Circle 4Q25 First Take: Given USDC supply and disclosed reserve yields, roughly 95% of interest income is predictable. This keeps CRCL’s share price largely tracking USDC, effectively tethered to rate-cut expectations and shifts in crypto policy.

The delta versus expectations in the print lies in non-interest income, internal operating efficiency, and the medium/long-term goals embedded in guidance. These are the true swing factors.

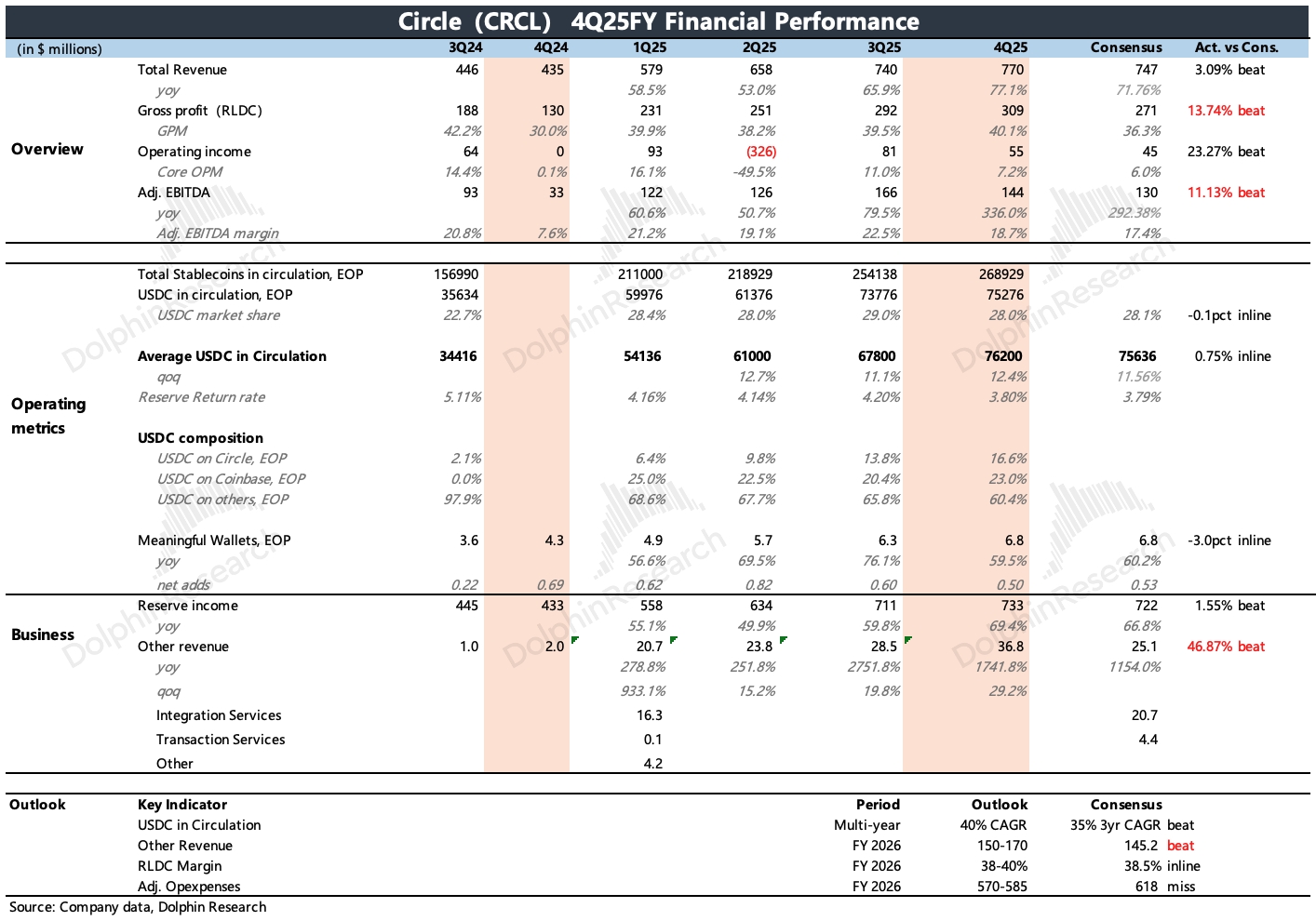

1) Actual Q4 beat, driven by a sharp step-up in 'other income' that accelerated QoQ. Public USDC market-cap data were distorted by outsized crypto drawdowns and outflows, which elevated redemption/burn volumes and led the market to underappreciate USDC’s underlying ecosystem expansion.

Since H2 last year, Circle has been active on external ecosystem build-out. The CPN payments system launched in Apr. already has 55 FIs onboard, with 74 under evaluation; Arc L1 launched in Dec. now has 100+ participants in testing; also in Dec., Circle secured a trust bank license, helping attract more traditional institutions.

2) The market had worried that as Circle expands its ecosystem, it must share reserve interest with partners, while Coinbase disclosed a rising USDC mix, potentially lifting Circle’s channel distribution costs and pressuring GPM. Those concerns were front and center.

In reality, Circle continued to lift its self-held USDC share, mitigating cost pressure. Coupled with software, payments and other infra services that carry high margins, 'other' grew faster this quarter with higher revenue contribution. GPM reached 40%, improving 50bps QoQ.

3) Guidance met overall, with line items slightly ahead. Details below.

(1) On multi-year USDC supply growth, despite volatility late last year and early this year, management still expects ~40% CAGR for multiple years, slightly above the market’s next-3-year view. Dolphin Research suggests this medium/long-term, largely qualitative guide should be taken lightly given market swings, and it does not imply near-term delivery.

(2) 'Other income' came in slightly above, with the company guiding $150–170 mn this year (+46% YoY), and consensus sitting near the low end. Dolphin Research views this as the area with more discretionary push from the company; both guidance and consensus are not demanding, and we look for continued quarterly beats. $Circle(CRCL.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.