VIPS 4Q25 First Take: A warmer winter and a late Lunar New Year weighed on winter apparel sales. Management had already lowered guidance, but the actual print came in worse. Details below.

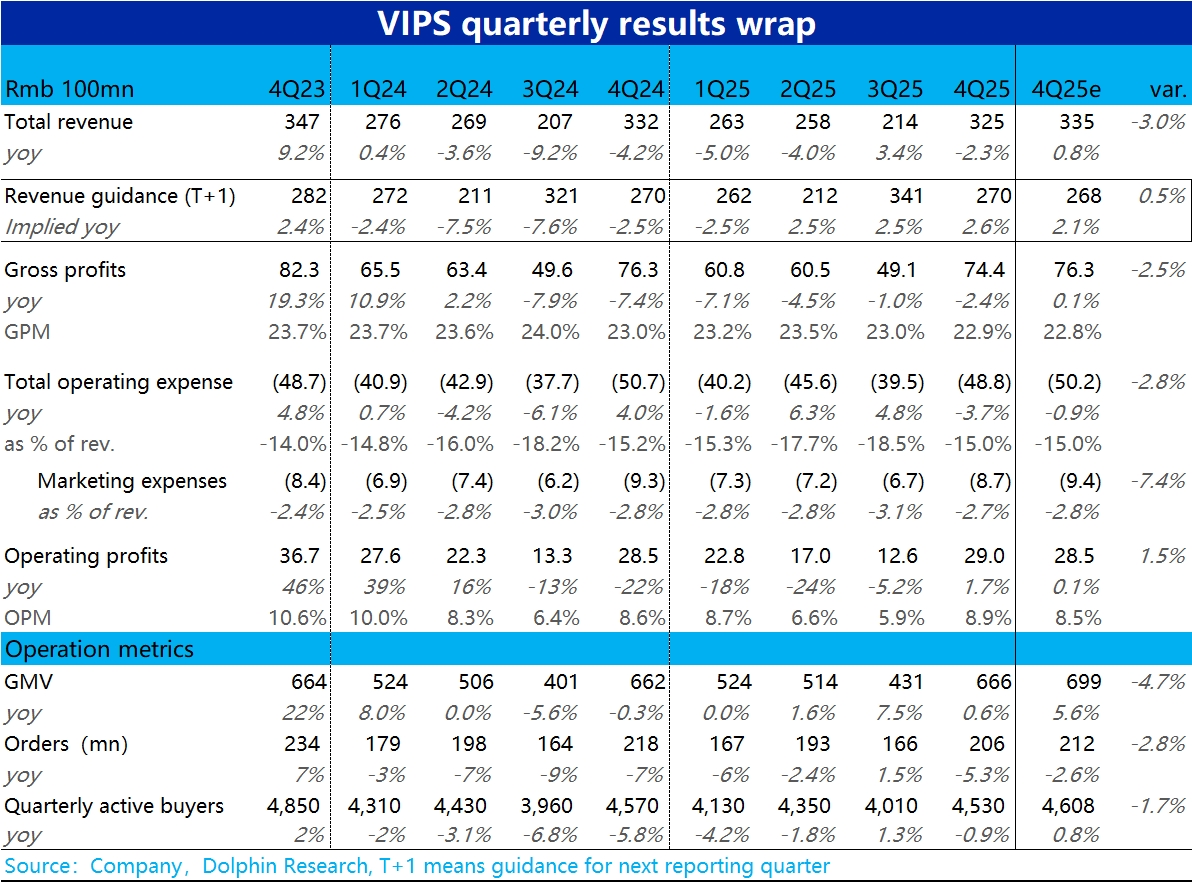

1) Operating metrics turned softer: active buyers declined YoY, down by approx. 0.4 mn. With lower purchase frequency per user, order volume fell 5% YoY.

A higher AOV, likely driven by product mix upgrades and SVIP contribution, barely kept GMV in positive territory. In short, all three metrics missed expectations.2) With GMV lagging, revenue fell 2.3% YoY, worse than the market’s post-cut expectation of sub-+1% growth. The company is no stranger to managing through revenue declines.

Amid weak topline, tight cost control helped: total opex fell 3.7% YoY, a larger drop than revenue, with all expense lines down. As a result, profit still grew +1.7% YoY.

Operating profit reached RMB 2.9 bn, beating market expectations.3) In summary, the quarter was soft, but protecting profitability is commendable. The late Lunar New Year also suggests better sales in 1Q26.

Management guided next quarter revenue mid-point to +2.6% YoY, back to growth and slightly above consensus. Hence, the weak 4Q print should not be overly penalized.On shareholder returns, buybacks totaled approx. $700 mn over the past year, plus ~$250 mn in dividends, exceeding $950 mn in aggregate. That equals about 11% of current market cap.

This provides solid support for the stock. The company also announced it will pay an annual dividend next year of approx. $305 mn, up 22% YoY. $Vipshops(VIPS.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.