MNST 4Q25 First Take: Intl brokers track energy drink category sell-through via Nielsen monthly data and saw continued QoQ improvement in both buyer penetration and purchase frequency in Q4. In N. America, household penetration for Monster hit a record high of 33%. As a result, Street expectations heading into the print were elevated.

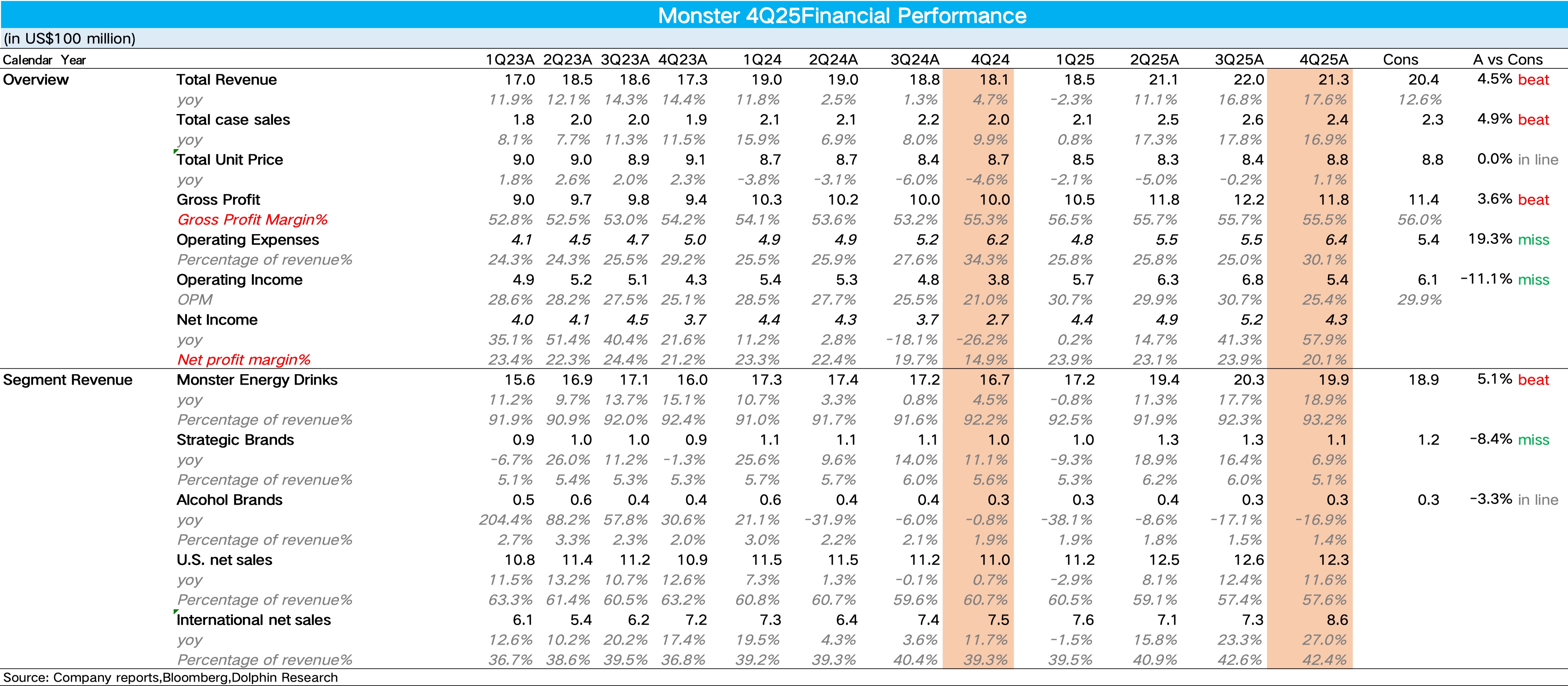

On actuals, revenue beat and remained strong. However, unlike Q3, higher spending drove a slight miss on the profit line.

1) Revenue rose 17.6% YoY, the fastest quarterly growth in nearly three years. By volume/price, unit case volume was up 16.9% YoY, extending Q3’s high-growth trend.

Drivers were twofold: the energy drink category continues to gain global penetration on health and functionality trends. At the company level, a pivot toward health-oriented SKUs and faster innovation captured incremental, health-conscious consumers.

Pricing increased 1.1% YoY. In the core N. American market, MNST implemented varied price hikes by pack size and subcategory while pulling back on promotions.

2) Intl mix kept rising. By brand, the Monster core franchise grew 18.9% YoY, outpacing the category, helped by flavor innovation that resonated with fashion- and fitness-focused female consumers. Other strategic brands rose 6.9% YoY, with slower QoQ growth.

By region, Intl revenue grew 27% YoY and mix increased to 42.4%, supported by deeper leverage of Coca-Cola’s global distribution network. U.S. revenue rose 11.6% YoY, sustaining double-digit growth.

3) Spending modestly exceeded expectations. GPM was stable as mix upgrades and modest pricing offset higher input costs such as aluminum cans.

On opex, heavier sponsorship in Q4, plus launches like Storm, pushed expenses slightly above expectations, resulting in OP modestly below the Street. For more details, follow Dolphin Research’s deep dive and the earnings call content $Monster Beverage(MNST.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.