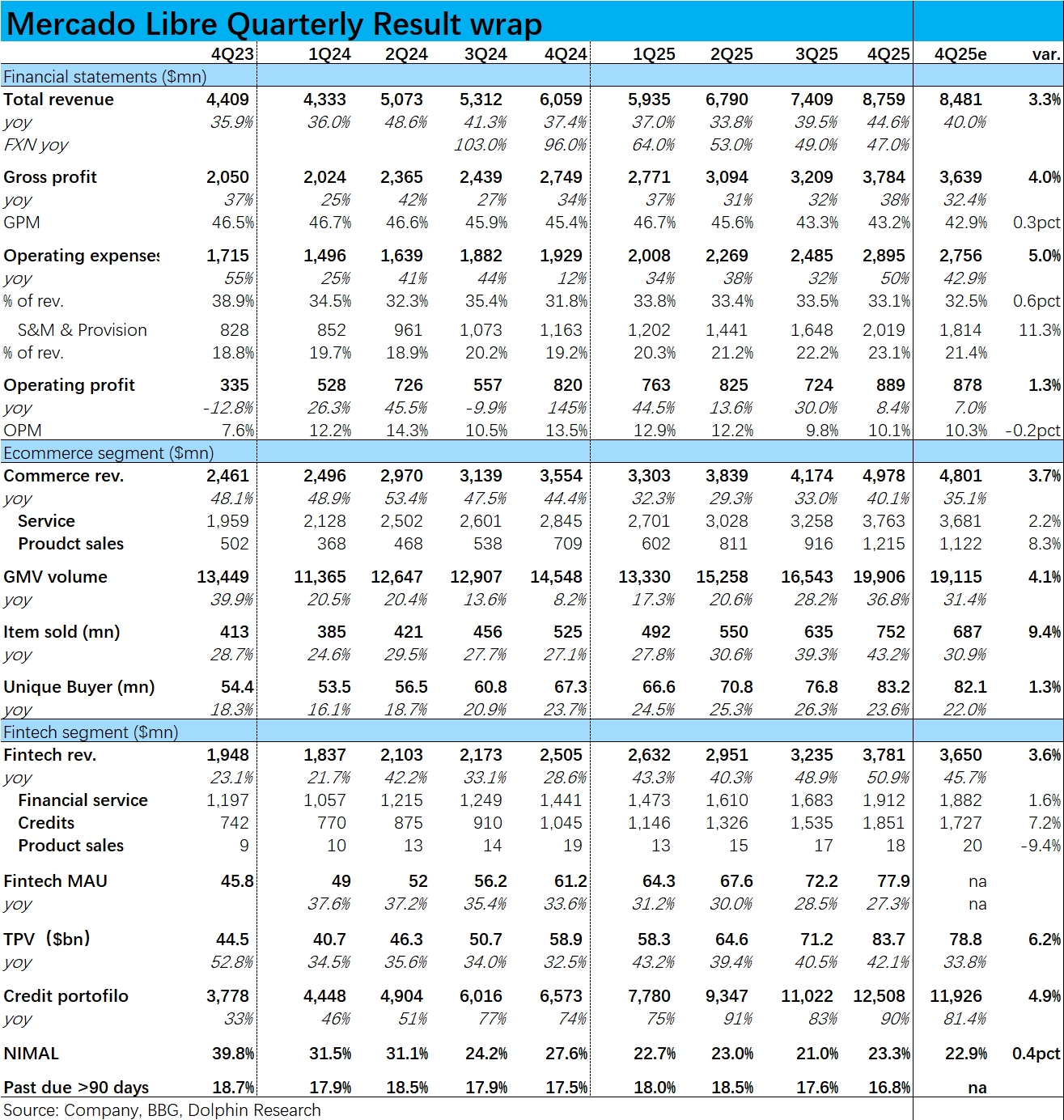

MELI 4Q25 First Take: the LatAm e-commerce leader delivered solid results, with growth metrics strong and beating estimates. However, opex rose sharply, compressing margins — revenue up, profits less so.

1) At the consolidated level, total revenue grew nearly 45% YoY, a clear acceleration vs. last quarter, largely on FX tailwinds. At constant FX, revenue rose 47% YoY, implying a modest 200bps deceleration vs. last quarter.

While topline remained strong, heavy investment in logistics infrastructure, user acquisition, and credit provisioning weighed on margins. GPM contracted ~200bps YoY (in line), and total operating expenses jumped 50% YoY, faster than expected, driving OP to approx. 890 mn, only slightly above estimates, with OPM down by over 300bps YoY.

2) E-commerce: GMV rose nearly 37% YoY, a marked acceleration vs. 28% in Q3, again largely supported by favorable FX. Order growth also improved by 400bps vs. last quarter, pointing to strengthening underlying momentum.

3) Fintech: total payment volume increased ~42% YoY; headline growth nudged higher but was slightly softer at constant FX, effectively stable. Credit loans outstanding continued to surge ~90% YoY, and NIMAL improved QoQ to 23.3% (still lower YoY), mainly on seasonal uplift in loan yields.$Mercadolibre(MELI.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.