Disney: How to balance growth and profit?

Hi everyone, I'm Dolphin Analyst!

$ Disney.US released its Q2 2023 earnings report after the US stock market closed on May 10th.

This is the first complete financial quarter since legendary CEO Iger returned, so the market is very concerned about the reform effect promised by management last quarter to "increase profits" - "both at the group level and in segmented businesses, there have been varying degrees of improvement on the profit side, especially in the streaming business that has been a long-term drag on profits."

Unexpectedly, the number of streaming subscribers plummeted. In addition to the IPL copyright issue causing a further decline in the Indian market, the content pipeline for Disney+ in Q2 was not rich enough. Although the low-priced ad version was launched at the end of last year, the standard version that North American users prefer has seen a significant price increase, putting pressure on subscriber growth. Whether this strong profit protection strategy will affect the growth of streaming remains to be seen in the short term.

In addition, we also suggest paying attention to the theme park business. "The park business was still strong in Q2, but the popularity of local parks has visibly slowed down," and although demand for international parks is strong, the bulk of revenue still comes from local parks.

Due to concerns about the stagnation of streaming growth and the impact of macroeconomic downturns on cable TV advertising and park demand, Disney fell more than 4% after hours. In the long term, we are optimistic about the profit recovery space of Disney's business after the reform by the new management team and the value return of the century-old entertainment leader, but the short-term pressure on some businesses cannot be underestimated.

At present, the valuation is not high (24FY EV/EBITDA 10x, PE 20x), located in the neutral to lower range of historical valuations, but we should also pay attention to whether the top line will drag down the pace of EPS repair in the future. If the demand for risk return is relatively high, it is best to confirm the macro impact through one quarter's situation or wait for a more comfortable entry point.

How will the new management team help Disney get through the macroeconomic downturn and what is the performance guidance for the next two years? Pay attention to the earnings conference call. Dolphin Analyst will also share the meeting minutes on the Longbridge app and user group as soon as possible. If you are interested, you can contact the assistant (WeChat "dolphinR123") to obtain them.

Interpretation of this quarter's financial report

I. Understanding Disney

As a nearly century-old entertainment kingdom, Disney's business structure has undergone multiple adjustments. Dolphin Analyst has provided a detailed introduction in "Disney: The 'Facial Rejuvenation Technique' of a Hundred-Year-Old Princess." Here is the latest business structure for investors to read before reviewing the financial report.

Disney's business structure mainly includes four parts: film and television entertainment, cable television, streaming media, theme parks and merchandise retail.

The [theme park and merchandise retail] business has been relatively mature after years of development. With the support of the first IP reserve, Disney's theme park business has a leading position and is more affected by overall consumption. Under normal circumstances, it can be regarded as a stable cash flow.

[Film and television entertainment], [cable television], and [streaming media] are essentially producing and distributing Disney films, so changes in revenue are mainly related to Disney's film scheduling and overall film market consumption.

Source: Disney Financial Report, Dolphin Research and Analysis

2. Streaming media's loss reduction slightly exceeded expectations, and more profit improvement is expected

Iger's first major task upon his return was to improve the company's profitability, and the long-term loss-making streaming media business was the main target. Specific execution actions such as reducing content expenses and layoffs are all aimed at reducing costs and increasing efficiency.

The profit margins of each segmented business item in the second quarter have improved year-on-year or quarter-on-quarter, and the streaming media business has exceeded market expectations in reducing losses. The overall operating profit margin in Q2 was 15%, an increase of 2pct from the previous quarter's 12%, but still lower than last year's 19%.

After the significant reduction in losses in streaming media, the drag on overall profitability has also been significantly reduced. In addition, the profit margin of content sales is also being repaired season by season, but the current profit pillar is still the park and cable television.

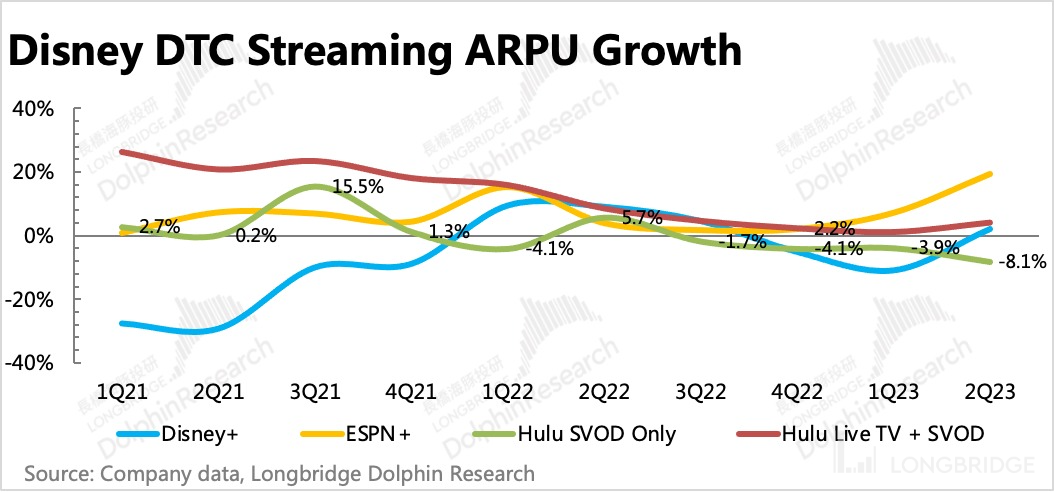

3. Disney+ unexpectedly lost users again

Although the streaming media business has reduced losses, the number of users has missed significantly, with a loss of 4 million users, while the market expected an increase of 1.34 million. In other words, 13% of the revenue growth of streaming media in the second quarter was basically due to the price increase in December (except for the ARPU of Hulu Live TV+SVOD, which decreased year-on-year, and other platforms increased).

!Diagram description and line chart description have been automatically generated

!Diagram description and line chart description have been automatically generated

{kind=link}

This is relatively consistent with Dolphin Analyst's judgment in the previous season's financial report review - "The new management may prioritize "profit" goals over "user expansion" and adjust its business strategy. Compared with last year, this year's Disney may use more content for external authorization to obtain income, digesting high production costs, rather than hiding in Disney+ exclusive to obtain more user payments."

The blame for unexpected user loss is mainly attributed to the Indian market, where the impact of IPL copyright continues to deepen. At the beginning of the year, Viacom18 announced that IPL matches will be broadcast for free, further causing a decline in demand for Disney+Hotstar subscriptions.

In addition, the North American region also saw a user loss for the first time due to insufficient content on Disney+ this quarter. However, there is no need to worry too much about Disney+'s content reserves in the second half of the year. In addition to newly produced series, Disney has many blockbuster movies this year, which will also be broadcast on Disney+ after being released in theaters. However, the problem in the Indian market is temporarily unsolvable.

4. Park performance is still strong, but can it continue in the short term?

In the second quarter, revenue from theme parks and consumer products increased by 17%, with park business growth rate of 23.5%. Although the growth rate slowed down compared to the previous quarter, it is still considered strong. Consumer product revenue has worsened compared to the previous quarter.

However, as we expressed our concerns in the previous season's financial report review, the growth rate of visitor volume to domestic parks in the United States has dropped to single digits of 7% (compared to a year-on-year growth rate of 11% in the first quarter). Although Asia, such as Japan and Shanghai, is still in the post-epidemic retaliatory demand release stage (year-on-year>100%), the revenue from parks outside the United States is limited and may not be able to make up for the growth stagnation or even decline of domestic park business.

5. Blockbuster movies are abundant, but profit margins still need to be repaired

In the second quarter, sales revenue of film and television content improved significantly compared to the previous quarter and exceeded market expectations.

In addition to the heat of "Avatar 2" in the second quarter, "Ant-Man 3" was also released in February. However, although the two Disney films performed relatively better than their peers, they did not meet expectations compared to previous series, mainly because the overall demand in the film market has not fully recovered. Fortunately, these two years are a big year for Disney movies in terms of content, so in terms of scheduling, movie revenue doesn't have to be too worried.

In addition to the heat of "Avatar 2" in the second quarter, "Ant-Man 3" was also released in February. However, although the two Disney films performed relatively better than their peers, they did not meet expectations compared to previous series, mainly because the overall demand in the film market has not fully recovered. Fortunately, these two years are a big year for Disney movies in terms of content, so in terms of scheduling, movie revenue doesn't have to be too worried.

In addition, the income from external authorization of content was greatly affected by the exclusive supply of Disney+ last quarter, and it has improved compared to the previous quarter. This is consistent with our judgment last quarter, and the reason behind it is that "under the first goal of pursuing profit growth throughout the group, this strategy may be adjusted later. For example, after the release of "Avatar 2", it may choose to authorize multiple platforms to obtain more authorization income."

The operating loss of content sales in the second quarter was still 2.3%, and there is still much room for improvement to reach the normal historical level of around 10%. The main improvement point for profit margin repair is content production costs. In the past two years, whether it is Disney or other streaming media and film production companies such as Netflix, they have been ruthless in the content arms race.

However, Netflix announced in last month's financial report that it will reduce its content spending scale this year, and even the content spending has had a large negative growth rate for two consecutive quarters. Disney has just started to decline year-on-year this quarter, and we expect that Disney's content spending this year will also shrink to a certain extent.

The trend of continued weakness in cable TV continued in the second quarter, with cable TV revenue down 7% year-on-year, further expanding from the previous quarter. Like last quarter, the main decline was in advertising revenue (down 15% year-on-year, down 12% year-on-year in the previous quarter), which is more related to user viewing time.

Due to the inertia of subscription fees and copyright fees, the impact of streaming media on cable TV still lags behind, but the year-on-year decline in the second quarter (-3.6% yoy) has expanded compared to the previous quarter (-1.9% yoy).

Nielsen data shows that the share of TV users' time spent on cable TV channels has continued to decline since the beginning of the year. In the medium and long term, cable TV's advertising revenue will continue to be under pressure, and future profit margins will also be gradually weakened, making it difficult to return to a level above 30%.

7. Rapid improvement in free cash flow

Last quarter, we talked about the urgent need for improvement in Disney's cash flow, and this quarter, management immediately executed it. In the second quarter, free cash flow net inflow was RMB 2 billion, a new high in single-quarter net inflow in nearly two years. The improvement in free cash flow mainly came from the significant increase in operating cash inflow brought about by profit improvement.

As of April 1, the company had RMB 10.4 billion in cash on its books, which improved in sync with free cash flow on a month-on-month basis.

Dolphin "Disney" related articles

Earnings season

February 9, 2022 conference call "The future belongs to streaming, but it needs to be operated reasonably (Disney 1Q23FY conference call summary)"

February 9, 2022 earnings review "The legend returns, Disney begins to change"

November 9, 2022 conference call "Disney: Focusing on profits, opening up and saving (4Q22 conference call summary)"

November 9, 2022 earnings review "The giants take turns to hammer, can even century-old Disney hold on?"

August 11, 2022 conference call "Disney: Offline demand is hot, lowering medium- and long-term streaming user guidance (3Q22 conference call summary)"

August 15, 2022 "Disney: Theme parks are still hot, streaming expansion is running"

May 12, 2022 conference call "Disney: Strong content in the second half of the year, continued prosperity in parks, lowering content licensing and closing Asian parks are unfavorable factors (2Q22 conference call summary)"On May 12, 2022, Financial Report Review: "Disney: Traditional Business Accelerates Profit Release, Striving to Infuse Blood into Streaming Media"

February 10, 2022, Telephone Conference: "Gradually Entering the Content Cycle, Management is Confident in Growth Targets (Disney Telephone Conference Summary)"

February 10, 2022, Financial Report Review: "Disney: Streaming Media Growth Recovers Glory, Theme Parks are Even More Beautiful"

November 11, 2021, Telephone Conference: "The Impact of the Epidemic, Disney's Content Cycle in the Second Half of the 2022 Fiscal Year (Telephone Conference Summary)"

November 11, 2021, Financial Report Review: "Streaming Media Growth Collapses, Disney's Long Transformation Road is Difficult to Walk?"

In-depth

June 1, 2022, "Disney: Streaming Media Bubble Burst, Returning to the Theme Park's Roots"

October 10, 2021, "Disney: The 'Anti-Aging Technique' of the Hundred-Year-Old Princess"

October 15, 2021, "Can Disney, Who Continuously 'Creates Dreams', Have a 'Dreamy Valuation'?"

Risk Disclosure and Statement for this Article: Dolphin Research Disclaimer and General Disclosure

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.