🔥 In the list of "Biggest AI Winners," half are no longer cheap—the real opportunity might not be where you first look.

The market is now telling a very simple story:

"Whoever grows the fastest, should rise the most."

But my own judgment is exactly the opposite—

The fastest growers are often the ones whose expectations are most easily overdrawn.

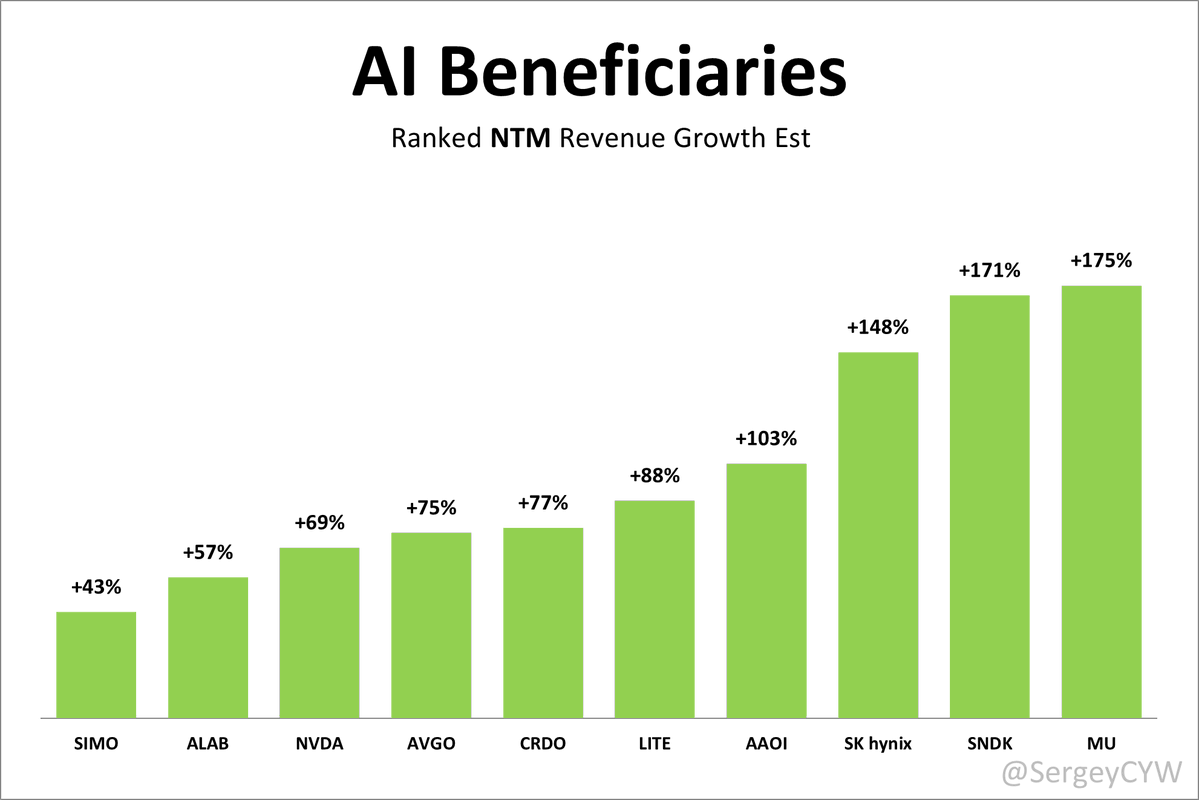

First, let's break down this list; it can actually be divided into three layers of logic:

First Layer: The core leaders already "priced in" by the market.

$NVIDIA(NVDA.US)

$Broadcom(AVGO.US)

The characteristics of this layer:

Clearest logic

Most concentrated capital

Most consistent narrative

The problems are also most obvious:

The market already knows they will grow.

So the question isn't "Will they grow?" but:

Can they still exceed expectations?

Second Layer: The "high-flexibility segments" within AI infrastructure.

$Micron Tech(MU.US)

$Sandisk(SNDK.US)

$SKH

The essence of this layer:

Storage = The "supporting bottleneck" of AI computing power.

Current growth comes from:

HBM

Data center demand

Expansion of AI training scale

But there's a risk I've been watching closely here:

This is a strongly cyclical industry.

Once supply starts to catch up,

profit expansion might not continue linearly.

Third Layer: The most easily overlooked, but most volatile chain.

$Applied Optoelectronics(AAOI.US)

$Lumentum(LITE.US)

$Credo Tech(CRDO.US)

$Astera Labs(ALAB.US)

$Silicon Motion Tech(SIMO.US)

This layer is what I think is most worth breaking down:

They aren't "telling an AI story,"

but are "stuck in a key position within the AI chain."

Examples:

Optical modules

High-speed connectivity

Data transmission

These things won't appear in the headlines,

but determine whether the system can run.

The problem is:

Many companies here have already had their "perfect execution" traded ahead by the market.

So my current thinking is very clear:

Not to chase the "growth rate ranking,"

but to look for two things:

1) Whether expectations have been fully priced in.

2) Whether there is a "second-stage narrative."

For example:

$NVIDIA(NVDA.US)'s first stage was GPUs.

The second stage is the entire platform (CUDA + AI ecosystem).

Yet many companies are still stuck in the first stage.

The real opportunity often appears when:

The market hasn't yet started telling the "second-layer logic."

There's an even more realistic problem:

In this list, how many companies are such that:

Growth can materialize,

but the stock price has already priced in two years ahead?

What I care more about now isn't "who grows the fastest,"

but:

If growth only meets expectations, rather than exceeding them,

who will get their valuation cut first?

Which type are you more inclined towards?

Continue betting on the certainty of the leaders,

or gamble on those "second-layer opportunities" that the market hasn't fully articulated yet?

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.