Good news for Buff Stacking, Is Meta taking a sharp turn?

Hello everyone, I am Dolphin Analyst!

On the morning of February 2nd (Beijing time), $Meta.US released its Q4 financial report for 2022. As expected, $Snap.US issued an earnings warning again before the report was released, which affected other advertising companies. The stock performance in the past two days has been weaker than the market. However, it can be seen from the 18% surge in Meta's stock price after hours that there are many positive signals released in this financial report when carefully analyzed by the Dolphin Analyst.

The core points of this financial report are summarized as follows:

1. Revenue exceeds expectations, possibly due to Reels. Meta's total revenue for Q4 was in line with guidance, but the market was too conservative and the consensus expectation was given below the guidance level. It is estimated that the market was scared by Meta's frequent earnings warnings and macroeconomic pressures last year. For the Q1 2023 guidance, the market expectation (~27.2B) was just in the middle of the guidance (~26-28.5B). However, given the current situation, the market will definitely adjust revenue expectations after the financial report is released.

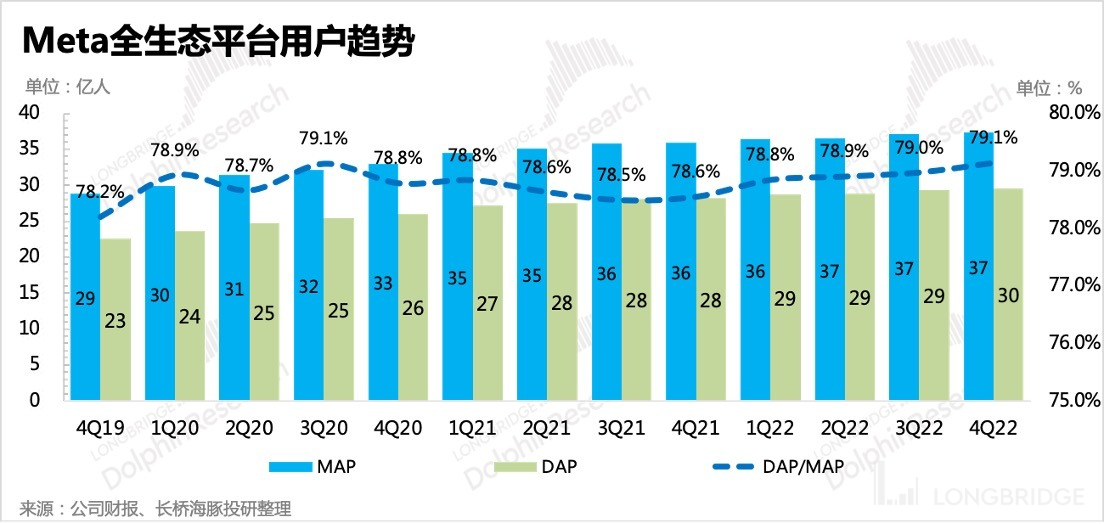

2. Stable traffic growth, with the main site as the source of active growth. In Q4, Meta's ecosystem users reached 3.74 billion, with 2 billion daily active users and slightly improved user stickiness. Facebook's main site was the main source of incremental users. With the further improvement of the Facebook Reels function and its prominent position, the high stickiness of short videos helps to promote user social activity.

3. Strong expenditure reduction, with significantly improved actual profitability. After the continuous investment in the metaverse caused dissatisfaction among shareholders, Meta quickly launched a large-scale layoff and lowered the expenditure guidance. The Q4 expenditure on cost items such as layoffs, business restructuring, and new data center investment accounted for a drag of nearly 13 percentage points on the operating profit margin. However, after adding these back, the actual profitability level is almost back to the Q4 2021 level.

Regarding the expenditure guidance for this year, Meta made another adjustment this time, and both the total operating expenditure and capital expenditure were lower than market expectations. For shareholders who are more concerned about revenue this year, this is a pleasant surprise.

4. A new repurchase plan of 40 billion was added. The repurchase plan for Q4 was originally carried out as usual, with a remaining quota of 10.8 billion. However, the company added a new 40 billion repurchase plan to reward shareholders.

The free cash flow recovered to 5.3 billion in Q4, and with the compensation for layoffs and business restructuring expenses, it has recovered to 70% of the previous year. As subsequent profits continue to be released normally, cash flow is also expected to continue to improve. As of the end of last year, Meta had 40.8 billion in cash + securities, and after deducting 10 billion in interest-bearing debt, there was a net cash of 30 billion, indicating a good cash situation.

5. Comparison of Key Indicators with Expectations

Dolphin's Viewpoint

Dolphin's Viewpoint

After the disclosure of last quarter's financial report ("Fearless Meta, still gambling on the "metaverse" despite heavy losses"), Zuckerberg was "attacked" by investors due to the unexpected expenditure plan. In November, Meta announced a 13% staff reduction, and Zuckerberg also apologized publicly and promised to reduce spending, especially on metaverse investments, in a more rational way.

Meanwhile, Reels continued to rely on the two traffic giants Facebook and Instagram, further penetrating users and accelerating monetization, while TikTok's competitive threat to Meta seemed to have reached its peak, due to slower user growth, lower ROI, and geopolitical factors between countries.

The "open source + cost-saving" strategy has made the market increasingly optimistic about Meta's profitability turning for the better. Despite expectations of a turning point, institutions still have some doubts about Meta, and their performance outlook is relatively conservative, including their expectations for 2023, which are also more cautious than those of Dolphin Analyst.

However, if we look at third-party data and research information, the duration of Facebook and Instagram in the fourth quarter bottomed out and rebounded, and Reels has also clearly accelerated monetization by releasing more inventory.

Furthermore, if we consider the willingness of advertisers to invest, they will be more concerned about conversion rates under economic downturn. Therefore, under this macroeconomic pressure, Meta may have a chance to eat more of the market share of weaker small and medium-sized platforms, such as Snap, which has a high proportion of brand advertising, thanks to its advantage in high ROI for performance advertising and further releasing Reels' advertising inventory.

As we know, under the expectation of weakening European and American economies this year, the market will focus more on companies' profitability. Meta's real profit margin has already shown signs of recovery in the fourth quarter, and this time, Meta's attitude towards their outlook is "correct". The guidelines for total expenses and capital expenditures are both lower than the market's expectations.

We can say that Meta's Q4 report is a relatively satisfactory high-scoring answer. Although macroeconomic pressures still loom over every advertising company, the challenges faced by Meta have been more or less mitigated this year under the "open source and cost-saving + competition reduction" strategy. As of Wednesday's close, Meta's valuation is still not high, and after this financial report, the market's expectations will give more room for improvement. The additional $40 billion repurchase program can also provide more comfort and investment confidence to Meta shareholders in the short term.

This article is an original Dolphin research article and may not be reproduced without authorization. After the financial report interpretation, the content of the telephone conference call will be immediately available. Interested users can add the WeChat account "dolphinR123" to join the Dolphin research group and discuss investment views. The following is a detailed analysis of financial reports

1. Reels accelerating, unstoppable power of short videos

As a relatively pure advertising stock, the macro economy can be said to be Meta's biggest source of revenue. Since the second half of last year, sensitive advertisers have already started to take action, directly reflected in the decline in advertising companies' growth rate each quarter. Coupled with competition, Apple's privacy policy and other disturbances, Meta could no longer hold on as early as the second quarter, and revenue declined year-on-year.

Therefore, in the fourth quarter, when macro expectations were even worse, the market was even more conservative about Meta, even though the company revealed in the previous quarter that Reels' annual revenue had reached 1 billion US dollars and that it would continue to improve Facebook Reels' advertising features.

The market consensus for the fourth quarter was still close to the lower end of guidance, and it was believed that there would be an accelerated decline on a quarter-on-quarter basis. In actuality, the decline did not significantly widen, and there was still a 2% positive growth without exchange rate fluctuations.

Looking ahead to 2023, in the weak economic cycle where performance advertising is more advantageous, Dolphin Analyst is not so pessimistic about Meta and Reels will be expected to become an important revenue contribution this year.

1. In terms of the quantity and price of advertising, there is an obvious characteristic of economic growth gradually slowing down - the magnitude of the decrease in quantity increase is expanding. In 2023, under further global economic downturn, this trend will continue, and head platforms will take advantage of their own advantages to release more inventory at a lower price to attract small and medium-sized advertisers who originally hesitated because of "price." For Meta, after the proportion of Reels inventory with lower quotes is increased, this trend will become even more obvious.

2. Steady increase in traffic and increase in stickiness: In the fourth quarter, Facebook, which has more high-paying adult users, was the main source of growth, which is closely related to the company's tilt of resources to Facebook Reels. After Instagram's transformation to short videos was blocked (some users resisted), Meta increased the position of Reels on Facebook.

When short videos penetrate into middle-aged Facebook users with high purchasing power, it will naturally increase the frequency of single-person advertising display of the main site, thereby helping Meta attract more advertiser budgets during the shopping season.

{kind=link}

3. From the perspective of the advertising value of individual users: Reels has driven more mature markets in Europe and America. In addition to not being as bad as imagined in consumption, combined with the situation of Snap, Meta has obviously eaten part of the share of its peers.

4. Expectations for 1Q23: The company has set a target range of 26-28.5 billion, corresponding to a decline of 6.8% to growth of 2%, among which the negative impact of the exchange rate is still 2%. The market expectation falls on the median of the guidance. Although it did not exceed the guidance, according to the situation in the fourth quarter, the market is expected to be more positive about the outlook for the first quarter.

II. Competition slowdown? Crossing the short-term peak

When it comes to competition, TikTok cannot be ignored.

Before 2022, the direct competitive threat of TikTok to Meta was the grab for traffic, especially young users. Short video traffic has always been an advantage. In China, the product experience has been polished and matured for Douyin, which quickly killed all opponents after going abroad.

After 2022, TikTok officially began large-scale commercial monetization.

Although the scale of traffic is in the global TOP, the problem with TikTok now is slower growth in the second half of the year (reduced fresh traffic), younger user base (which implies low purchase conversion rates), and unavoidable international issues, and the call for banning TikTok has begun to spread among US government officials in the fourth quarter.

Therefore, based on the data from the third and fourth quarters of last year, Facebook and Instagram, which have added Reels function, have seen an increase in user time in the United States, while the traffic of TikTok, which is proud of its traffic, has come under pressure.

Dolphin Analyst believes that the possibility of completely banning TikTok in the United States is very low, but it is not ruled out that some special groups will be restricted from using it. Although the final scope of the ban may not be high, advertisers are currently more skeptical and inclined towards short-term cooperation. This would lead to overall quote of TikTok being uncompetitive, far lower than the traffic matching Meta and YouTube.

This is also part of the reason why TikTok's target of $12 billion in advertising revenue last year was difficult to achieve. In the short term, the ban is not only taking its toll, but the cost of penetrating middle-aged and elderly users is higher (competition is fierce, Meta and YouTube will fight to hold their fortresses), so TikTok's increase in advertising market share will be relatively slow. However, the current situation does not represent the long-term trend, and Dolphin Analyst still sees the operational capabilities of TikTok as strong under natural management. But for Meta, which experienced a dark 2022, it is already able to breathe.

3. The VR market is in its education period, and high-priced Pro models are not selling well.

In the fourth quarter, revenue from the VR business was RMB 730 million, a year-on-year decline of 17%, but higher than the market's expected RMB 650 million. Last year, there was a new version of the Quest 2 that increased the amount without increasing the price, and with strong consumer demand, the base was higher.

In October of this year, Meta launched the high-end VR headset Quest Pro, which is priced at $1,499. For the VR market still in its cultivation period, the potential number of users willing to try it out is small. Moreover, with no disruptive changes in actual experience, there is little motivation for users to upgrade.

According to the latest data from IDC, it is estimated that global VR headset shipments will reach 9.7 million units in 2022, a decrease of 1 million units from the forecast in October. Although Pico 4 was launched this year with great fanfare, the actual sales results fell short of expectations. The three factors of reduced home-based effects, lack of significant technological innovations, and insufficient content are likely to have contributed to the poor sales of VR headsets this year.

Oculus accounts for 84.6%, or an estimated 8.2 million units sold in 2022 compared to nearly no increase in 2021. IDC estimates that global shipments will grow by more than 30% next year. At the same time, during the third-quarter conference call, Zuckerberg also hinted that he hopes to launch a new product at a moderate price in the next 1-2 years, which may lead to a rebound next year.

But we also believe that the industry's explosion ultimately depends on a wide variety of content. If VR games are the benchmark for content, then in this year's macro environment and under the investment cycle of large-scale content, there are still difficulties in releasing content on a large scale, and it may not be until after next year that there will be a significant boost.

4. Slash Expenses, Slim Down, and Recover from the Slump Faster Than Expected

4. Slash Expenses, Slim Down, and Recover from the Slump Faster Than Expected

The excessive spending that plagued Meta's third-quarter report saw a clear improvement after the company announced massive layoffs in November. What's even more surprising is that the reduction in normal operating expenses and the outlook for 2023 spending both indicate that Meta's profit margin will see a significant improvement compared to 2022. This is the trend that the market hopes to see in the current environment.

1. Temporary decline in gross margin.

In the fourth quarter, the gross margin was 74.1%, influenced by Reels revenue, which has lower prices but splits with creators, and the short-term impact of layoffs, business restructuring, and investment in the new generation of data centers.

Dolphin Analyst believes that after removing the one-time impact, the gross margin level should be around 77%. Although it is lower than before, Reels revenue has the potential for high-speed expansion and can still increase the scale of profits.

2. Ongoing layoffs, with room for further operational efficiency improvement

In November, Meta announced to lay off 11,000 people, accounting for 13%. As of the end of last year, the total number of employees decreased by only 1,000 on a month-on-month basis. The layoff plan should still be in progress. Dolphin Analyst believes that the epidemic dividend made tech giants blindly optimistic about the future prospects, ignoring the macro environment in the short and medium term and the downward cycle.

During the three-year epidemic, Meta's staff grew by 60%. Although the number of layoffs in this round seems to be large, it accounts for only 40% of the net increase in staff during the three-year epidemic.

However, the operating profit during the same period has only increased by 20%, and the high input and high loss VR business actually belongs to venture capital projects. However, it accounts for a large proportion of the total expenditure of listed companies, which obviously harms the interests of shareholders. There is a huge difference between the return goals of investors in the secondary market and the shareholders in the primary market, and it is inevitably difficult to tolerate small Zha's squandering large amounts of money.

Fortunately, the Meta management team put on the brakes in time and admitted their mistakes. Especially after giving lower-than-expected spending guidelines, this serious and corrective attitude is expected to regain investors' trust. Compared with TikTok, which is still embroiled in international friction risks, Reels is still walking the old-fashioned path of imitation, but with a basic support of 3.7 billion social communication base, it is likely to fare better than Tiktok, which is constantly targeted by the U.S. government in the short term. Dolphin Investment Research "Meta" Historical Articles:

Financial Report Season

October 27, 2022 Conference Call: "Despite being questioned and 'besieged,' Xiaozha still insists on betting on the Metaverse (Meta 3Q22 conference call minutes)"

October 27, 2022 Financial Report Review: "Headstrong Meta - still gambling on 'Metaverse' despite severe bleeding"

July 28, 2022 Conference Call: "Macro, Apple ATT, competition and headwinds - the management's short-term outlook is still conservative (Meta conference call)"

July 28, 2022 Financial Report Review: "No Google-like reversal in sight, Meta's sluggishness is hard to conceal"

April 28, 2022 Conference Call: "Not in a hurry to commercialize Reels in response to competition (Meta conference call minutes)"

April 28, 2022 Financial Report Review: "Is the explosive growth due to faith? The turning point for Meta has not yet arrived."

February 3, 2022 Conference Call: "Can we expect Reels to activate Meta user growth like Stories did 3 years ago? (Conference call minutes)"

February 3, 2022 Financial Report Review: "Adding Thunder to the Thunder - Facebook turns into a 'God of Misfortune' after changing its name to Meta."

October 26, 2021 Conference Call: "Facebook conference call keywords: Metaverse, Apple's privacy policy, young people, competition"

October 26, 2021 Financial Report Review: "Facebook: Not afraid of 'thunderous' expectations, betting heavily on 'Metaverse'" 2021 July 29 Telephone Conference Call "Facebook: Metaverse will become the next chapter of the company [Conference Call Summary]" (https://longbridgeapp.com/news/41516471) 2021 July 29 Financial Report Review "The energy of Facebook may exceed your imagination|Longbridge Investment Research" (https://longbridgeapp.com/news/41513711) 2021 April 29 Telephone Conference "Facebook first-quarter performance call summary" (https://longbridgeapp.com/topics/781219?invite-code=032064) 2021 April 29 Financial Report Review "Facebook: Guidelines have always been low-key, and performance has continued to explode" (https://longbridgeapp.com/news/34576269) 2021 April 28 Financial Report Preview "Facebook performance preview: Can there be any surprises after being expected by the market?" (https://longbridgeapp.com/topics/777901?invite-code=032064)

In-Depth

2022 July 1 "TikTok wants to teach the "big brothers" to work, Google and Meta want to change" (https://longbridgeapp.com/topics/3016272?invite-code=032064) February 17, 2022 "Internet Advertising Summary-Meta: Low combat power is the original sin" (https://longbridgeapp.com/topics/1924950) September 24, 2021 "Apple draws a knife, is Facebook the first giant to "shed blood"?" (https://longbridgeapp.com/topics/1165524?invite-code=032064) August 6, 2021 "Facebook: Digging Deep into the "Business Value" of the World's Number One Internet Users Harvesting Machine" (https://longbridgeapp.com/topics/1012966?invite-code=032064) November 23, 2021 "Facebook: Turning around "Meta" at a high price, the turning point is not far away after the double pressure" (https://longbridgeapp.com/topics/1360670?invite-code=032064)

Disclosure and Statement of Risks in This Article: [Dolphin Investment Research Disclaimer and General Disclosures] (https://support.longbridge.global/topics/misc/dolphin-disclaimer)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.