Goldman Sachs: Samsung Electronics

Unprecedented profit margins: Driven by strong quarterly price increases (traditional DRAM +47% QoQ; NAND +66% QoQ),

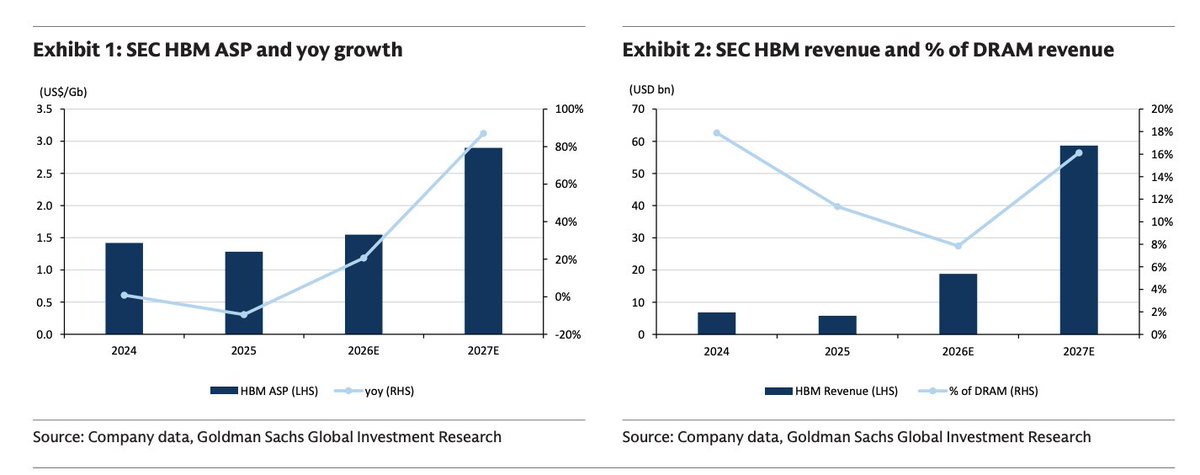

HBM progress: The smooth ramp-up of HBM4 mass production has significantly boosted performance. Samsung recently became the world's first company to achieve over $1 billion in HBM4 revenue. Goldman Sachs raised its 2027 HBM pricing forecast, expecting prices to achieve nearly 90% year-on-year growth next year.

Price stability: Long-term agreements signed with buyers are expected to protect future profit margins and pricing at high levels.

The capacity utilization of advanced processes remains good, mainly due to manufacturing Exynos processors for the upcoming Galaxy S26 and producing 4nm base chips for HBM4. However, back-end inventory stocking means the actual reported losses are slightly higher than the target.

The smartphone division is estimated to have recorded its first-ever operating loss. Soaring component costs—particularly rising memory chip prices—have severely squeezed mobile product margins. Goldman Sachs expects this margin erosion to persist as memory prices continue to rise for the remainder of the year.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.