CoreWeave (Trans): Massive capex fully backed by signed service contracts

Below is Dolphin Research's Trans of $Coreweave.US FY25 Q4 earnings call. For our earnings analysis, please see 'CoreWeave: Orders Surge, Profits Dive — Is the compute unicorn stuck in a profitability loop?'.

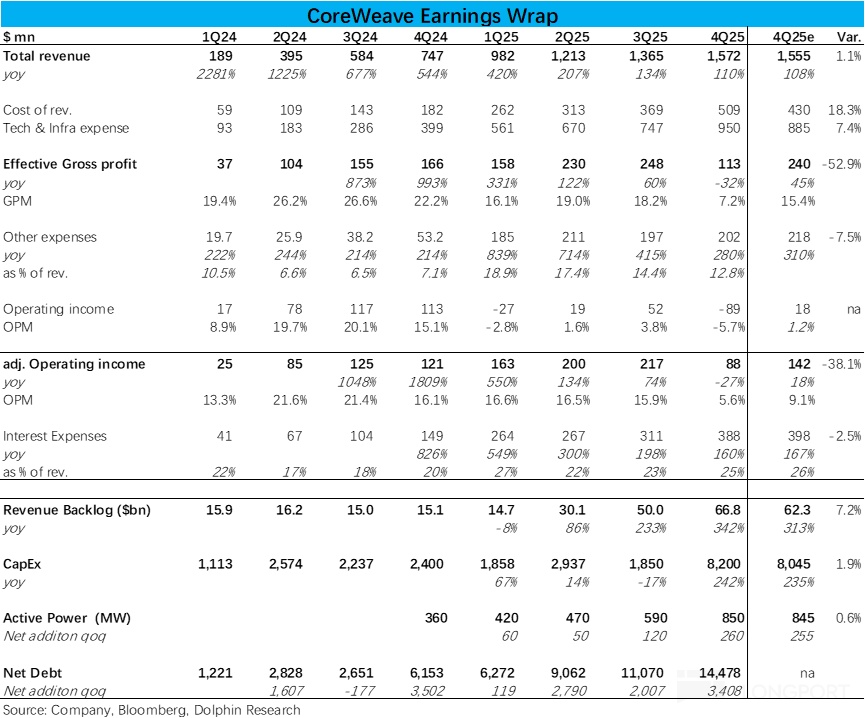

Key financials recap

Cash & marketable securities: $4.2bn as of Dec 31. Balance at period end.

Financing activities:

Issued convertible preferred notes in Q4, raising Approx. $2.6bn. This was in Q4.

Expanded the revolving credit facility to $2.5bn. Facility capacity increased.

Secured over $18bn of debt and equity financing in 2025. Funding mix diversified.

In Jan, NVIDIA announced a $2bn investment in CoreWeave. Strategic capital infusion.

Cost of funds: Wtd avg interest rate fell by 300bps in 2025 (nearly 600bps cumulative since 2023). Trend improving.

Call details

2.1 Management highlights

1) Market backdrop & demand

Demand remains strong and broad-based: hyperscalers, AI-native, and enterprise customers are all accelerating. New reserved instance customers in Q4 were roughly 2x any prior quarter, including Cognition, Cursor, Mercado Libre, Midjourney, and Runway.

Customer base expansion: The number of customers committing at least $1mn of spend on CoreWeave Cloud grew nearly 150% YoY. These are durable platform relationships, not one-off deployments.

Pricing steady: Pricing held stable through 2025 and is expected to remain so into 2026. Demand and pricing for prior-gen GPUs like H100 and A100 remain firm for inference use cases, with new contracts signed.

Long-term outlook: Given strong demand signals, the roadmap is being accelerated. The goal is to add over 5GW of incremental data center capacity beyond the contracted footprint by 2030.

2) Platform evolution & product strategy

New monetization avenues: The company is expanding beyond GPUs into CPU, storage, and software, and licensing its proprietary cloud stack to third parties to unlock margin-accretive growth. This opens new profit pools.

Cross-sell traction: Roughly 80% of large customers (≥$1mn annual spend) have adopted one or more CoreWeave storage products. The partnership with Weights & Biases added several hundred million dollars of incremental contract value.

Value of the proprietary cloud stack: The company is accelerating development of its stack, including SUNK and Mission Control. In Jan, NVIDIA announced plans to test and validate CoreWeave's platform for inclusion in its reference architecture.

Some customers have licensed SUNK as their multi-cloud research cluster management platform. The company expects this to be a high-margin revenue driver, and this upside is not included in the 2026 guide.

Maintaining technical leadership:

In Q4, CoreWeave became the first cloud platform to reach NVIDIA GB200 'exemplar cloud' status, and it remains SemiAnalysis's only platinum-grade AI cloud. Technical leadership remains a key differentiator.

It expects to be among the first to bring NVIDIA Rubin GPUs to market in 2H26, and plans to expand into NVIDIA's Vera CPU and BlueField storage. Product breadth will deepen.

3) Infrastructure expansion

Rapid scale-up: Roughly 2GW of additional power was contracted in 2025, taking contracted capacity to over 3.1GW by year-end. The vast majority is expected online by end-2027.

Latency issues addressed: Data center latency discussed last quarter was resolved quickly, with impacted deployments completed ahead of schedule. Over 50,000 Grace Blackwell units have been delivered to affected customers.

Scale and speed: Over 260MW went live in a single quarter, spanning 100k+ GPUs and millions of interconnect components. Execution speed and reliability are core strengths, with scale exceeding the combined footprint of the 15 largest upstart clouds in North America and Europe.

4) Outlook

Investments tied to demand: 2026 capex is expected at ≥$30bn, directly supporting contracted revenue backlog of $66.8bn. Capex will be financed primarily via asset-level delayed-draw term loans.

FY26 guidance:

Revenue: $12–13bn (midpoint ~+140% YoY). Growth driven by backlog conversion.

Adj. OP: $0.9–1.1bn. Profitability to improve over the year.

Margin trajectory: Starting low-single-digit in Q1, expanding sequentially to low-teens by Q4. Management remains confident in a long-term 25–30% margin profile.

Exclusions: Guidance excludes any material revenue or profit from licensing the proprietary CoreWeave cloud stack. Potential upside is not embedded.

Q1 FY26 guidance:

Revenue: $1.9–2.0bn. Early-year ramp.

Adj. OP: $0–40mn. This is the trough in the annual margin trajectory, given $6–7bn of infrastructure capex in the quarter and significant new capacity coming online.

Interest expense: $510–590mn. Reflects funding scale.

Long-term revenue outlook:

Exit-2026 annualized run-rate revenue of $17–19bn. Supported by contracted demand.

Exit-2027 annualized run-rate revenue expected to exceed $30bn. Management emphasized these targets are underpinned by customer contracts.

2.2 Q&A

Q: Capex surprised to the upside, and delivery delays were resolved faster than expected. Yet the online capacity and revenue guide do not seem to reflect typical upside. Can you explain these dynamics?

A: A large portion of capacity went live late in the quarter, so monetization will show up starting in 2026. We will continue deploying at a rapid pace throughout 2026, including Q1, which is the impact you are seeing.

Q: With capex >$30bn this year, how should we think about funding cost and current WACC as capacity scales? How has this changed over the past 12 months?

In negotiations with data center operators, how is credit assessed — primarily based on customer contracts and logos, or other factors? Also, will NVIDIA's credit support (guarantor framework) measurably lower borrowing costs in 2026?

A: As the business matures, with a growing operating track record, deeper customer collaboration, and infrastructure delivery experience, we have made significant progress. Cost of capital declined 300bps over the last 12 months and 600bps over two years, and we expect this trend to continue. This is driven by better performance under our ETL structure.

On data centers, we added nearly 2GW of infrastructure contracts in 2025, vs. 1.3GW at end-2024. Our ability to secure, build, and advance DC contracts has improved materially, which is a key milestone. Signing such large-scale DC capacity reflects business maturity and enhanced credit and scale.

DC operators are very willing to work with CoreWeave. They seek diversified tenant mixes and exposure to large-scale AI infrastructure delivery, and view CoreWeave as a pure way to gain AI scale-up exposure.

Regarding NVIDIA, partnering with an investment-grade counterparty to offtake capacity clearly impacts capital or DC-related costs. We selectively (not exclusively) partner with NVIDIA in building the DC footprint, which should positively affect our DC cost base.

Q: Recent AI models have shown major advances, e.g., Claude Code, but we have not seen models deeply trained entirely on CoreWeave's largest Blackwell/GB200/NVL DCs yet. From the market chatter, how are Blackwell-based models progressing? If GPT-6 or others launch in 3–6 months, do you expect a step-function or steadier progress on Blackwell systems?

A: Blackwell systems are outstanding. They represent the next compute step-change, enabling data scientists and model companies to build and scale infrastructure in unprecedented ways.

Signals from model companies suggest performance gains are only beginning. Grace Blackwell deployments are still early, and clusters of the scale we delivered are not yet widespread.

As these clusters come online across our portfolio and globally, we expect step-change performance from the new technology. Customers are very excited, recognizing what they can do with superior performance for training and, subsequently, inference.

Q: On inference, how do you view focusing on NVIDIA's reference architecture? It is extremely strong for large-scale training. On the other hand, would you lean toward custom ASICs that appear more cost-effective for inference? Does NVIDIA's acquisition of Groq change the landscape, potentially letting NVIDIA's reference architecture dominate inference too?

A: Our model is deeply customer-led. Customers specify the AI infrastructure they need to drive their businesses, and they select CoreWeave for our ability to deliver high-performance NVIDIA technology.

Do they explore other vendors and technologies? That is reasonable. But current demand signals for what we deliver are overwhelming.

We will stay focused on our existing high-performance solution set, which over the past three years has stretched delivery capacity for us and the broader market.

Q: On guidance, revenue is in line but profitability is lower, while capex is far above expectations. This suggests metrics may swing materially even with a guide. How should we think about guidance going forward? Were Q4 variables resolved, and has the guide changed?

A: Think about guidance across several variables. Capex fundamentally serves contracted customer backlog, which was $66.8bn this quarter and underpins platform investment.

On revenue growth, almost all backlog contracts begin generating revenue this year. We brought 850MW online in FY25, and expect ~1.7GW in 2026.

On margins, the trajectory reflects deliberate investment to meet voracious platform demand. With ~30% of total active power going live in Q4, capacity costs precede full revenue maturity, which naturally compresses margins near term.

As noted, Q1 is the margin trough. Margins expand sequentially as deployed capacity scales, returning to low-teens by Q4.

Strategically, we invest against contracted demand and backlog. As growth normalizes, we remain confident in 25–30% margins long term, with mature, fully ramped contract mixes contributing ~25% GP.

Margin-accretive products and services in the mix continue to grow, e.g., storage ARR now tops $100mn, with 80% attach among large customers. While not included in the 2026 guide, we see tangible long-term upside from monetizing the CoreWeave stack across other NVIDIA clouds, enterprises, and sovereigns. 2026 reflects growth acceleration driven by existing backlog.

Q: On capex and margins, the market is focused on heavy current capex vs. limited near-term margins or cash flow, and you target 20–25% long-term margins.

How confident are you in the capex ramp? As margins improve, could growth be calmer than expected? Do you need to keep capex above market expectations to reach targets?

A: Two parts. First, the business is built on a pay-for-success model, with customers signing long-term contracts for infrastructure.

Hyperscalers signing 5-year infrastructure contracts purchase at fixed prices. This is a very stable way to build revenue and margins, giving visibility over the 5-year horizon and enabling capital market access to fund builds — CoreWeave's foundational module since inception.

Second, the implicit question is confidence in sustained compute infrastructure demand. Demand is broadening across the economy, expanding from hyperscalers and base models into enterprise and sovereigns, with many new entrants locking in capacity.

Demand is also expanding beyond the initial GPU wave into storage and CPU, reflecting customer use extending into the application layer. We have a pulse only few global companies have, drawing insights from across the economy, which reinforces confidence in contracts and in diverse customer and compute types.

A few data points: 2026 capex is almost entirely tied to signed customer contracts slated to go live this year, doubling deployed power. From an EBITDA margin lens, this quarter was 57%.

Long-term contracted customers contribute ~25% margin, and those contracts carry EBITDA margins in the ~70% range. As contracts scale, we expect substantial cash flow.

Q: Looking ahead to Rubin contracts, are you seeing similar 5-year demand? How do pricing and prepayment expectations differ? How should we think about ROI vs. prior generations and the economics outlined in the S-1?

A: One clear trend is contract terms extending from an Avg. 4 years to an Avg. 5 years. This enhances business stability and gives confidence to build and expand infrastructure.

On pricing, we target margins. As infrastructure costs move, we adjust customer pricing to align with Nitin's margin targets. On prepayments, this remains a negotiable lever to shape contract economics, and as capital costs decline, reliance on prepay is reduced.

Q: What gives you confidence in $30bn run-rate revenue by 2027? How much is already contracted vs. to be won? And how are you prioritizing across segments as demand evolves?

A: On demand, we maintain a diversified view of compute use, engaging broadly with compute consumers for the best insight into demand sources. As compute access improves, new companies and ideas will emerge and become customers, and we aim to support them from day one.

On the $30bn target, we forecast based on contracted power capacity, existing sold contracts progressing (2026 capacity is largely sold), and ongoing additions to allocate after capacity comes online in 2027.

Customer appetite to secure more capacity and bring in more compute is large and sustained, including the world's most trusted companies and leading AI labs. On this basis, we are highly confident in the $30bn target.

<End of text>

Risk disclosure & statements:Dolphin Research disclaimer & general disclosure