MNST (Trans): Zero-sugar line remains the core growth driver ---

Below is Dolphin Research's transcript of MNST FY25 Q4 earnings call. For the earnings take, see Monster Beverage: A new product cycle ahead — another major year of 'evolution'?.$Monster Beverage(MNST.US)

- Core takeaways from the print

II. Detailed call notes

2.1 Management highlights

1. Monster Energy beverages

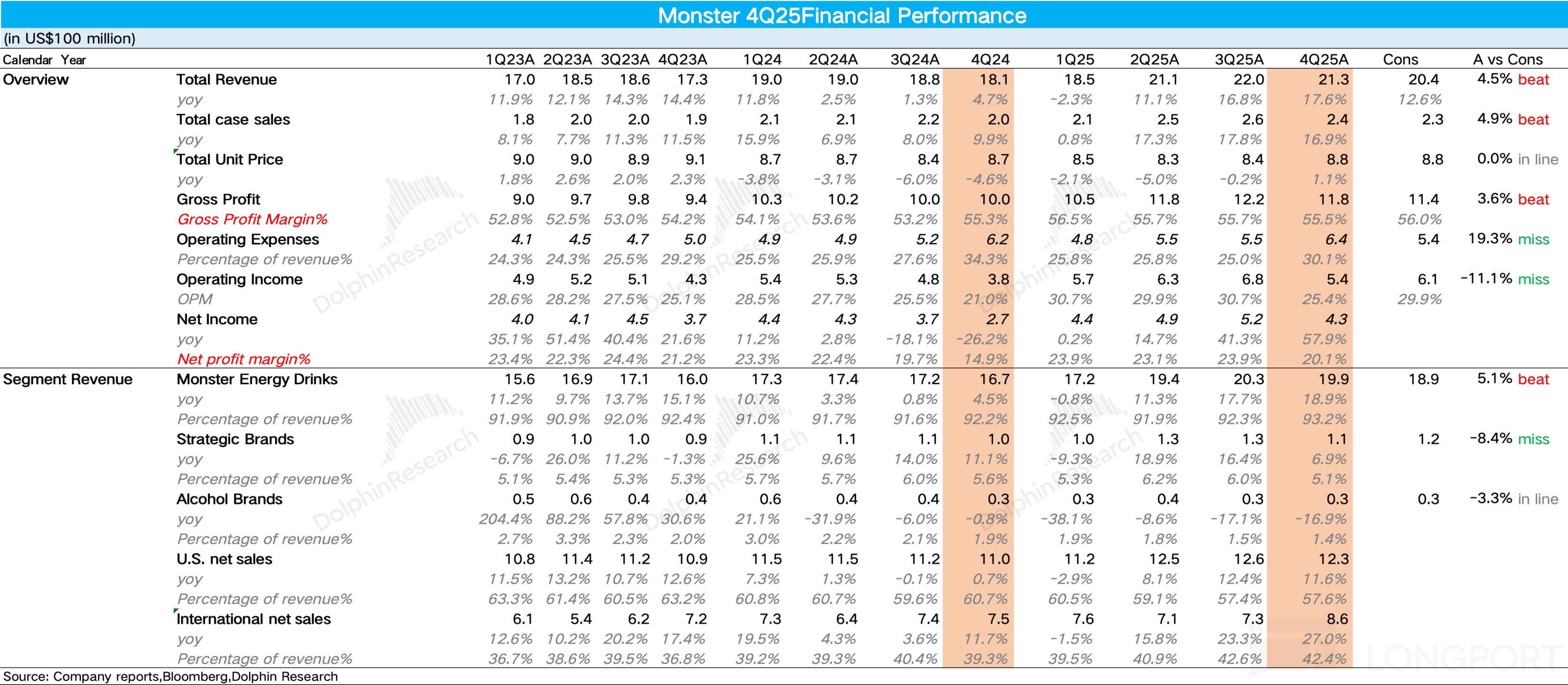

a. Revenue: Revenue reached $1.99bn, +18.9% YoY. FX-adjusted +17.5%.

b. Growth drivers:

- Zero Sugar remains the core growth engine, with Ultra up 24% in the U.S. and flagship Ultra White +32%. Momentum stayed broad-based across channels.

- Sugared lineup: Contributed one-third of U.S. incremental growth. Juice Monster surged 37%.

c. Innovation: Ultra Wild Passion and the America 250 commemorative series performed well. Reign has entered 38 EMEA markets and is set for a full U.S. rollout.

2. Strategic Brands:

a. Revenue: Revenue was $110mn, +7.8% YoY. Growth was supported by mix and distribution gains.

b. Value matrix: Strong in Africa (Predator, Fury), now the No.1 value energy brand in the region. The company is accelerating value-brand penetration into China and India.

3. Alcohol Brands:

a. Revenue: Revenue was $29mn, down 16.8% YoY. Trends reflect portfolio transition.

b. Update: Ongoing rebranding and new product testing, including Hot Lemonade and Beast Perfect 10. Related impairments were booked this quarter, lifting reported G&A.

4. Global regions

a. North America: Revenue +13.3%. A targeted price move on Nov 1 improved revenue quality with minimal volume impact.

b. EMEA: Revenue +32.6%. Monster leads Western Europe in category growth.

c. APAC: Revenue +11.5%. Execution and innovation supported broad-based gains.

d. Japan: A distributor system issue temporarily drove a 15.2% decline, which normalized in Feb. No structural change in demand.

e. China/India: Standout. China revenue +78.9% YoY, India +54.2%.

f. LATAM: Revenue +90.8% (material FX impact). Share hit record highs in Brazil and Chile.

2.2 Q&A

Q: What is driving the acceleration in Intl share gains and how sustainable is it? Also, how is the Affordable Energy strategy performing in EMs, and how does it expand the category and add incremental growth?

A: Affordable Energy is our differentiated approach for markets where core Monster pricing is out of reach. We keep Monster as a premium leader and do not plan to lower it into value tiers. Value is growing well, with global volume expected to reach 100mn unit cases in 2025, a first-time disclosure. With most of the world living in developing markets, this is a major opportunity, led by Nigeria, Egypt, Kenya, Mexico, India, and China.

Globally, energy drinks are posting strong double-digit growth. Consumers respond to the category’s value proposition and cross-age, multi-occasion utility. About 25% of buyers over the past 12 months were new to the category. Monster continues to outperform the category, driven by core SKUs and innovation.

In Europe, two-thirds of our growth comes from existing business, with one-third from innovation, while peers rely more on new products. Ultra grew Nielsen sales 53% in Q4, with Ultra White +59%, underscoring Zero Sugar and core SKUs’ momentum. The Lando Norris Zero Sugar product lifts usage frequency among existing users and is highly incremental.

Specifically, 25% of its sales came from category newcomers and another 25% from brand-new buyers. With a sugared and zero-sugar portfolio that spans multiple occasions, we are growing ahead of the industry.

Q: For 2026 in the U.S., what are the growth drivers, shelf-space outlook, and margin trajectory?

A: While we do not provide formal guidance, the fundamentals behind sustained growth are clear. Versus CSDs and coffee, energy offers superior value and functional benefits. Rising household penetration and innovation remain key growth drivers.

More importantly, consumption is shifting from specific occasions to 'day parts', increasing frequency and unlocking long-term runway. In 2026, we will focus on pricing, sustained innovation, and deeper FSOP penetration. We remain constructive on category opportunities.

On shelf space, retailers allocate based on data-driven performance. With energy outgrowing other drinks, we expect continued shelf expansion, taking space from weaker alcohol and soft drinks. We adhere to an 'innovation equals incremental' strategy: new SKUs must secure extra display space rather than displace core products, ensuring pure incremental growth.

Q: Gross margin expanded this quarter despite tariffs and inflation. What offset the headwinds, and how should we think about the trend?

A: GPM improved mainly on pricing, supply-chain efficiencies, and mix, particularly higher Zero Sugar share. Aluminum costs, the Midwest Premium, and Rotterdam premiums rose, and a higher Intl mix diluted margins modestly. These headwinds were largely offset by pricing. Philosophically, we prioritize dollar profit over percentage margin.

We actively hedge aluminum, and all operating analyses are net of hedges. Aluminum (including premiums) is up over 50% from Q4 2025 to early 2026, and this pressure likely persists through 1H26. We expect cost pressure in Q1–Q2 2026 to be slightly above this quarter, then ease in 2H as we lap the high-cost base of 2025.

Q: G&A delevered despite strong top-line. Which investments are ongoing vs. one-time?

A: G&A volatility reflects three specific items: $12.9mn linked to performance-based awards, approx. $5.1mn of professional fees tied to the AFF San Fernando plant start-up, and $6.6mn for digital transformation. Some digital spend will be capitalized going forward, with a portion remaining in G&A.

Ex these items, G&A as a percent of sales is actually declining. Operational leverage remains healthy. We continue to invest behind growth with discipline.

Q: Will you take additional pricing to offset cost inflation?

A: We continuously assess pricing opportunities domestically and internationally. Decisions follow our cadence and balance company economics, distributor dynamics, and consumer acceptance. The Nov 1, 2025 price increase executed well, met expectations, and did not dent volumes.

Q: Will 2026 innovation be concentrated in one half or spread through the year? How are recent launches performing on repeat rates?

A: We are taking a phased, staggered approach this year rather than clustering all launches at the start. Announced products will roll through H1, with unannounced items following in the fall. The America 250 series has already landed with select retailers and will scale alongside the celebrations.

We closely track innovation performance. Repeat metrics and market feedback are encouraging, and we remain optimistic about the pipeline. Execution will be paced to maintain incrementality and velocity.

Q: Update on India and the long-term vision and principles for working with new bottlers?

A: We are very excited about India. We maintain tight collaboration with The Coca-Cola Company in Atlanta, Coca-Cola India, and local bottlers to activate and accelerate growth. New bottlers are highly engaged, and I have personally met their CEO multiple times.

Strategically, we and the bottler are aligned on India’s opportunities. We will compete with a dual-brand approach, Monster and Predator. The objective is clear: confront the main competitor (a certain famous blue can) and take share.

Q: Considering aluminum hedging and recent price moves, plus Intl expansion and higher Affordable Energy mix, how should we think about geography and product mix impacts on margins?

A: As noted, we expect margin pressure in Q1–Q2 2026, with no further update at this time. From the financials, all reported regions showed GPM expansion. For Affordable Energy, it actually helps margin uplift, which is why we prioritize it outside the U.S.

While many Intl markets cannot support U.S.-like premium pricing, we focus on optimization to raise margins. Last quarter’s results already demonstrated early proof points. We will continue to balance growth, mix, and pricing.

<End here>

Risk disclosure and statements:Dolphin Research disclaimer and general disclosures

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.