有色商品周期如何投射在 A 股?

This round of commodity market trends is different from the previous four bull markets, with a divergence between energy and non-ferrous metal trends. Changcheng Securities' research report points out that the performance of non-ferrous metal stocks is influenced by the A-share market environment, with industrial metal stocks showing greater upward elasticity than commodity prices during bull markets, while precious metal stocks are highly correlated with commodity prices. The report reviews the commodity bull markets since 2004, emphasizing the synchronous relationship between commodity prices and PPI, and that industrial metals are more deeply affected by the A-shares

This round of commodity market trends shows significant differences compared to previous situations, with energy and non-ferrous metals exhibiting a divergent trend.

The strategy team at Great Wall Securities (Wang Yi, Wang Zhengjie) released the latest research report on January 22, indicating that the commodity market after 2022 is fundamentally different from the previous four bull markets, with energy and non-ferrous metals showing a "fork" in their trends.

Great Wall Securities pointed out that the performance of non-ferrous metal stocks depends not only on commodity price trends but is also profoundly influenced by the overall market environment and style shifts in the A-share market. Industrial metal stocks demonstrate a much greater upward elasticity than commodity prices during bull markets, while precious metal stocks are highly correlated with commodity prices, showing a relatively independent market trend.

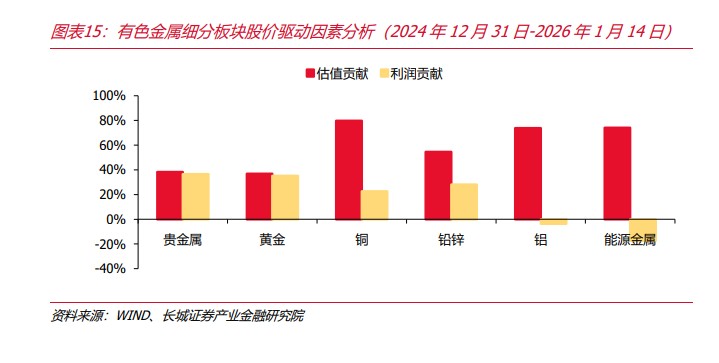

The report summarizes: the more it leans towards the "long-term logic" sectors (copper, aluminum, energy metals), the greater the valuation contribution; the more it leans towards "current profitability" precious metals, the more synchronized the commodity and stock price trends.

New Pattern After Four Rounds of Commodity Bull Markets

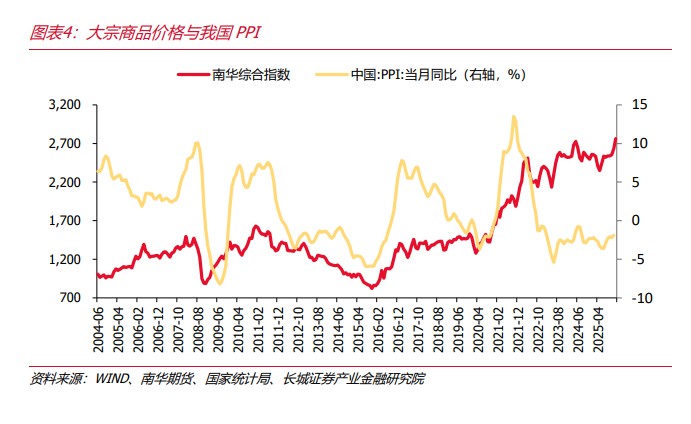

The report reviews four typical commodity bull markets since 2004: the global demand expansion period (2004-2008), the liquidity easing period (2009-2011), the supply-side reform period (2016), and the pandemic recovery period (2020-2022). During these cycles, the commodity index generally rose, with precious metals and energy leading the way for industrial products.

After 2022, the commodity market shows significant differentiation: energy and black metals have stabilized and declined after severe fluctuations, while non-ferrous metals, especially precious metals, have risen strongly.

Weak global economic recovery, geopolitical conflicts, and green transformation have jointly shaped this "fork" trend. The report emphasizes that previous commodity bull markets are highly synchronized with PPI, and commodity prices usually slightly lead PPI in bottoming and rebounding.

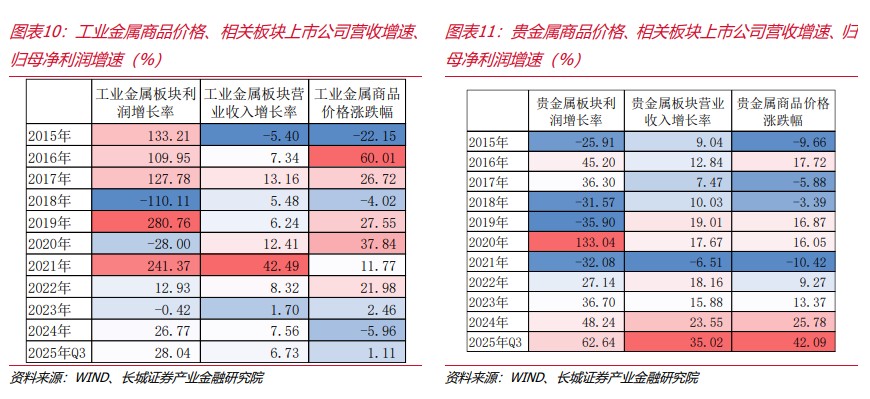

Industrial Metals More Affected by A-share Market

The research report focuses on analyzing the transmission mechanism between non-ferrous commodity prices and stock sectors. Commodity prices lead the initiation of stock sectors, but the lag and elasticity of industrial metal stocks are more influenced by the overall performance of the A-share market. In the 2006-2007, 2014-2015, and 2024 "924" market periods, industrial metal stocks significantly outperformed commodity prices; whereas during the 2019-2021 A-share growth style dominance period, the elasticity of industrial metal stocks was weaker than that of commodities.

Precious metals, on the other hand, exhibit stronger independence. The report points out that since 2018, the gold sector has shown a relatively independent market trend, with a high correlation between commodity prices and stock prices (correlation coefficient 0.5-0.9), while the correlation for industrial metals is only 0.2-0.3.

Valuation Elasticity Exceeds Commodity Price Elasticity

Data from early 2025 to the present reveals a new market characteristic: the valuation elasticity of the A-share non-ferrous metal sub-sector is significantly greater than the commodity price elasticity. The price increases of copper, aluminum, and energy metal stocks have clearly outpaced their corresponding futures indices, while precious metals "follow but do not amplify."

Research report summary: "The more a sector leans towards 'forward logic' (copper, aluminum, energy metals), the greater the valuation contribution; the more it leans towards 'current earnings' (precious metals), the more synchronized the commodity and stock price movements."

The implication for investors is that in the current market environment, the industrial metal sector reflects market risk appetite and industry trend expectations more than merely following commodity price fluctuations.

Risk Warning and Disclaimer

The market has risks, and investments should be made cautiously. This article does not constitute personal investment advice and does not take into account the specific investment objectives, financial situation, or needs of individual users. Users should consider whether any opinions, views, or conclusions in this article are suitable for their specific circumstances. Investment based on this is at one's own risk.