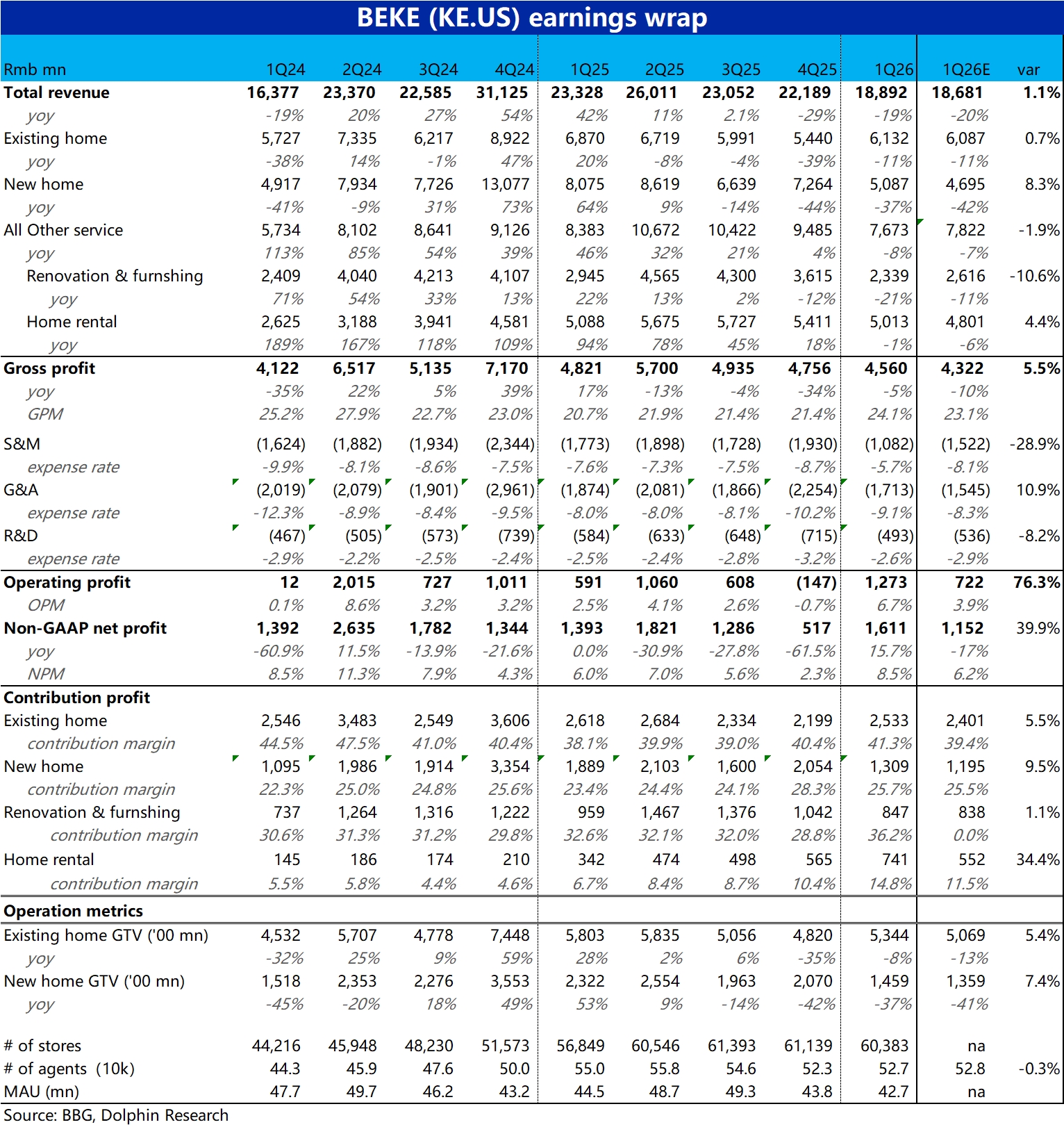

BEKE 1Q26 First Take: Overall, the quarter screened as a solid beat vs. expectations. Despite most segments posting YoY revenue declines on a high base, profit inflected as the company streamlined headcount, lifted productivity, and tightened opex, with Adj. net profit up nearly 16% YoY and well ahead of the Street.

In detail:

1) Track 1 brokerage remains under pressure. GTV and revenue were both down YoY, with existing-home transactions proving resilient at a low-teens decline, while new-home fell 40%+ YoY.

2) In Track 2, home improvement revenue fell Approx. 21% YoY on macro headwinds and a strategic refocus, notably worse than the Street’s -11% view. Leasing revenue dipped 1% YoY, mainly due to a recognition change for the high-touch 'Steward Rental' model from gross to net; underlying volume likely still grew Approx. 20–30%.

3) While macro headwinds persist, margins improved across business lines. In Track 1 brokerage, segment margins expanded by 200–300bps YoY, slightly above expectations, driven by headcount rationalization and a modest reduction in agent commission splits.

Margins in Track 2 exceeded expectations by a wider margin. Home improvement, despite smaller scale, delivered a 36% margin after materially optimizing the upstream supply chain and cutting customer acquisition spend. Leasing benefited from rapid growth in higher-margin 'Steward Rental,' lifting segment margin from 10.4% in the prior quarter to nearly 15%.

4) Cost discipline also contributed meaningfully. Total opex fell Approx. 22% YoY vs. total revenue down 19% YoY, led by a sharp 39% cut in marketing spend, which came in just over RMB 1bn vs. the Street’s ~RMB 1.5bn.

5) Overall, margin expansion did more of the heavy lifting, beating by Approx. RMB 240mn, while opex undershot by Approx. RMB 160mn. As a result, Adj. profit was Approx. RMB 1.6bn, nearly RMB 500mn above the Street. $KE(BEKE.US) $BEKE-W(02423.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.