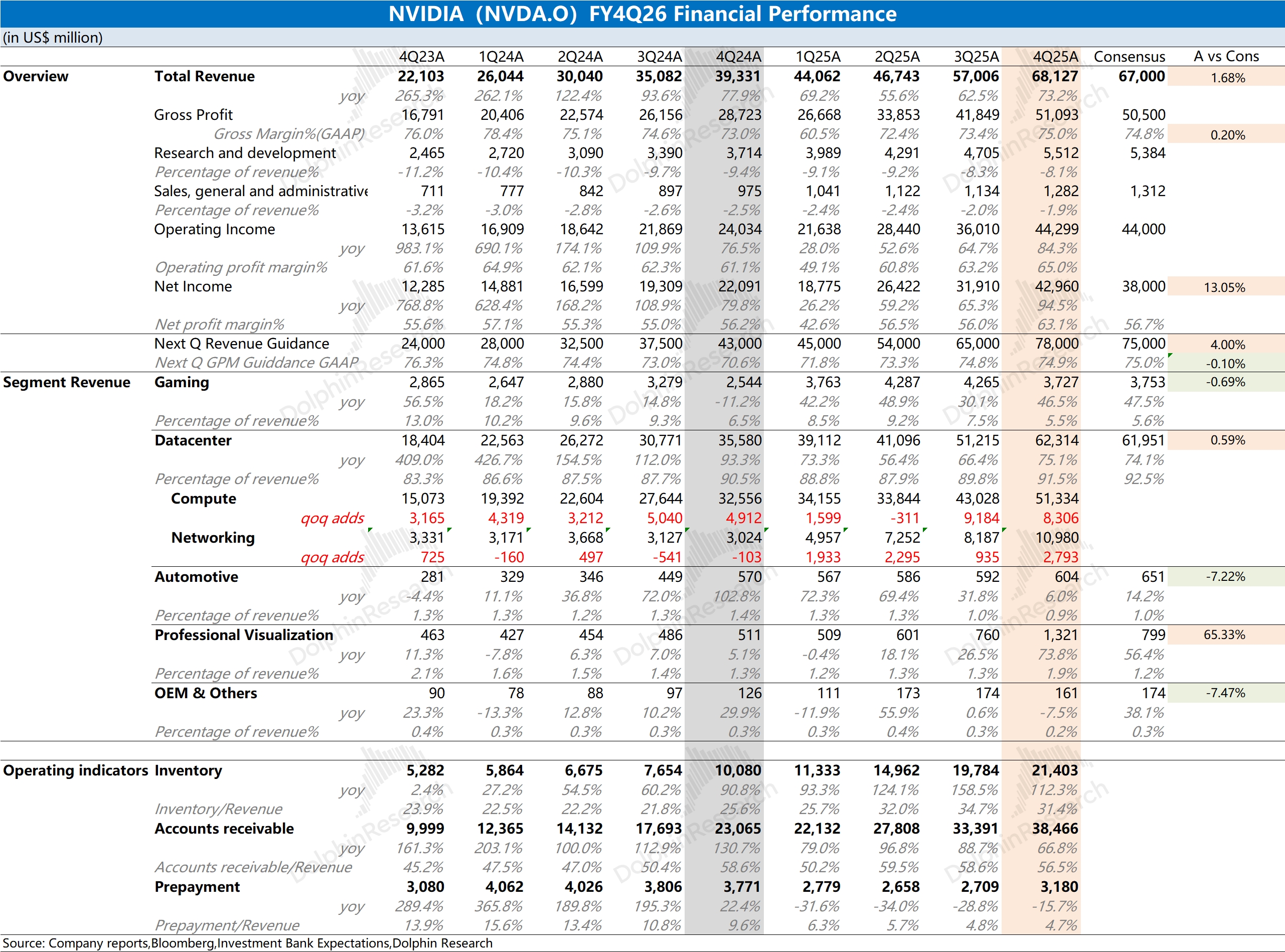

NVDA FY4Q26 First Take: another strong print.

Revenue rose QoQ by $11.1bn, largely driven by Data Center as Blackwell moved into mass production.GPM recovered to 75%.For next quarter, the company guides revenue to $78bn (+/-2%), implying another ~$10bn QoQ increase and beating raised buy-side estimates ($73-76bn).Current flagship products are B300/GB300, and with Rubin launching in 2H, management expects high growth to continue.

Jensen Huang has outlined the AI outlook, targeting cumulative Blackwell + Rubin shipments of 20 mn units by end-2026 (roughly $500bn in revenue).As a result, investors are not worried about FY2027 performance.

Beyond near-term results, the market is focused on NVDA's mid- to long-term competitiveness in AI chips.As large models shift focus from training to inference, customers weigh compute alongside cost-efficiency, and ASIC competitors present potential risks to NVDA GPUs' high share and margins.

Under these concerns, NVDA faces strong growth yet a valuation that has been slow to re-rate.

More importantly, management needs to ease investor worries and reinforce mid- to long-term confidence.For more details, follow Dolphin Research's upcoming commentary and management Trans.$NVIDIA(NVDA.US) $NVDA 2X Long ETF(NVDL.US) $Direxion Daily NVDA Bear 1X ETF(NVDD.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments