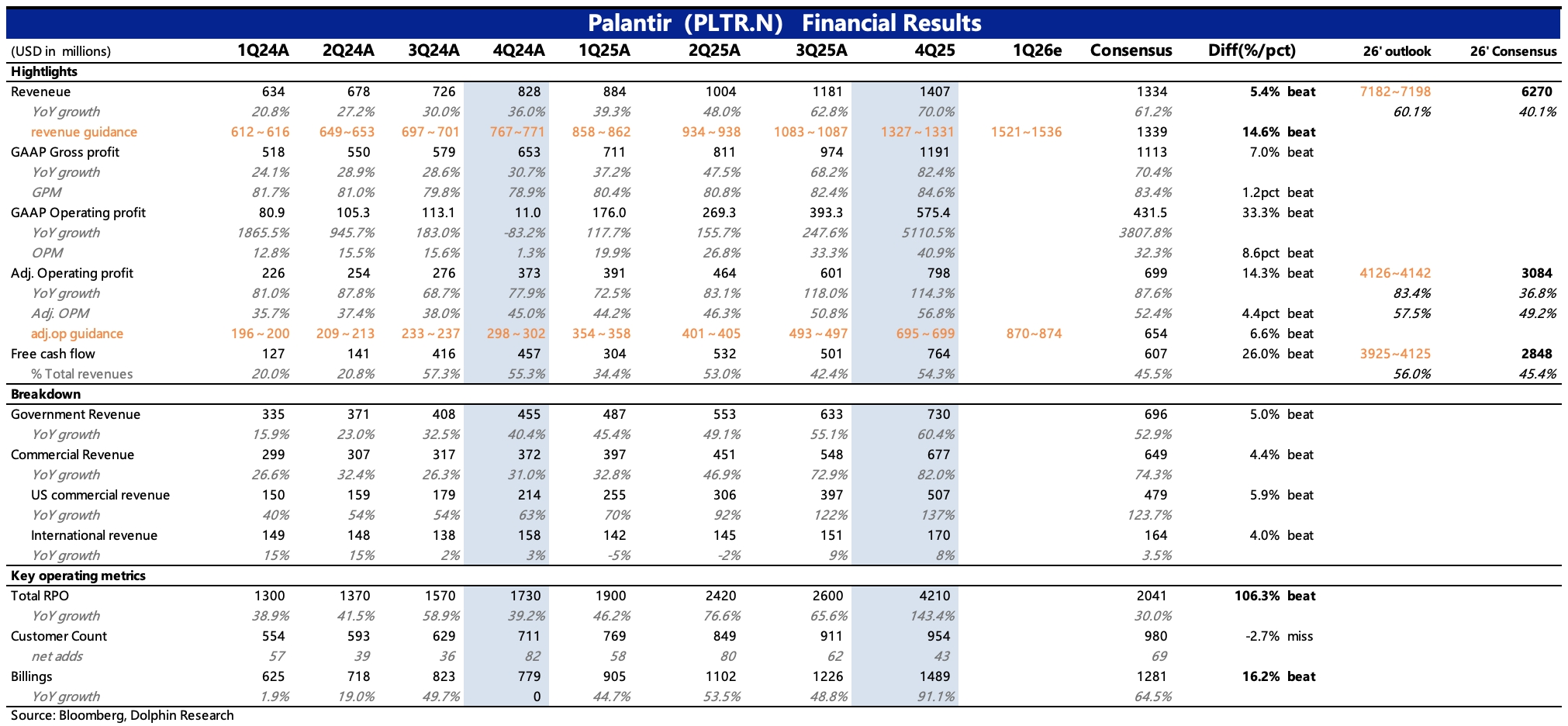

PLTR 4Q25 First Take: Q4 was solid, with key metrics beating. Growth reaccelerated in Q4, easing concerns about the durability of the high-growth profile underpinning its rich multiple.

1) Headline results: Revenue surged 70%, with QoQ acceleration, driven by US customers across Gov. and commercial. Adj. OP was nearly $800 mn, and OPM expanded sharply to 57%, up 4ppts QoQ, helped by higher product GPM and workforce efficiency.

GPM improved by 2ppts. Beyond mix shift, it also signals customer recognition of Palantir's product edge, supporting premium pricing.

The opex ratio also improved by 2ppts. Notably, a deepening partner ecosystem leverages partners' mature sales networks, helping Palantir trim near-term sales costs.

2) By segment: Growth was largely US-led, with commercial up 82% and Gov. up 60%, both meaningful contributors. Non-US regions remained in single-digit growth, with revenue mix down to 24%.

3) Leading indicators: Ample near- and long-term growth fuel. RPO, customer adds, and NDR all look healthy, capturing new demand and retention. Notably, after a pullback last quarter, RPO accelerated in Q4.

4) Outlook: Guidance for Q1 and 2026 corroborates those signals. It points to healthy growth, well ahead of Street expectations. $Palantir Tech(PLTR.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.