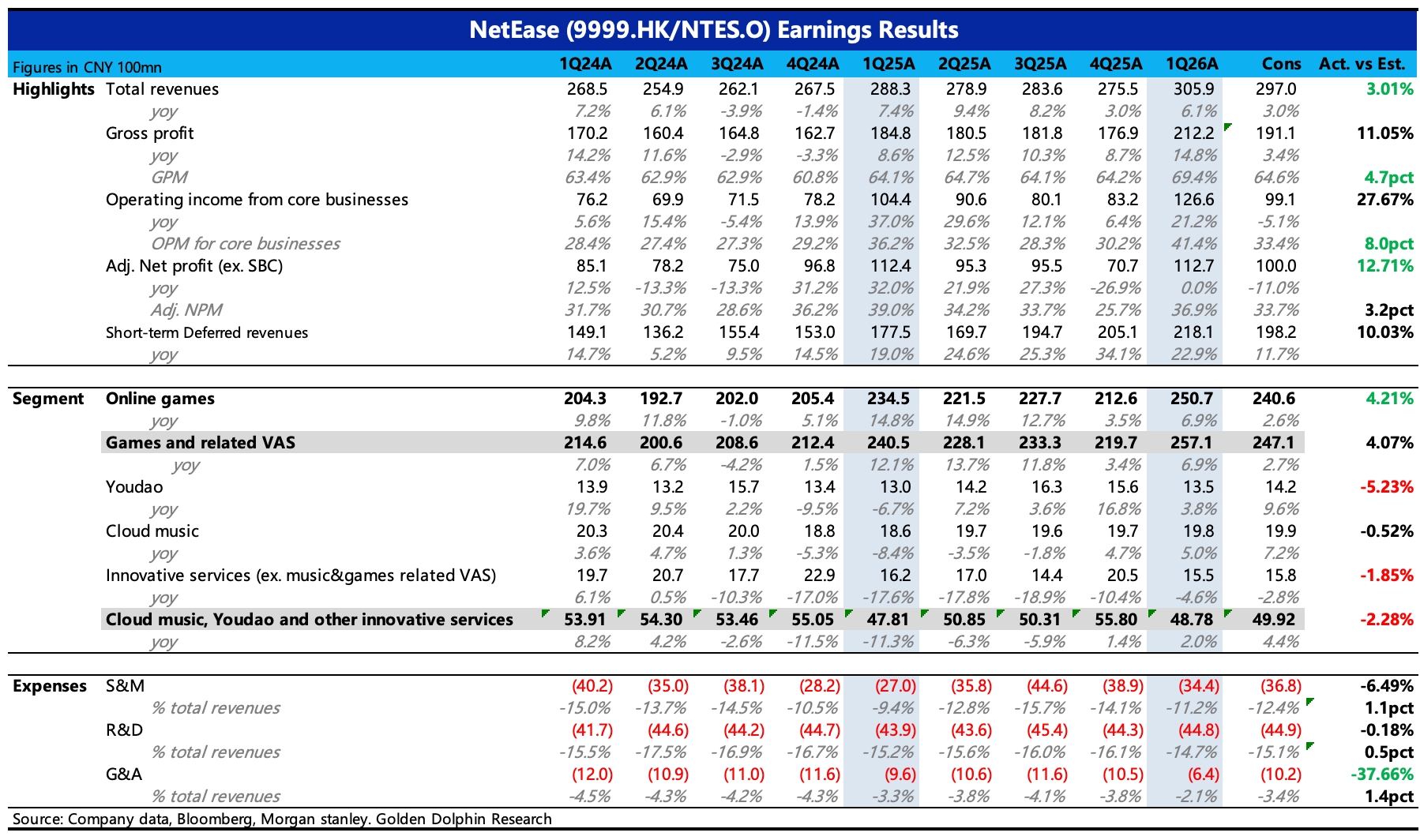

NetEase 1Q26 First Take. Q1 results beat, with upside vs. Street driven by game revenue, GPM, and tight opex control.

(1) Game revenue beat. The market had expected sub-5% growth given no new launches this quarter and a tough base last year, but NetEase delivered 7% growth. Drivers included the 'Fantasy Westward Journey' PC 'Changyou' servers, the overseas rollout of 'Where Winds Meet', and operational recovery in 'Identity V' and 'Eggy Party'.

Deferred revenue at Q1-end rose 22% YoY, topping the 17% widely modeled by the Street. By Dolphin Research estimates, gross billings grew 18% QoQ; while short of last year's exceptional Q1 surge, it outperformed typical seasonal patterns.

Q2 will still face a high base. From H2, the mobile pipeline adds heavyweight launches, with '遗忘之海' in Q3 (Sell-side est. full-year all-platform billings of RMB 3–5bn) and '无限大' in late Q4 or early next year (Sell-side est. RMB 10bn), which should support sequential acceleration in game revenue.

(2) GPM expanded sharply, the quarter's biggest highlight in our view. Q1 GPM reached 69.4%, up over 500bps YoY and QoQ, driven by games and live streaming. Game-related GPM rose to 75%, up 600bps YoY.

Key drivers included a higher mix from self-developed, high-margin PC titles this quarter and lower channel fees, aided by steering users to top up on the official website and lower rev-share rates at app stores like Apple. This aligns with the margin expansion logic the market has been anticipating.

(3) Personnel expense optimization. Opex was tightly managed in Q1, with R&D growing slowly, and S&M down QoQ on normal seasonality. G&A fell 33% YoY.

G&A has been shrinking for two years; from an already lean base, the further step-down suggests meaningful headcount optimization or comp adjustments in Q1. SBC tells a similar story: despite NetEase's share price being up ~10% YoY, SBC expense nearly halved YoY.

News also surfaced at quarter-end of significant cuts to outsourced teams. These savings likely were not fully reflected in Q1, and details warrant attention on the call.

(4) Buybacks up; overall shareholder returns are modest. The quarter's declared dividend is $0.144 per share ($0.72 per ADS), totaling $460mn, a 30% payout, roughly stable. NetEase repurchased $127mn in Q1, already above the total for last year; management typically paces buybacks with market cap swings, and $2.9bn remains authorized (three-year term).

Annualizing Q1 dividends plus buybacks implies ~$2.35bn in full-year shareholder returns, about 3%–4% of the $74bn market cap as of yesterday's close, which is not high. $NTES(09999.HK) $NetEase(NTES.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.