts further to advanced nodes, rising ASPs should continue to support margin expansion.

ii) Capex: Q4 capex was $11.5bn, taking FY2025 to $40.9bn, up $11.0bn YoY and within the raised $40–42bn guide.More importantly, FY2026 capex is guided up sharply to $52–56bn, above mkt ($48–50bn). This implies an incremental $11–15bn in 2026 and signals confidence in downstream demand and the 2nm ramp.

iii) Operating outlook: TSMC expects ~30% revenue growth in 2026, in line with raised mkt expectations (buyside lifted from 25% to 30%).This would mark a third consecutive year of 30%+ growth in 2024–2026, supporting a larger capex plan.

Beyond the core print, investors are focused on:

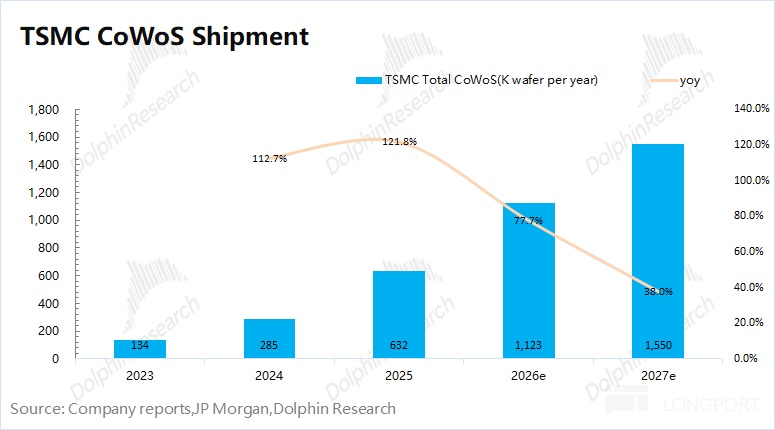

a) CoWoS capacity: Mainstream AI accelerators (Nvidia, AMD, TPU) rely on CoWoS, and TSMC supplies the vast majority of global CoWoS capacity (>90%). Even if chip designers want to raise output, CoWoS allocation will directly constrain AI chip shipments, making TSMC a key chokepoint in the AI chain.

Industry data and mkt expectations suggest current CoWoS monthly capacity is ~70k wafers, potentially rising to ~120k by end-2026.Dolphin Research estimates CoWoS shipments may exceed 1.1mn wafers in 2026 (+77% YoY), with Nvidia, AMD and Broadcom the largest customers.

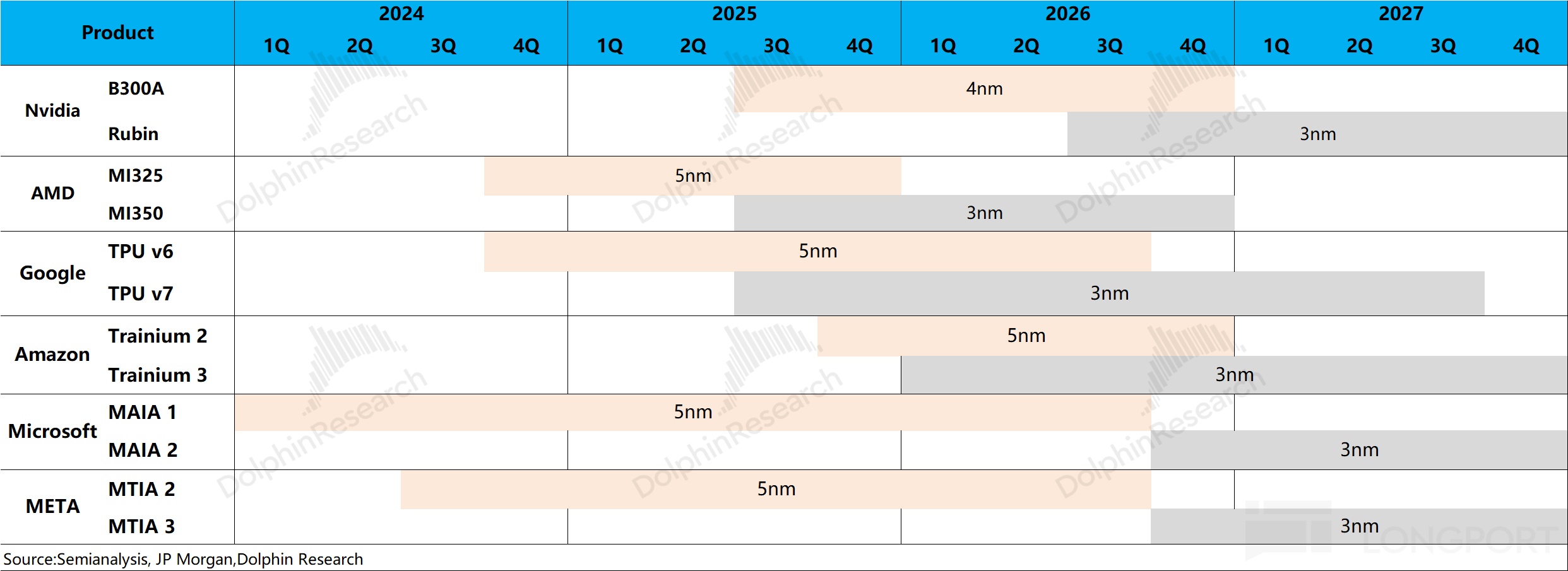

b) 2nm progress and node migration: 2nm will ramp to volume in 2026, with parts of Apple and Qualcomm smartphone demand migrating to 2nm. In parallel, AI chips will broadly upgrade to 3nm, where Rubin, MI350 and Google TPUv7 are set to use TSMC's 3nm.

As the node mix migrates forward, capex will keep rising.This is a direct function of the move to more advanced structures and capacity adds.

c) Foundry competition: As TSMC starts 2nm volume, Samsung and Intel are following with SF2 (2nm) and 18A (1.8nm).

However, both still lag TSMC meaningfully: (i) their latest-node transistor densities are below 250 MTr/mm², even under TSMC's prior-gen N3P (294 MTr/mm²). (ii) Yield rates are relatively low and current volume is focused on internal chips, while TSMC serves a broad set of external anchor customers.

Performance in models like Google Gemini vs. GPT shows compute is only one piece of capability. With AI chips supply-constrained, if Intel and Samsung lift yields, they could still capture some overflow orders.This is an area to watch.

Across a+b+c, TSMC leads peers in technology depth and customer breadth, remaining the most critical link in AI chips.It is best positioned structurally.

At a current mkt cap of $1.7tn, the stock implies roughly ~22x 2026E P/E (assumes revenue +33% YoY, GPM 62.6%, tax rate 16.3%).Versus its historical range (20x–30x), it sits around the lower-mid band.

All in, this was a solid quarter.For 2026, mgmt reiterated a 30% revenue growth target. With CoWoS capacity and process leadership, TSMC remains the single most important foundry in the AI chain. High growth and 60%+ GPM underpin higher capex and bolster confidence in AI and semis.

Because all major AI chip vendors rely on TSMC's CoWoS allocation, downstream players have incentives to pursue backups. Progress in CoWoP and yield trajectories at Intel/Samsung also warrant close watch.

Absent breakthroughs on those fronts, TSMC's CoWoS remains the best option, and TSMC retains outsized pricing and allocation power in AI.

Below is Dolphin Research's detailed read of TSMC's results:

I. Revenue: ASPs kept rising

Q4 2025 revenue was $33.7bn, above prior guidance ($32.2–33.4bn). QoQ growth of 1.9% was led by new iPhone shipments.USD appreciation weighed on reported growth; in TWD, revenue rose 5.7% QoQ, clearly above guidance.

Given monthly disclosures, quarterly revenue is typically well anticipated by the mkt. The key question is the split between price and volume this quarter.How did each contribute?

Dolphin Research assesses revenue drivers through volume and price lenses:

1) Volume: Q4 2025 wafer shipments were 3,961k, down 3% QoQ, reflecting early-stage 2nm ramp adjustments.TSMC lifted its 2026 capex target to $52–56bn, an incremental $11–15bn, a clear signal of sustained capacity expansion.

2) Price: Q4 2025 ASP per eq. 12-inch wafer was $8,516, up 5% QoQ. With 2nm entering production and AI shifting from 5nm to 3nm, product mix will skew further to advanced nodes and support higher ASPs.This should sustain price tailwinds.

II. GP and GPM: firmly 60%+

Q4 2025 GP was $21.0bn, up 6.8% QoQ. GPM reached 62.3%, up 2.8ppt QoQ.Rising ASPs were the primary driver of margin expansion.

Revenue and GPM are the two most watched metrics. With monthly prints, revenue tends to be well priced in.GPM is therefore a focal point this quarter, and Dolphin Research breaks down the key drivers:

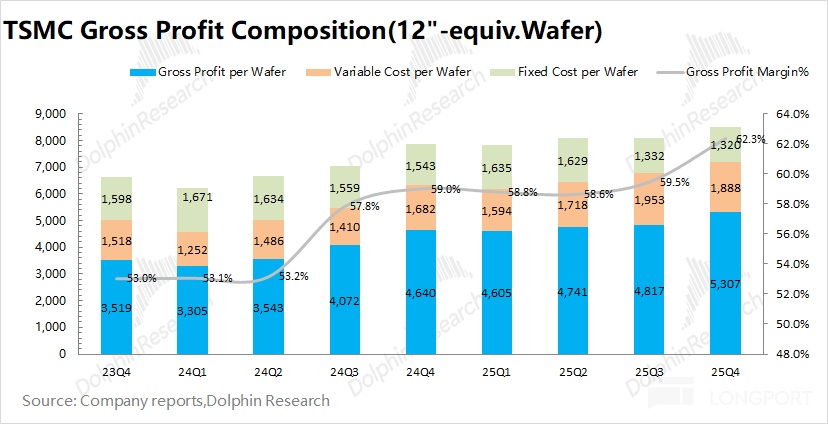

'GP per wafer = ASP per wafer – fixed cost – variable cost'

1) ASP per wafer (12-inch eq.): ASP was ~$8,516/wafer, up $413 QoQ. The uplift reflects new iPhone seasonality and higher 3nm mix.Pricing mix did the heavy lifting.

2) Fixed cost (D&A): Avg. fixed cost was ~$1,320/wafer, down $13 QoQ. On a TWD basis, total D&A was roughly flat QoQ.USD strength reduced D&A in USD terms.

3) Variable cost (other mfg. costs): Avg. variable cost was ~$1,888/wafer, down $64 QoQ. In TWD, unit variable cost was roughly flat; the decline mainly reflects FX translation from a stronger USD.

All in, GP per wafer was ~$5,307, up ~$490 QoQ. Margin gains were driven by higher pricing and lower costs, with the latter largely FX-related.Both sides contributed.

III. Wafer mix: leaning further to advanced nodes

3.1 Revenue mix by end-market

HPC remained the largest contributor at 55% of revenue. Supported by Nvidia's GB-series AI chips, HPC revenue was about $18.55bn and edged down QoQ.Q3–Q4 are peak seasons for smartphones and related devices, so TSMC tilted more shipments to iPhone and other handset customers.

Smartphone revenue was $10.8bn, up 15% QoQ, driven by new iPhone shipments. IoT and consumer electronics also grew QoQ on H2 seasonality.The broad-based uptick reflected typical year-end demand.

3.2 Revenue mix by node

Sub-7nm contributed 77%, underscoring advanced nodes as the core revenue engine. 3nm was 28% and 5nm stayed at 35%.3nm and 5nm are fully loaded; 2nm started initial production in Q4 2025 and will ramp materially in 2026.

As smartphone chips migrate from 3nm to 2nm, AI accelerators are moving from 5nm to 3nm. A forward-shifting node mix should lift ASPs and widen TSMC's advantage vs. peers.This mix shift is structural.

3.3 Revenue mix by region

By region, North America remained the largest at 74%. Anchor customers such as Apple, Nvidia, AMD and Qualcomm underpin deep U.S. ties.This commercial linkage remains robust.

Outside North America, Mainland China and Asia-Pacific each accounted for 9% this quarter. Mainland China revenue was about $3.04bn and remains a top-three region. The customer mix in Mainland China has historically hovered around ~10%.This share was stable.

<End>

Dolphin Research on TSMC

TSMC

Oct 16, 2025 call Trans: 台积电(纪要):2nm 年底量产,明年会加大投资

Oct 16, 2025 earnings First Take: “霸气” 台积电,才是 AI 时代最强王者?

Jul 17, 2025 call Trans: 台积电(纪要):全年营收增速上调至 30%

Jul 17, 2025 earnings First Take: 硬气的台积电,才是半导体真 “脊梁骨”!

Apr 17, 2025 call Trans: 台积电(纪要):未来 30% 的 2 纳米产能将在美国工厂

Apr 17, 2025 earnings First Take: 关税乱战不碍 “爆棚” 指引,台积电稳坐钓鱼台?

Jan 16, 2025 call Trans: 台积电:2025 年资本开支提升至 380-420 亿(24Q4 电话会)

Jan 16, 2025 earnings First Take: 台积电:“定海神针” 已经无敌?

Oct 17, 2024 call Trans: 台积电:完全没有意向收购英特尔(FY24Q3 电话会纪要)

Oct 17, 2024 earnings First Take: 阿斯麦带崩 AI?台积电来镇场了!

Jul 18, 2024 call Trans: 台积电:全年收入增长 20% 以上(24Q2 电话会纪要)

Jul 18, 2024 earnings First Take: ASML 和川普连续 “虚晃两枪”?台积电 “镇场” 还怕啥!

Apr 18, 2024 call Trans: 台积电:资本开支不调整,维持原计划(FY23Q4 电话会纪要)

Apr 18, 2024 earnings First Take: 台积电:iPhone 拉胯,英伟达救场

Jan 18, 2024 call Trans: AI,是未来增长的最强动能(台积电 23Q4 电话会)

Jan 18, 2024 earnings First Take: 台积电:3nm 向前冲,英特尔 “送春风”

Oct 20, 2023 call Trans: 3nm 上量,筹划进军 2nm(台积电 23Q3 电话会)

Oct 20, 2023 earnings First Take: 台积电:熬过 “业绩底”,3nm 战歌起

Jul 20, 2023 call Trans: 台积电:AI 疯狂助力,3nm 终要落地(2Q23 电话会)

Jul 20, 2023 earnings First Take: 台积电:英伟达救场,AI 托起 “周期” 底

Apr 20, 2023 call Trans: 明确二季度见底,3nm 量产在即(台积电 23Q1 电话会)

Apr 20, 2023 earnings First Take: 台积电:最强王者,也难逃周期沉浮

Jan 12, 2023 call Trans: 库存还将调整半年,增长要等到下半年(台积电 22Q4 电话会)

Jan 12, 2023 earnings First Take: 台积电的雷,巴菲特加仓也压不住

Oct 13, 2022 call Trans: 纵然财报亮眼,台积电也避不开行业衰退(三季度电话会)

Oct 13, 2022 earnings First Take: 台积电:暗夜里的 “孤勇者” 到底能挺多久?

Jul 14, 2022 call Trans: 半导体周期下行,台积电如何持续增长?(台积电电话会)

Jul 14, 2022 earnings First Take: 台积电:砍单潮中的 “另类” 傲骨

Apr 14, 2022 call Trans: 2nm 上日程(台积电电话会)

Apr 14, 2022 earnings First Take: 台积电:强势 “信仰”,无关周期

Apr 8, 2022 deep dive: 台积电(下):价格打折,信仰没折

Mar 16, 2022 deep dive: 市场暴跌之后,再谈骨灰级代工王台积电

Jan 13, 2022 call Trans: 给出季度强势指引后,台积电管理层聊了啥?

Jan 13, 2022 earnings First Take: 台积电太能打,“周期” 见了绕道走

Oct 14, 2021 earnings First Take: 台积电:一哥打头阵,风头依旧

Risk disclosure and disclaimer: Dolphin Research Disclaimer and General Disclosures

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.