TSLA 1Q26 First Take: Headline-strong print, with revenue, GPM, and net income beating consensus by a wide margin.

However, multiple one-off factors contributed to the beat.Even after stripping them out, the core auto biz still outperformed the Street’s low bar.

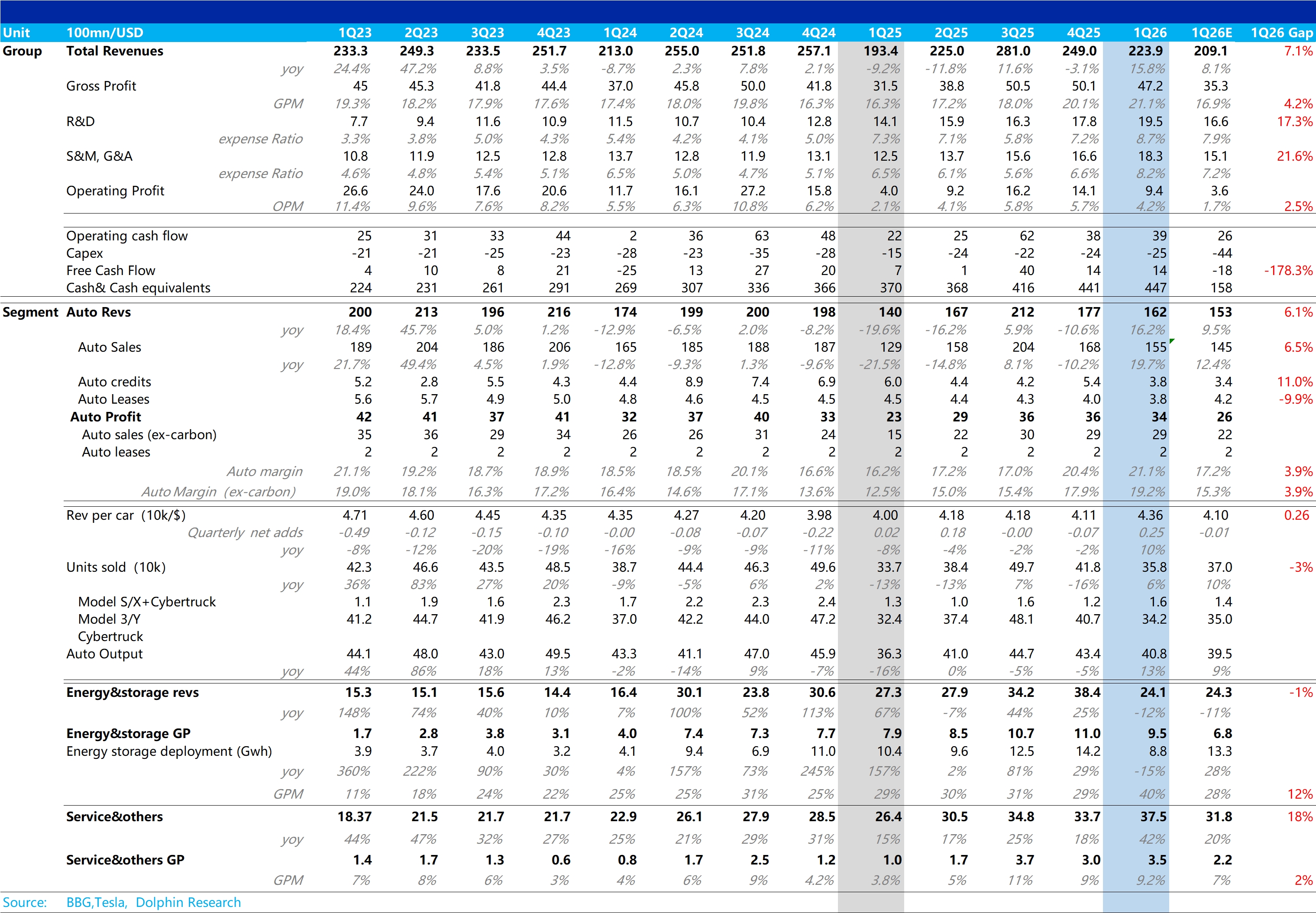

① Revenue: Beat ex-FX, driven by higher ASPs

Q1 revenue was $22.4bn (+16% YoY), well ahead of the $20.7–20.9bn consensus.There was an estimated ~$0.9bn positive FX impact; ex-FX, adj. revenue was $21.5bn, still above expectations.

The outperformance was mainly driven by an auto ASP rebound QoQ after several quarters of declines.Services & other revenue also grew 42% YoY.

② Margin: Headline print flattered by multiple one-offs

GPM was 21.1%, well above the 16.9% consensus, led by upside in auto and energy storage.Below the line, autos booked a ~$230mn warranty reserve reversal and storage recognized ~$250mn in tariff subsidies, with an additional ~$200mn FX gain.

Ex these items, underlying GPM was 18.7%.That is down 140bps vs. last quarter’s 20.1% peak but still above consensus.

Core auto GPM ex-regulatory credits printed at 19.2% vs. 15.3% expected.Ex one-offs, underlying core auto margin was ~17.5%, slightly below last quarter’s 17.9% yet meaningfully above expectations.

Dolphin Research believes a QoQ ASP uptick and higher recognition of high-margin FSD were key supports.These offset higher per-unit depreciation from lower volumes and rising upstream raw material costs.

③ Cash flow: Growth covered spend; FCF turned positive

Despite elevated AI spend (in-house AI chips, Optimus, FSD) and higher SBC pushing up S&M and R&D QoQ, top-line and margin beats, coupled with no spike in capex, drove Q1 FCF to +$1.4bn.This net inflow was far better than the expected outflow.

That said, autos are increasingly a cash-flow support rather than the core narrative.The market’s real focus is whether AI milestones are slipping and whether cash flows are sustainable amid heavy investment.

① Optimus: The V3 debut shifted from the prior 1Q timeline to mid-2026.Elon Musk said small-batch production could start in late Jul or Aug in Fremont, but the ramp will be slow, with meaningful volumes only next year.

② Robotaxi: The company remains cautious on launching unsupervised Robotaxi service.It has expanded to Dallas and Houston and aims to operate in ~10 states by year-end, but Musk noted this year’s related revenue will not be ‘super meaningful’.He expects it to become meaningful and significant next year.

③ FSD: Unsupervised features are expected to begin rolling out to the customer fleet in Q4 2026.Deployment will proceed only where specific geographies are deemed demonstrably safe.

Capex and cash flow pressure:

The 2026 capex guide was raised from ‘over $20bn’ to ‘over $25bn’, to support six new facilities (incl. lithium refining, Cybercab, Optimus) and AI compute infrastructure.

While cash and investments remain ample at >$44bn, at a >$25bn/yr capex run-rate current cash covers less than two years of high-intensity spend.The ambitious AI roadmap must translate into tangible revenue and cash flow soon, or the company could face financing pressure. $Tesla(TSLA.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.