颠覆认知!德银:非经济衰退下快速降息后,往往更可能迎来重新加息

Deutsche Bank warns that the current pace of interest rate cuts by the Federal Reserve is extremely rare during non-recession periods. Historically, while such policies have supported the market in the short term, they can easily lead to economic overheating and a rebound in inflation, ultimately forcing central banks to "hit the brakes" and raise interest rates again. International markets such as the Eurozone and Canada have shifted their expectations towards interest rate hikes, indicating that the U.S. may follow suit

Deutsche Bank issued a warning to the market in its report on the 9th, stating that although investors generally bet that the Federal Reserve will maintain an accommodative stance, the next move by the Federal Reserve in 2026 is very likely to be an interest rate hike rather than a cut. This potential policy turnaround contradicts the current mainstream consensus.

Jim Reid, Head of Global Macro and Thematic Research at Deutsche Bank, pointed out that the direction of international markets has undergone a dramatic reversal in the past few weeks, with market pricing in the Eurozone, Australia, New Zealand, Canada, and Japan all indicating that an interest rate hike is the next step. Especially in Canada and Australia, just two weeks ago, the market believed that the likelihood of a rate cut next year was greater, and this rapid reversal of expectations demonstrates the extreme instability of the current macro environment.

If the U.S. market follows this international trend, the pricing logic of risk assets and the outlook for next year will be completely overturned. Deutsche Bank strategists emphasized that the current market is experiencing the fastest interest rate cut cycle in decades without an economic recession, and historical data shows that such scenarios often lead to economic re-acceleration, which in turn forces central banks back onto the path of rate hikes, and in some cases, this ultimately leads to economic recession.

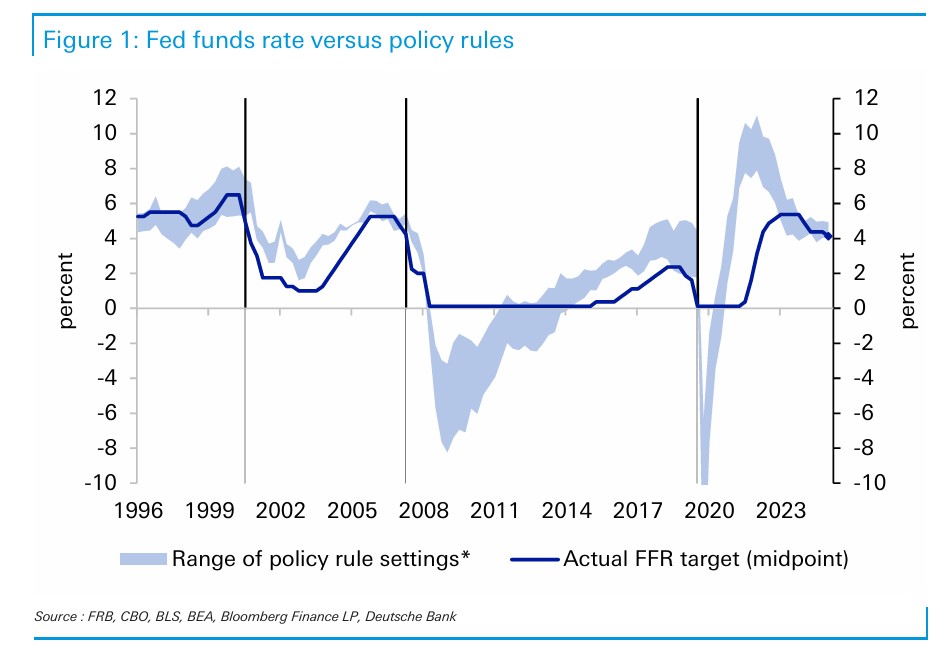

Although the market widely expects the Federal Reserve to announce another 25 basis point rate cut tomorrow, and the S&P 500 index has recently not only reached a new high but is also projected by Deutsche Bank strategists to rise to 8000 points, the bank warns that this optimistic outlook is highly dependent on the Federal Reserve maintaining an accommodative stance. Given that traditional policy rules indicate that interest rates are already at the lower bound of a reasonable range, and considering the dual pressures of fiscal stimulus and inflation stickiness next year, the threshold for a fundamental shift in policy narrative may not be high.

The Domino Effect of Global Tightening Expectations

According to Deutsche Bank, the interest rate expectations of major global economies are undergoing a significant reassessment. In addition to Japan, which is expected to raise rates next week, the pricing mechanisms in the Eurozone and several major developed markets indicate that rate hikes are becoming the new direction of least resistance. The sharp reversal in market expectations in Canada and Australia within just two weeks serves as a forward-looking warning for the U.S. market.

Domestically in the U.S., market trading around Federal Reserve policy has also greatly intensified volatility. The report noted that the day after the S&P 500 index hit a historic high, Federal Reserve Chairman Powell stated that a rate cut in December was not a foregone conclusion, leading to a significant hawkish reaction in the market; subsequently, New York Fed President Williams made dovish comments, and the market then recalibrated its rate cut expectations. This heightened sensitivity to the statements of central bank officials highlights the current market's fragility regarding expectations of the policy path.

For next year's outlook, Deutsche Bank cautions investors not to underestimate the impact of rate hike risks. Looking back at major cross-asset sell-offs in recent years (such as in 2015-16, 2018, and 2022), they all coincided with the Federal Reserve's rate hike cycles. Analysts specifically pointed out in the report that the current pace of interest rate cuts is extremely rare during non-recession periods. Historically, this type of policy is often a double-edged sword: while it supports the market in the short term, it can easily trigger economic overheating and a rebound in inflation, ultimately forcing central banks to "hit the brakes" and raise interest rates again. Currently, central banks around the world are treading carefully, trying to find a balance between maintaining growth and controlling inflation, but this also means that the risk of policy missteps or abrupt turns has significantly increased.

Fiscal Shock and Inflation Pressure

Another major factor supporting the Federal Reserve's potential shift to a hawkish stance comes from the fundamentals. Analysis by Deutsche Bank's U.S. economists shows that, based on traditional policy models such as the Taylor rule, the current federal funds rate is already at the lower end of the "correct level."

This means that the room for further rate cuts is not only limited but may also encounter resistance in the future. Analysts pointed out that the U.S. economy will face a fiscal impulse from the "Big Beautiful" plan next year, while inflation is expected to remain above target levels. This combination of fiscal expansion and sticky inflation could easily alter the current policy narrative, making further rate hikes a reality that must be considered by 2026.

In this macro context, the optimistic expectations for the stock market are being tested. Deutsche Bank's equity strategists previously set a target of 8,000 points for the S&P 500 index in 2026, which implies an annual increase of about 15-20%, consistent with the median level of historical distribution. However, the report clearly states that the realization of this increase hinges on the Federal Reserve's ability to maintain its accommodative preference.

If the Federal Reserve does not continue to cut rates as the market expects, but instead is forced to raise rates due to economic data, this "negative curveball" will directly impact the valuation models of risk assets. Given the dramatic changes that have occurred in international markets over the past few weeks, Deutsche Bank advises investors not to rule out the possibility of the Federal Reserve restarting rate hikes in 2026.