退到 “墙角” 的 “私募大佬们”

净值无力,何时打响反击

当市场的狂欢席卷而来,一批曾经的 “投资王者” 们却在寂静中默默的退到舞台一角。

他们的净值曲线与沸腾的市场背道而驰,仿佛置身于另一个平行时空。

他们的观点依然被人关注,但渐渐似乎成为了市场 “diss” 的对象。

那些昂扬的名字,曾经被资金追逐的产品,现在渐渐落到了百亿私募的业绩榜单末端。而且是在过去三年里,一而再,再而三的落到末端。

这不仅出乎投资者的预料,也当然激发了很多怀疑的声音。

曾经封神的投资大佬们,那些在 2021 年前闪闪发光的大佬们,已经被市场大潮卷向墙角。

如此 “坚守” 的他们,还能重现往日的荣光吗?

你们怎么了?大佬

1999 年 12 月,上个世纪最疯狂的网络股行情登峰造极的档口,《巴伦周刊》曾经刊发一篇名为《你怎么了,沃伦(巴菲特)》的封面文章,讨论巴菲特在过去一年多的时间里的业绩落后。

在那个网络股为主流的行情中,坚守自己股票风格的一批投资家都在 “走背字”,其中就包括巴菲特、老虎基金罗伯逊和量子基金的朱肯米勒(翻多前)。

类似的情况也发生在国内的部分投资大佬身上,比如林园,比如但斌。

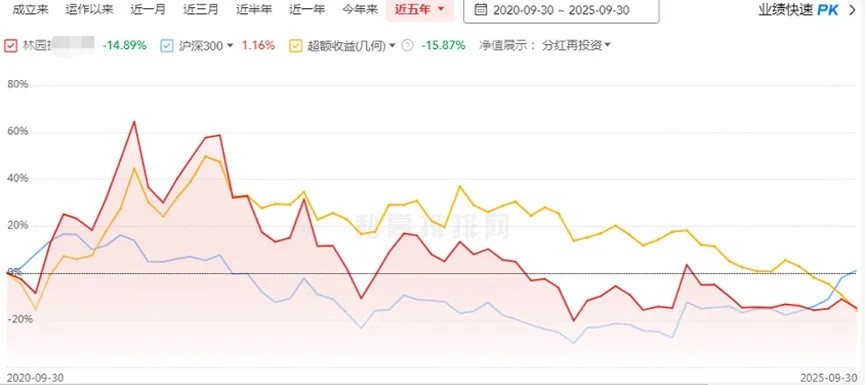

翻看近一年的百亿私募表现排序,林园投资的多只产品居于末尾,市场的狂欢与这家知名机构似乎无关。

据第三方数据披露平台,以截至 2025 年 9 月 30 日,过去一年沪深 300 指数上涨了 15.50%。而林园投资 XX 号的净值,是两位数的回撤。

这一正一负之间,距离被拉开超过 30 个百分点。

完美错过?

从净值走势看,林园的部分产品几乎 “完美” 错过了近一年的行情。尤其是今年二季度后,当热门股尽力演绎行情的同时,林园产品的净值反而走向了相反的方向。

这不是林园一个人的 “烦恼”。

回看 50 亿以上的主动权益私募机构,大致在过去一年里走向了两个方向。

要么,主动、被动的跟上市场的行情——擅长消费股投资的跟上新消费,爱搞周期股的 “信” 了科技大周期,爱上了机器人、AI、半导体。

要么,坚守以往的品种和投资思路——但面临许多的压力。

而林园们无疑是选择了后者。

重仓 “老消费”?

当当主力资金追逐 AI、半导体、新能源时,林园的产品却依然重仓着他那几张 “老牌” 消费股,对新兴科技领域几乎 “视而不见”。

这可以被认为是一种坚守,也可以被看做是一种执念。

据销售渠道的量化分析报告,对林园产品净值产生 “负贡献” 的行业,恰恰是食品饮料、医药生物、商贸零售等传统板块,他的重仓股却像 “钉” 在了林园所熟悉的传统领域。

其中,林园重仓的食品饮料公司 “尤甚”,成为对净值拖累最为明显的持仓方向。

另据渠道分析显示,尽管林园在公用事业、电子、钢铁和银行等板块的持仓对净值产生了正向贡献,但这些行业带来的全部收益加总,仍不足以弥补其在食品饮料单一行业上所遭受的损失。

“执念” 何来

但林园这么做,自然有他的逻辑。

纵观林园今年的公开言论,我们可以梳理出其坚守 “老牌” 的内在逻辑:

其一,他多次强调 “长期重仓,买了不卖,永远不卖” 的投资理念。

这意味着其投资框架建立在 “终身持有” 的底层逻辑上,对持仓标的的选择标准极为严苛,但同时也可能忽视了行业景气度的周期性变化。

其二,他明确表示看好中医中药等 “老年人经济” 的赛道,预测其未来十年符合增长率接近双位数以上。

这意味着在医药生物板块的配置,是基于对特定细分领域长期成长性的判断,但这种判断正面临市场现实的严峻考验。

其三,他信心十足地指出白酒板块依然低估,认为 “数千年来的中国酒文化不会消失,因为酒是能给人带来快乐的事情”。

这意味着对食品饮料的坚守,已经超越财务分析层面,上升到文化自信与人性需求的维度。

其四,他特别提及 A 股股息率优势,认为资金将持续流入食品饮料(他称之为 “嘴巴生意”)、公用事业等稳定股息率的行业。

这意味着其配置思路偏向高股息、稳定现金流资产,与当前市场追逐成长性的偏好形成鲜明对比。

其五,林园还在年内提及对科技股投资 “没有把握”,难以预测未来的龙头公司,“不是我不想投,而是这个钱我赚不到”。

这个想法其实非常好理解,市场行情风格终究会切换,就如同银行股也会连续走强两年一样。

这个时候改弦更张,如果行情风格发生切换,就面临更大的考验。

两难抉择

但同时,这样的选择也会导致非常大的压力。

尤其是,单一市场风格如果一直不切换的话,那么坚守的基金经理 “境遇” 会越来越有问题——直到被逼入死角。

上个世纪互联网股热潮中,美股市场就带来过一个 “切肤” 的案例,一个是老虎基金的罗伯逊,他在互联网泡沫前几个月 “清盘” 了自己的对冲基金——曾经市场规模最大的对冲基金之一。

但就在他完成清盘动作的当月,美股的风格真的切换了。

所以,这就是个两难问题。

除了两难抉择外,风格或许也是一个问题。

林园与许多第一代成功的基金经理一样,其投资体系的基石早在多年前就已奠定。他们凭借对 1990 年代-2000 年代中国经济结构变化的感知,早年重仓大消费为代表的传统赛道,在时代的浪潮中赚得了惊人的回报。

正是这份源于成功经验的 “信仰”,铸就了林园今日的 “执念” 底色:一方面,是对自身 “买入并持有” 投资体系的极度自信;另一方面,则是对市场喧嚣热闹的新兴赛道的本能性疏离。

这种疏离,在结构性行情愈演愈烈的当下,持续面临着严峻的考验。

某种程度上,林园的产品目前像是在旧航线上行驶的船只,当各路新人、老将在新航线上载歌载舞时,坚守旧航线的人还被风浪越推越远。

同行的 “注脚”

另据私募排排网的梳理,在百亿私募产品的 “倒序” 排名中(近一年),另一位 “大人物” 的紧贴着林园多只产品。

即东方港湾的但斌,这位百亿基金经理近两年可谓风光无限,不仅在去年拿下百亿私募冠军,更成为了中国内地 AI 投资的 “死多头”。

然而,但斌操盘的产品却有着分化,他打榜的产品近一年收益超过 25 个百分点,却名下另有产品收益同期仅有 12%,后者显著落后于沪深 300 指数。

但斌落后的产品,让投资者感觉到:重仓美股 AI 板块的力度 “轻” 了。

以私募行业的常识来看,一位基金经理不会将所有产品重仓于风险最高、潜在收益最高的赛道,要结合产品资金来源、客户风险承受度、合作渠道合规性的要求。

如此一看,但斌表现逊色的产品——在近一年与林园多只产品共同居于尾部——或许是但斌 A 股组合的 “样本”,或许也是其 “传统思维” 的展现。

毕竟,林园和但斌均因早年投资白酒而赚得盆满钵满。

2000 年的巴菲特,在熬过了 “全民 diss” 的时刻后,终于等到了风格的切换。但资金不允许的罗伯逊则收下了 “个人性格” 的 “苦酒”。这一次,大佬们的坚持会走向何方?