Block 4Q25 First Take: Beyond the print, the company announced two major moves this quarter. First, it will lay off 40% of staff, cutting headcount from just over 10k to roughly 6k. Management said the business is improving, so the decision is not financial, but to boost organizational agility and leverage AI tools for much higher productivity.

Separately, the company changed its reporting taxonomy. Headline segments remain Square merchant / Cash App / Other, but sub-categories shift from transaction/service/hardware/crypto to commerce-related/financial-related/Bitcoin-related. Historical financials were adjusted modestly, and we will reference legacy taxonomy for this quarter.

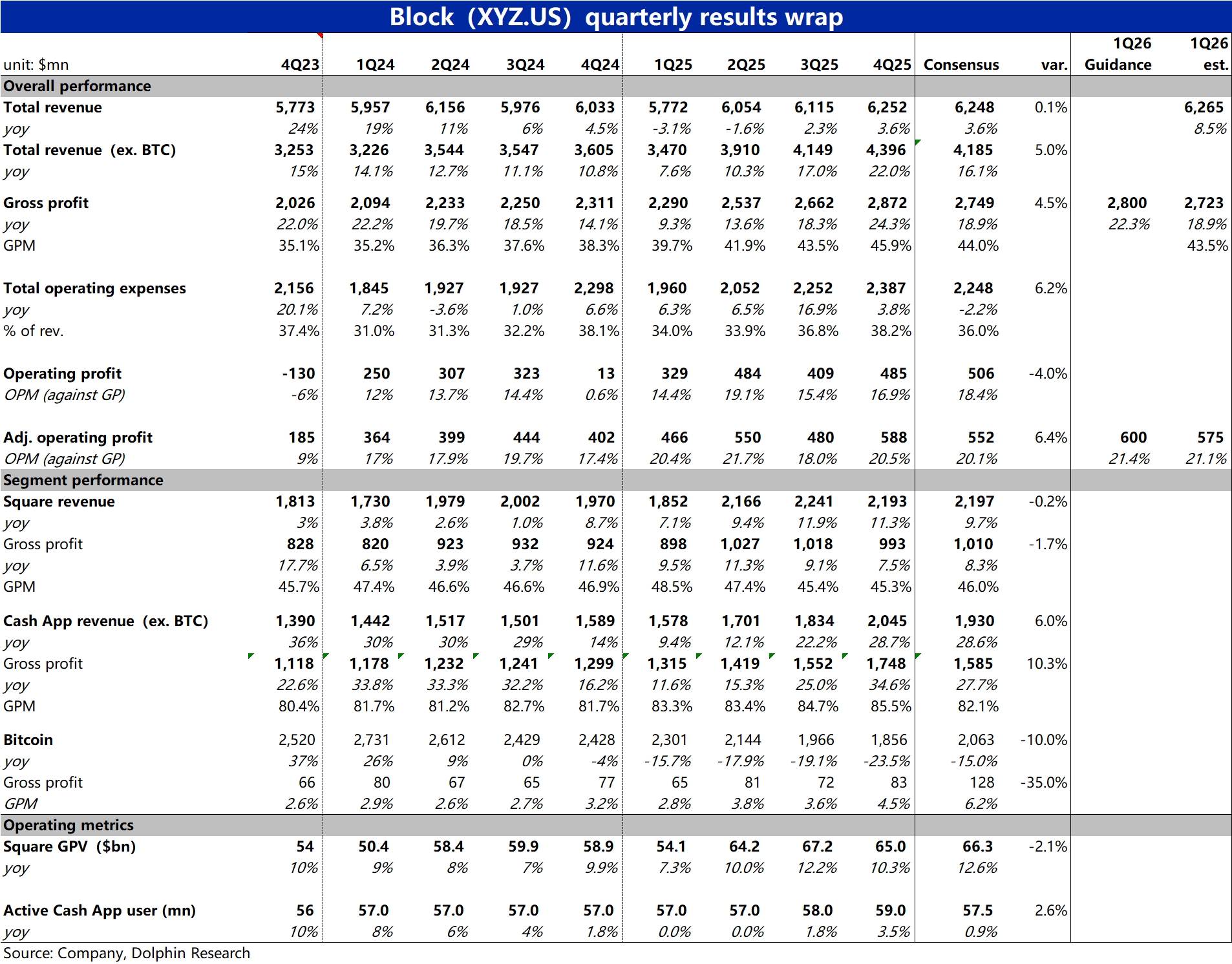

Overall, results were solid. Core revenue ex-Bitcoin rose 22% YoY, beating the Street by ~5pct. GP grew 24% YoY, also ~5pct above estimates, with GPM continuing to improve on better mix and operating efficiency.

A small blemish was opex coming in above Bloomberg consensus, largely because estimates were too low (–2% YoY). Actual opex rose 3.8% YoY, with no meaningful step-up in investment. On an Adj. OP basis, results still beat.

By segment, Square merchant was soft, with revenue and GP both below expectations. The drag came from a QoQ slowdown in GPV growth. The bright spot was Cash App, with revenue and GP materially above estimates, as active users, inflows, and transaction counts all improved broadly.

Guidance for next quarter was also above. The company guided GP of $2.8bn (+22% YoY), ~3% above consensus, and Adj. OP of $600mn vs. $575mn expected. The implied OPM is roughly in line, with OP outperformance driven by the stronger GP guide. $Block(XYZ.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.