After a violent rebound, is it "to go" or "to stay" for Hong Kong stocks?

I'm PortAI, I can summarize articles.

-

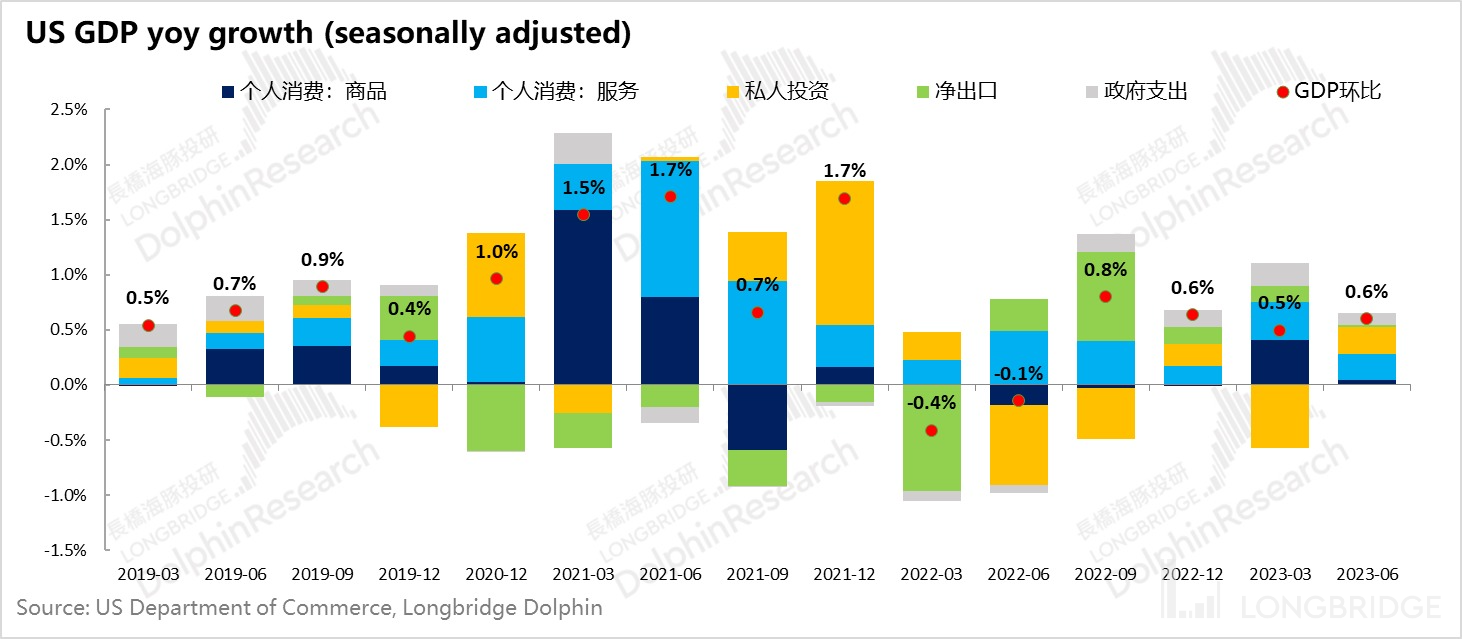

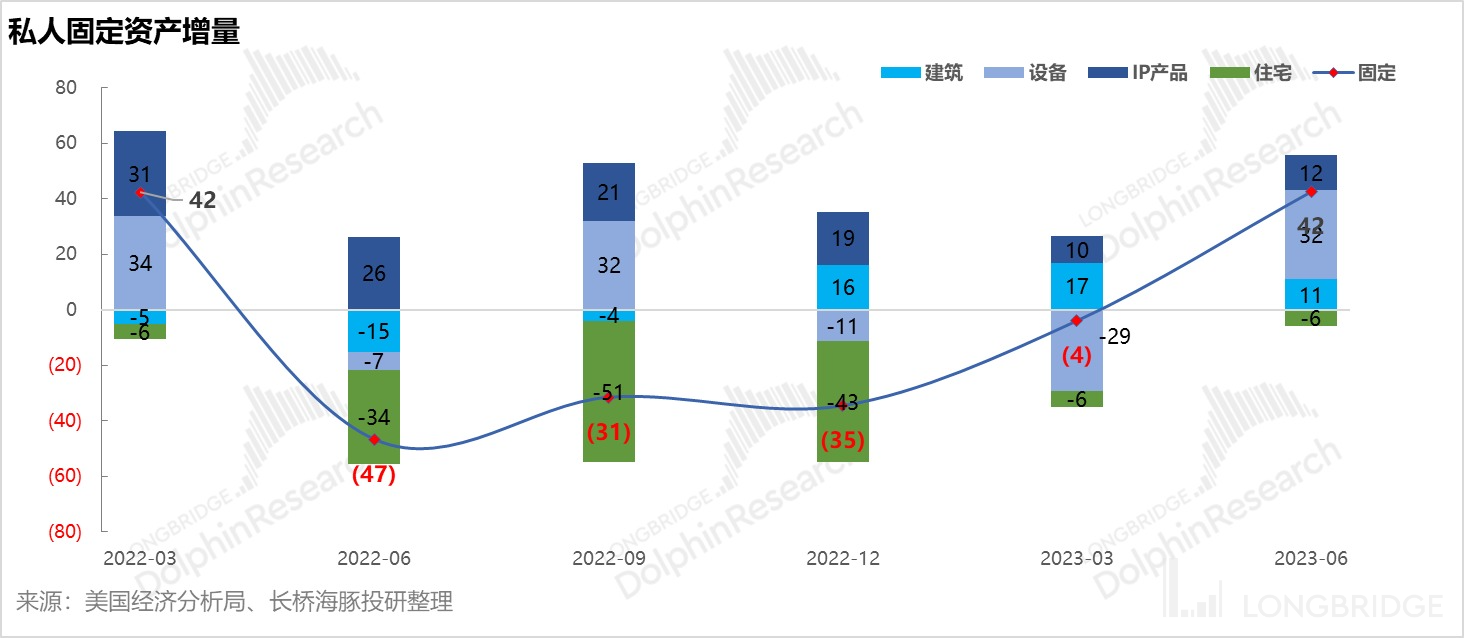

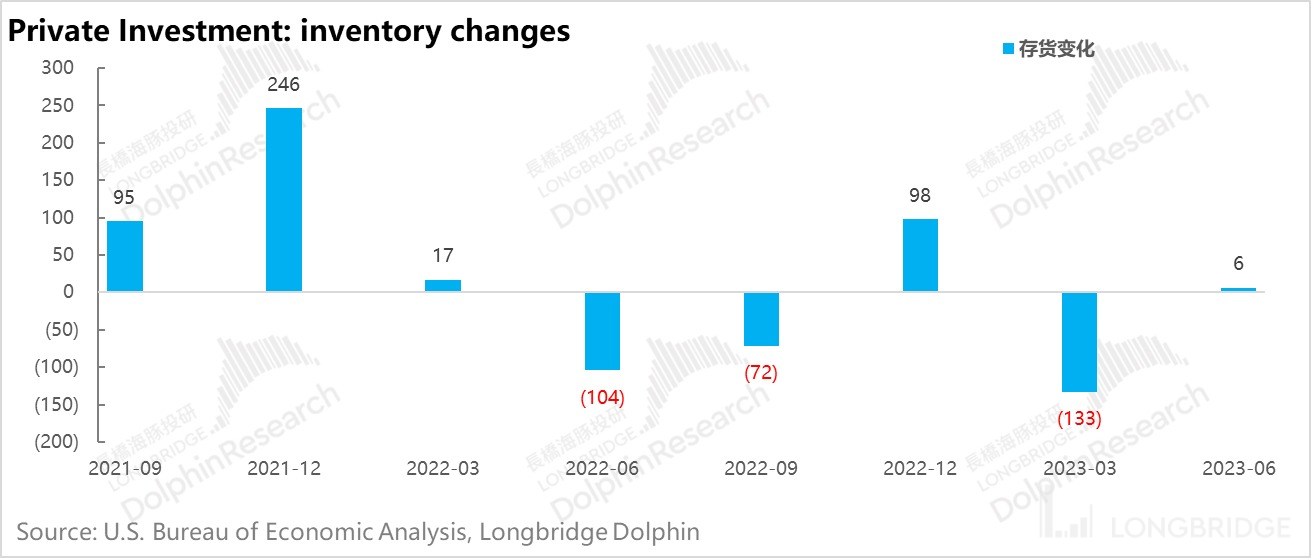

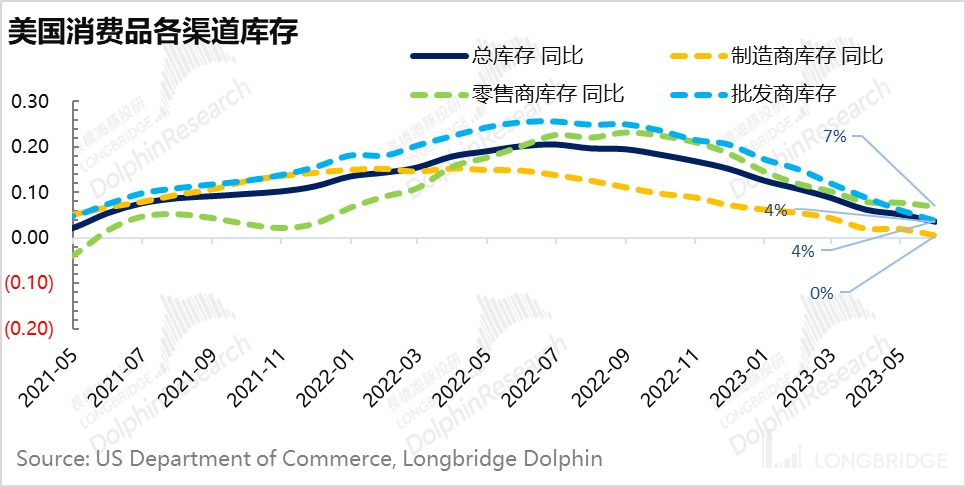

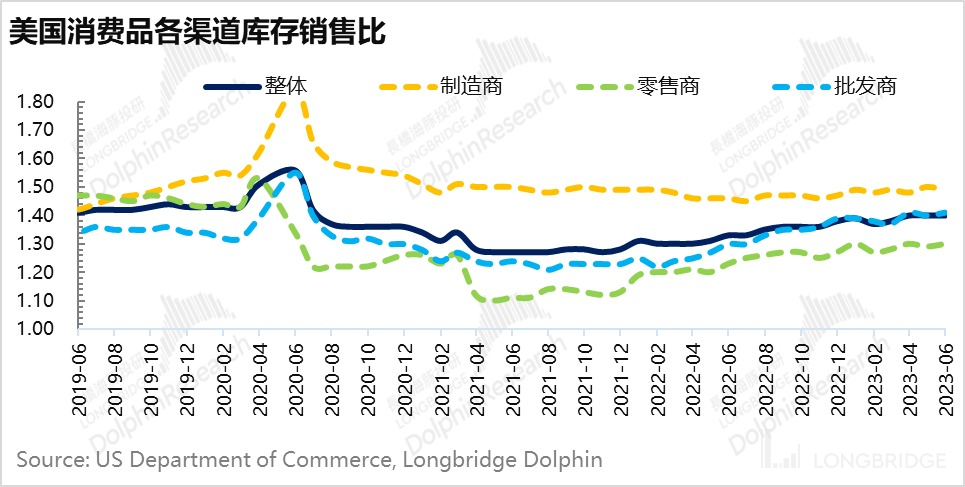

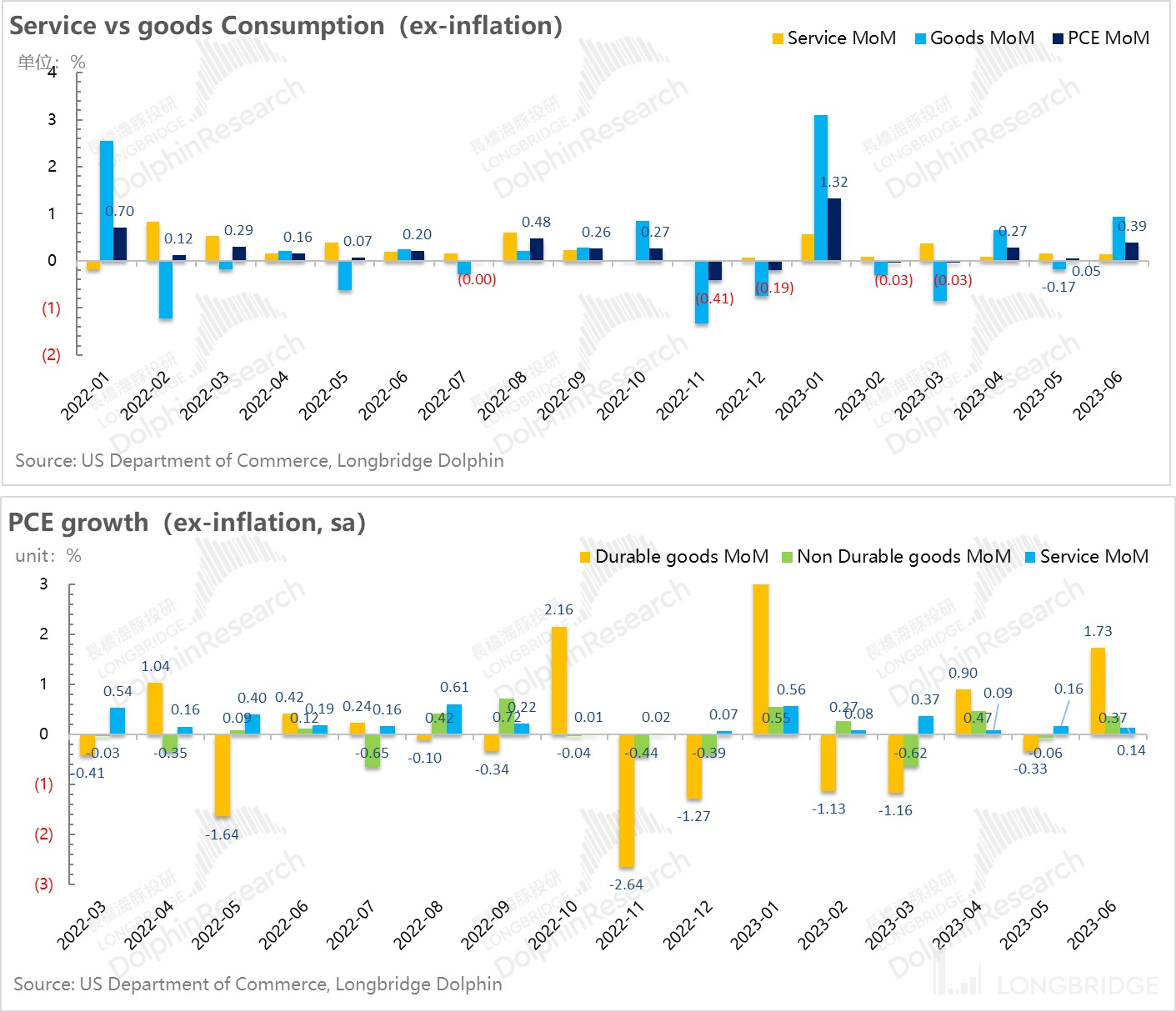

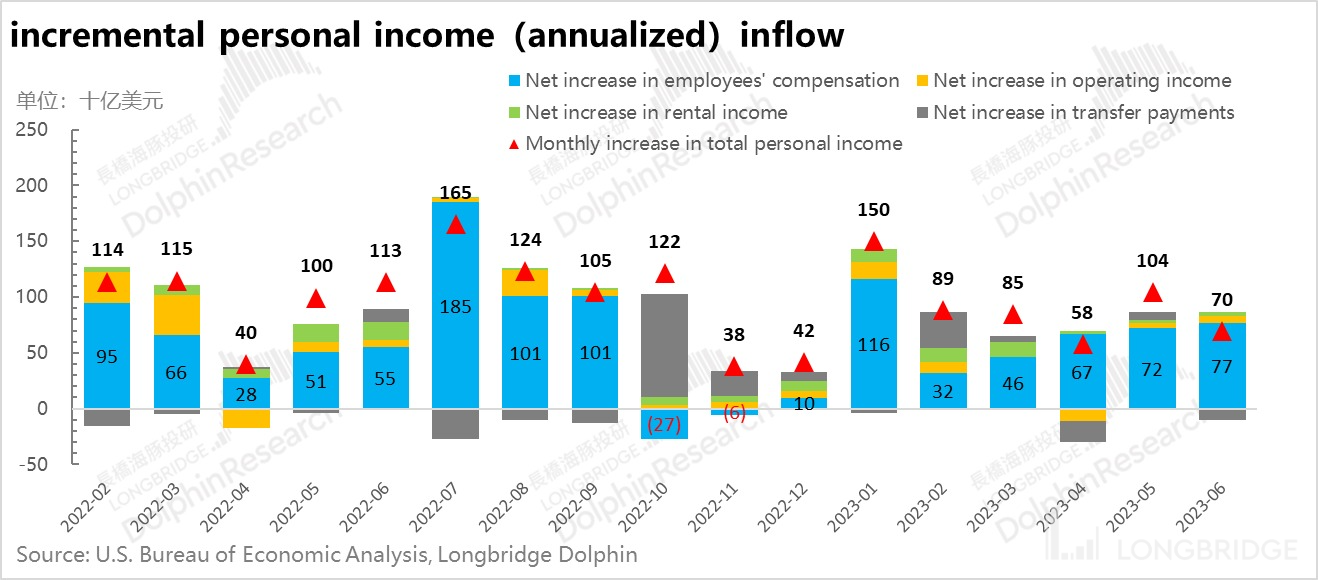

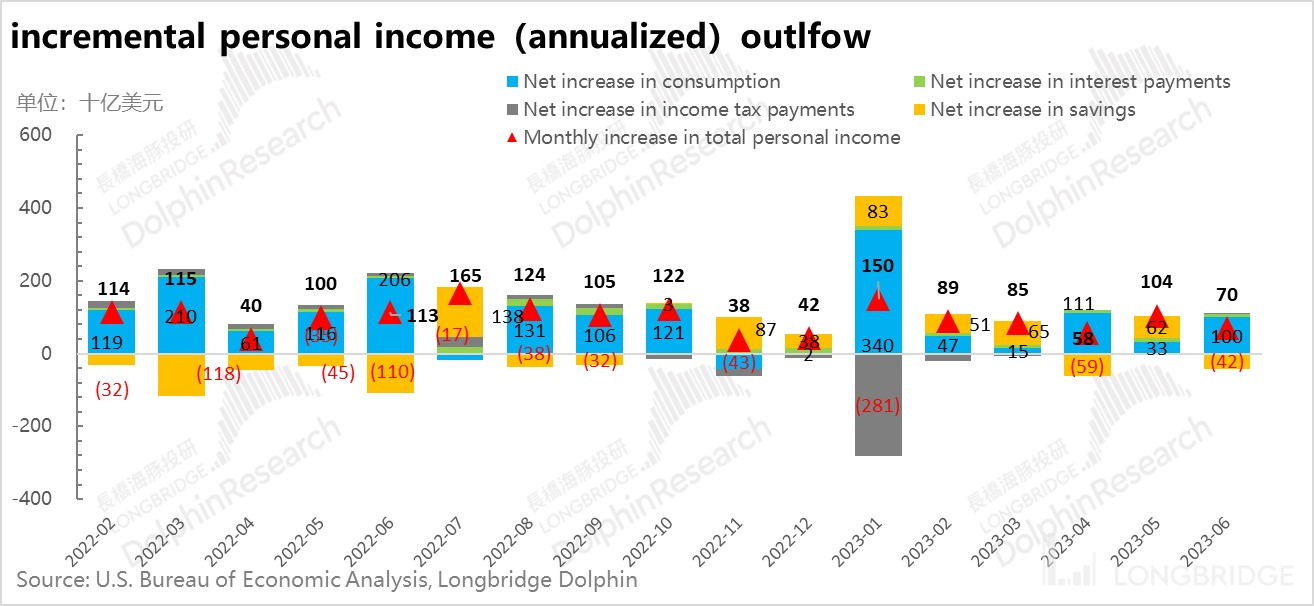

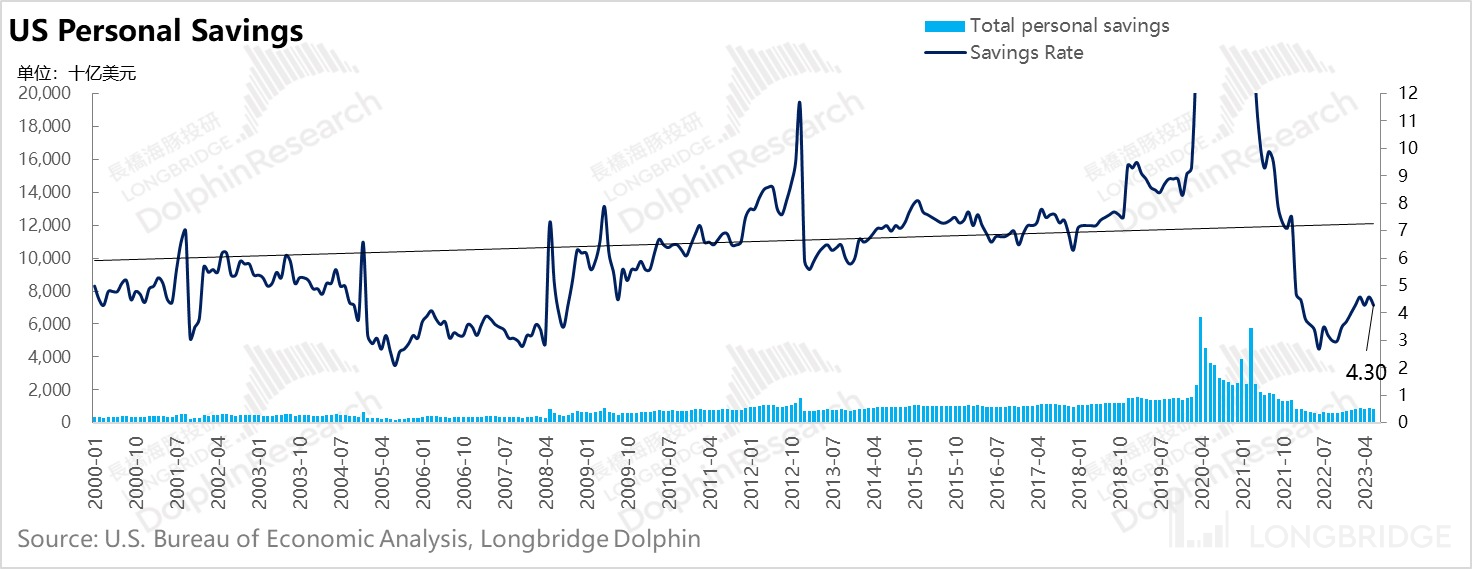

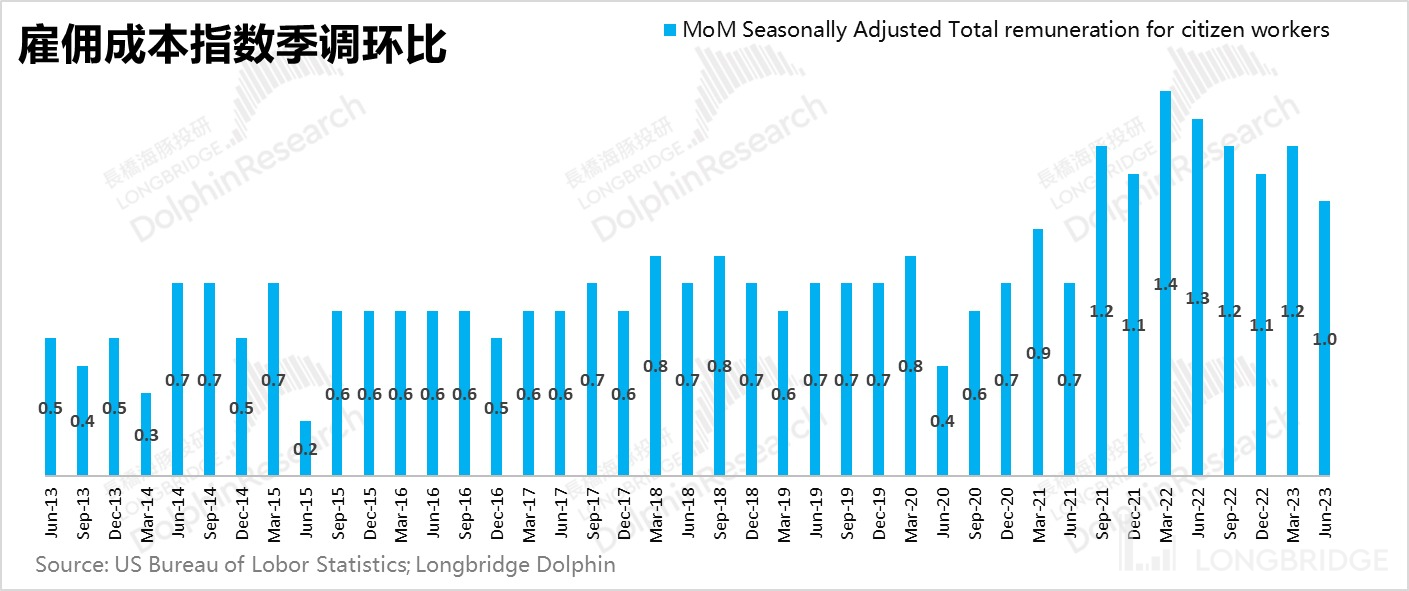

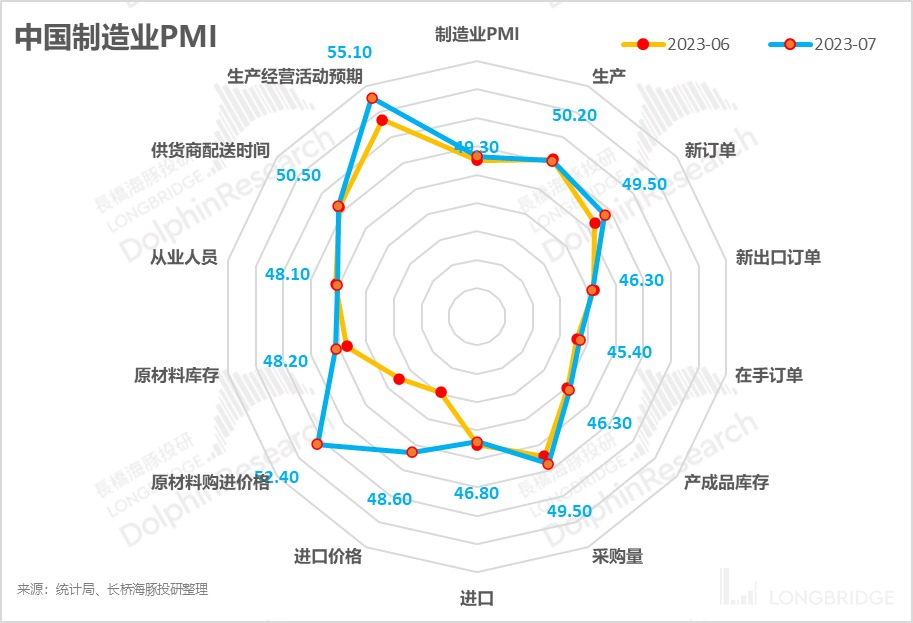

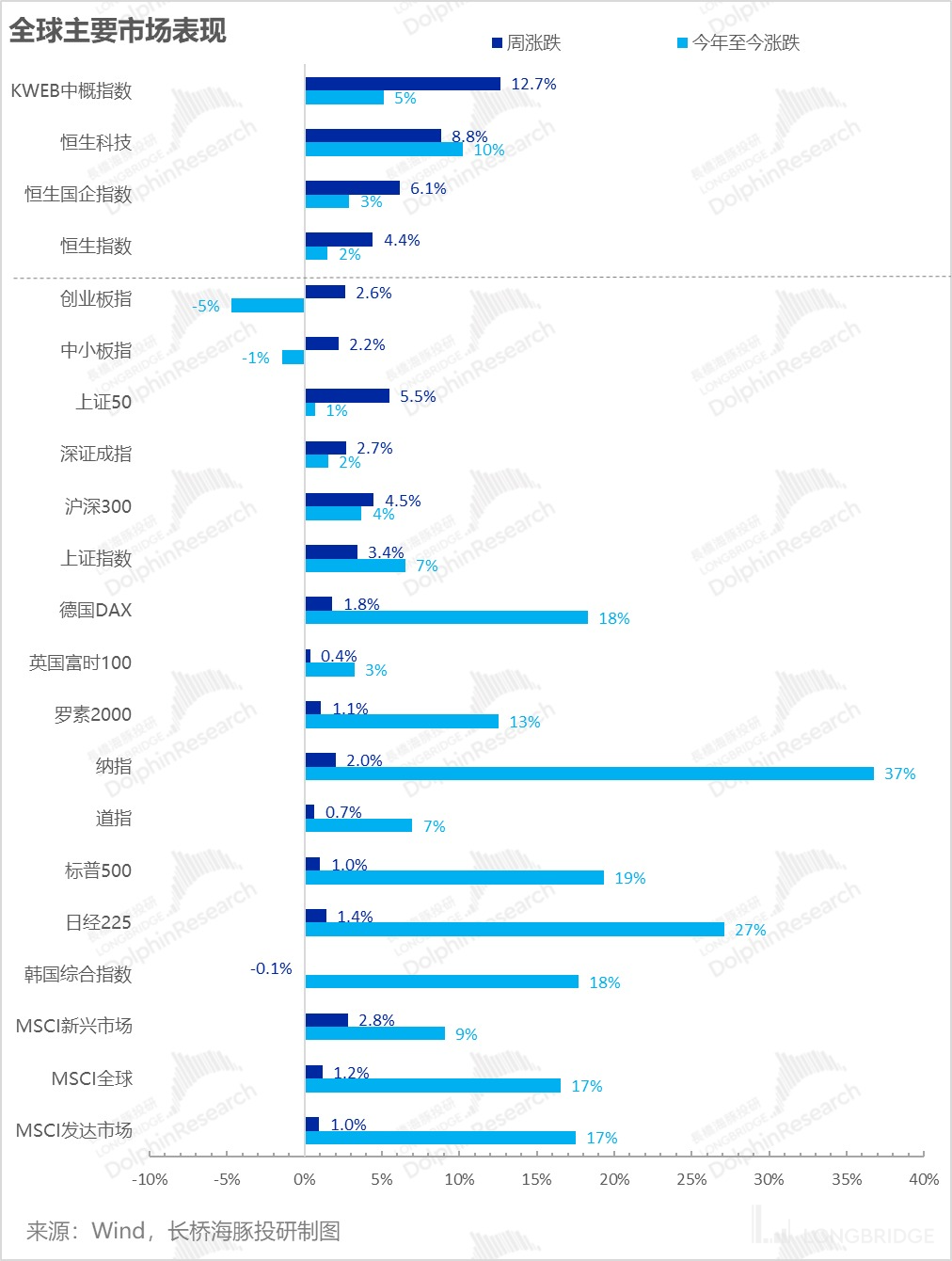

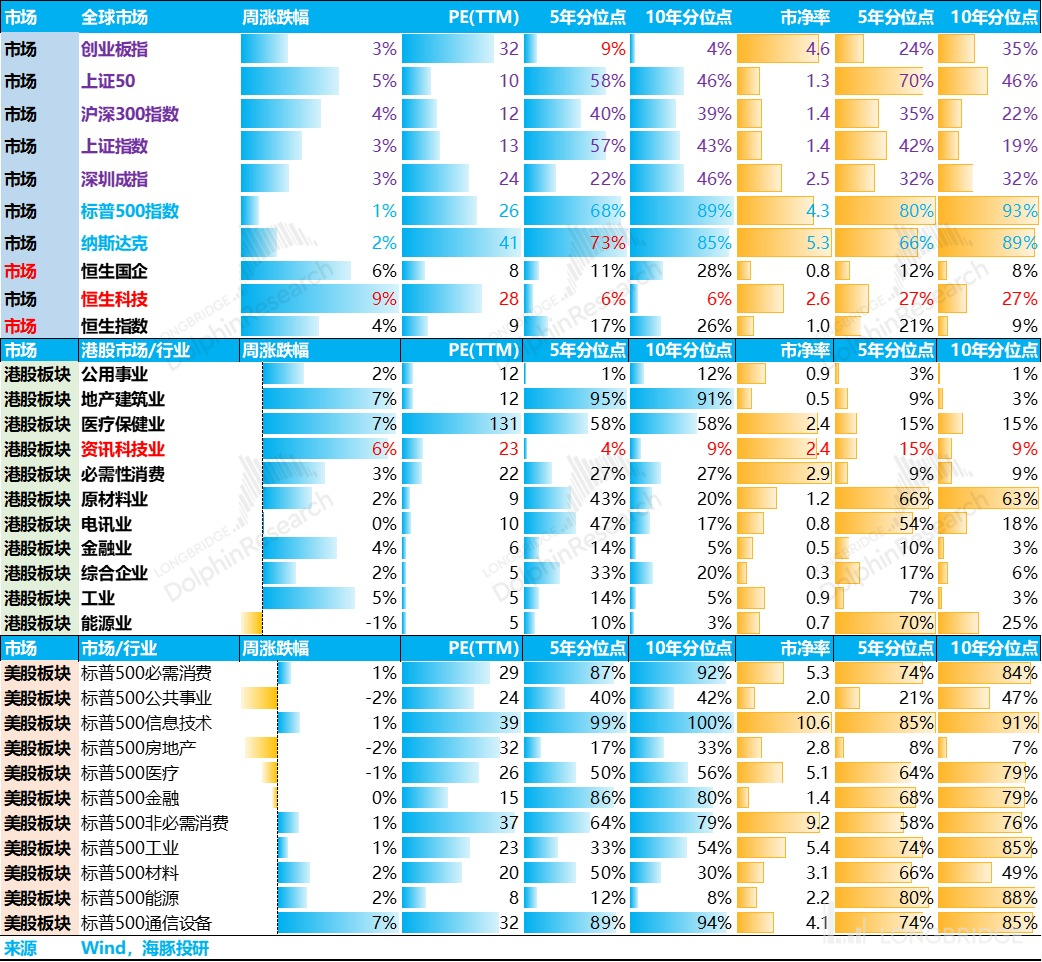

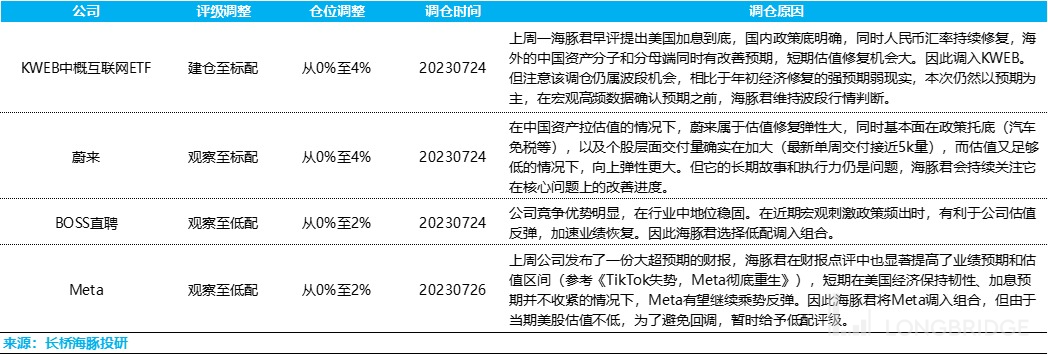

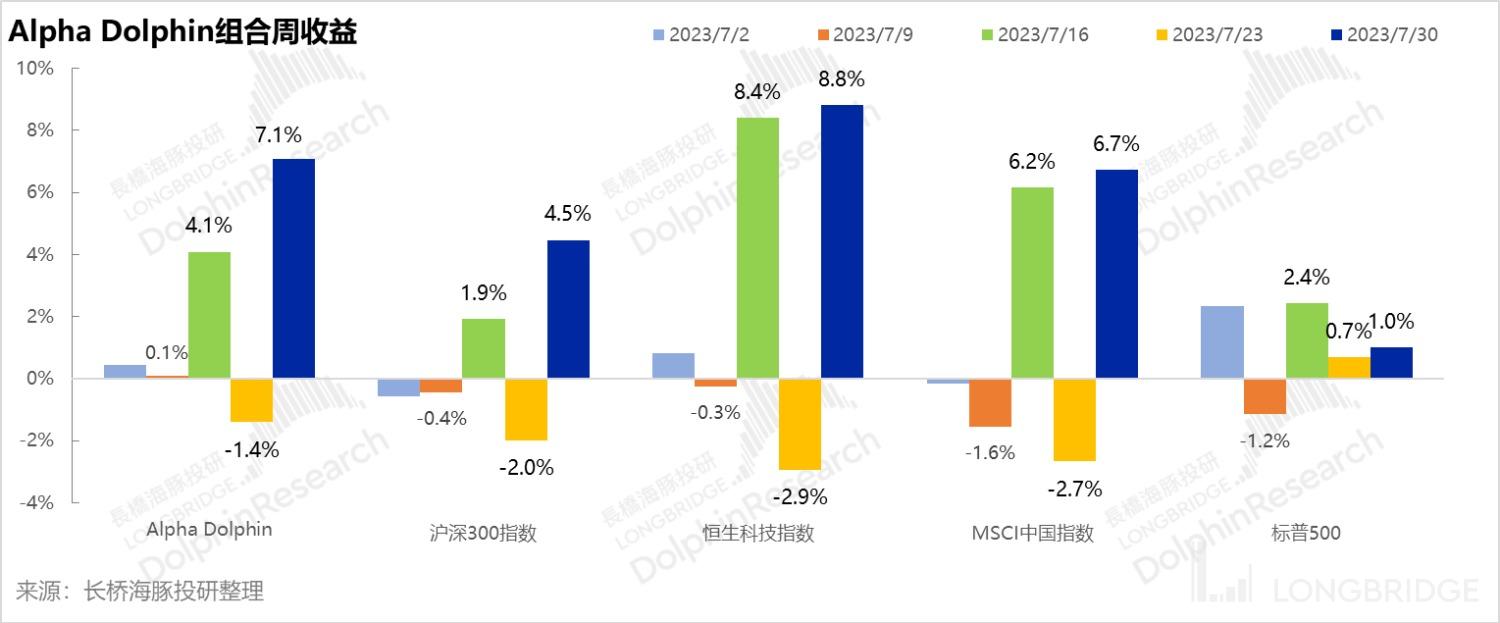

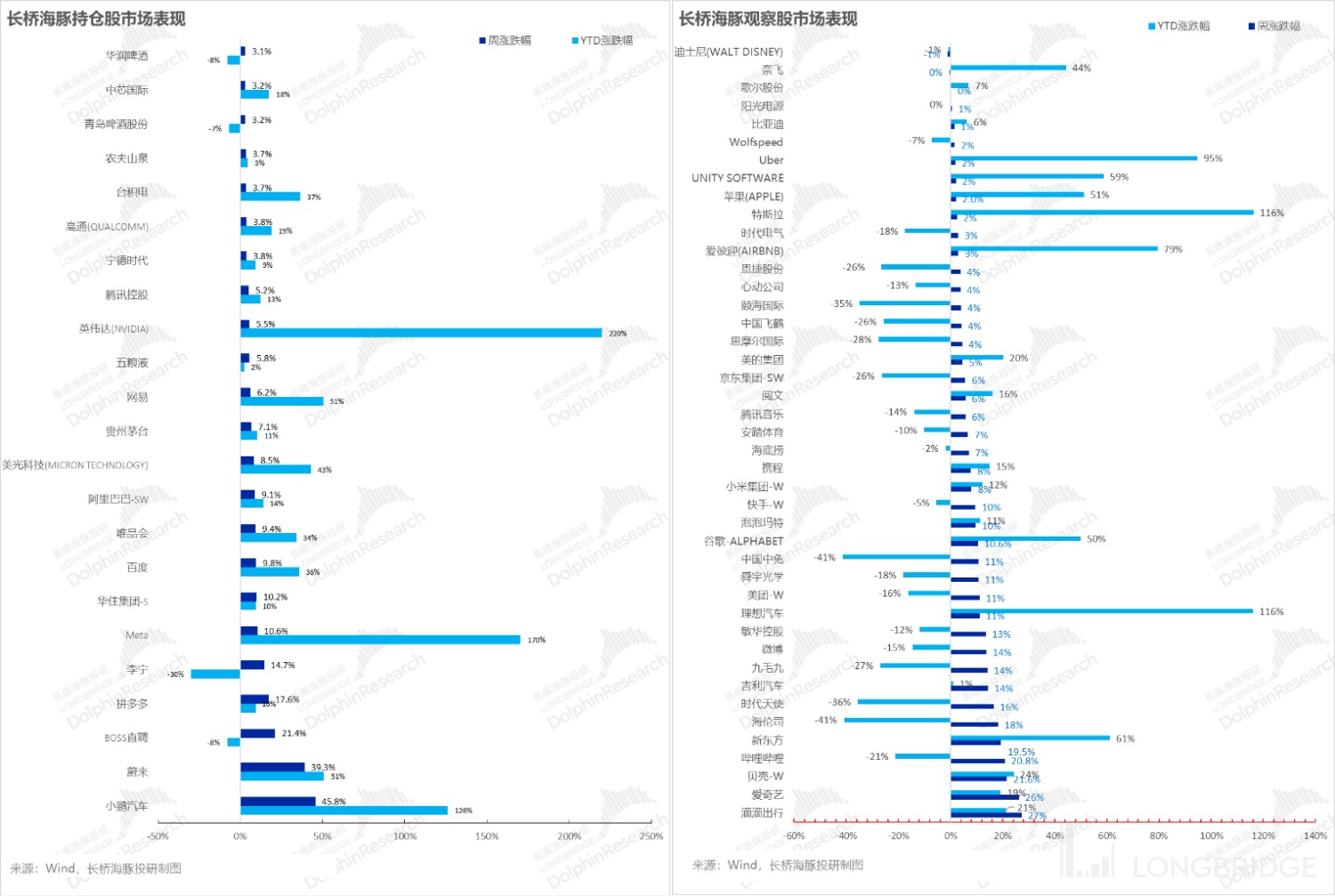

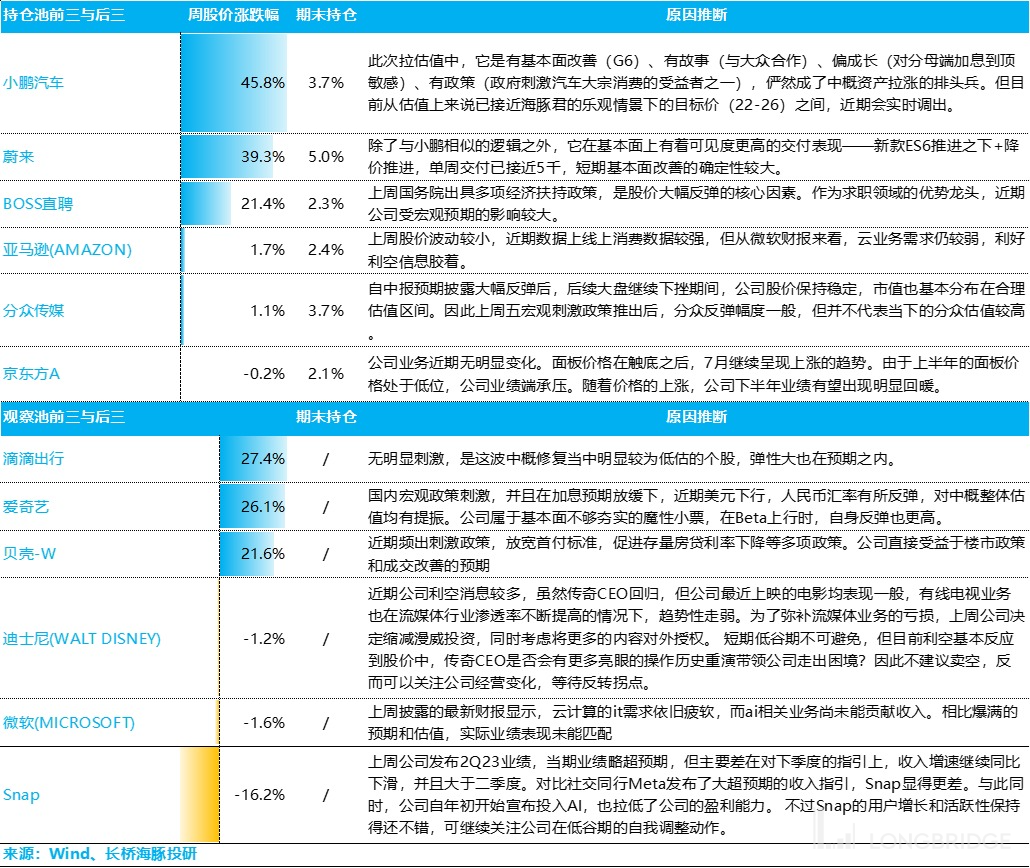

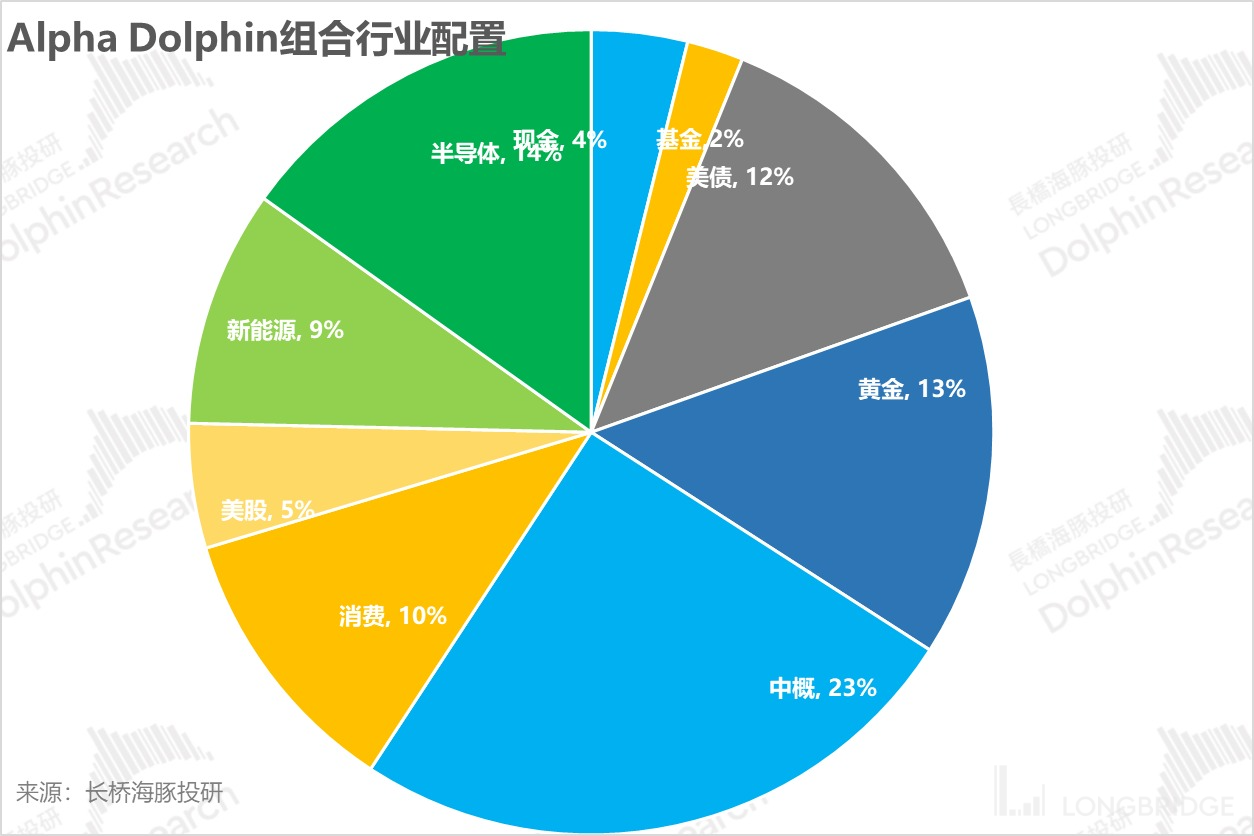

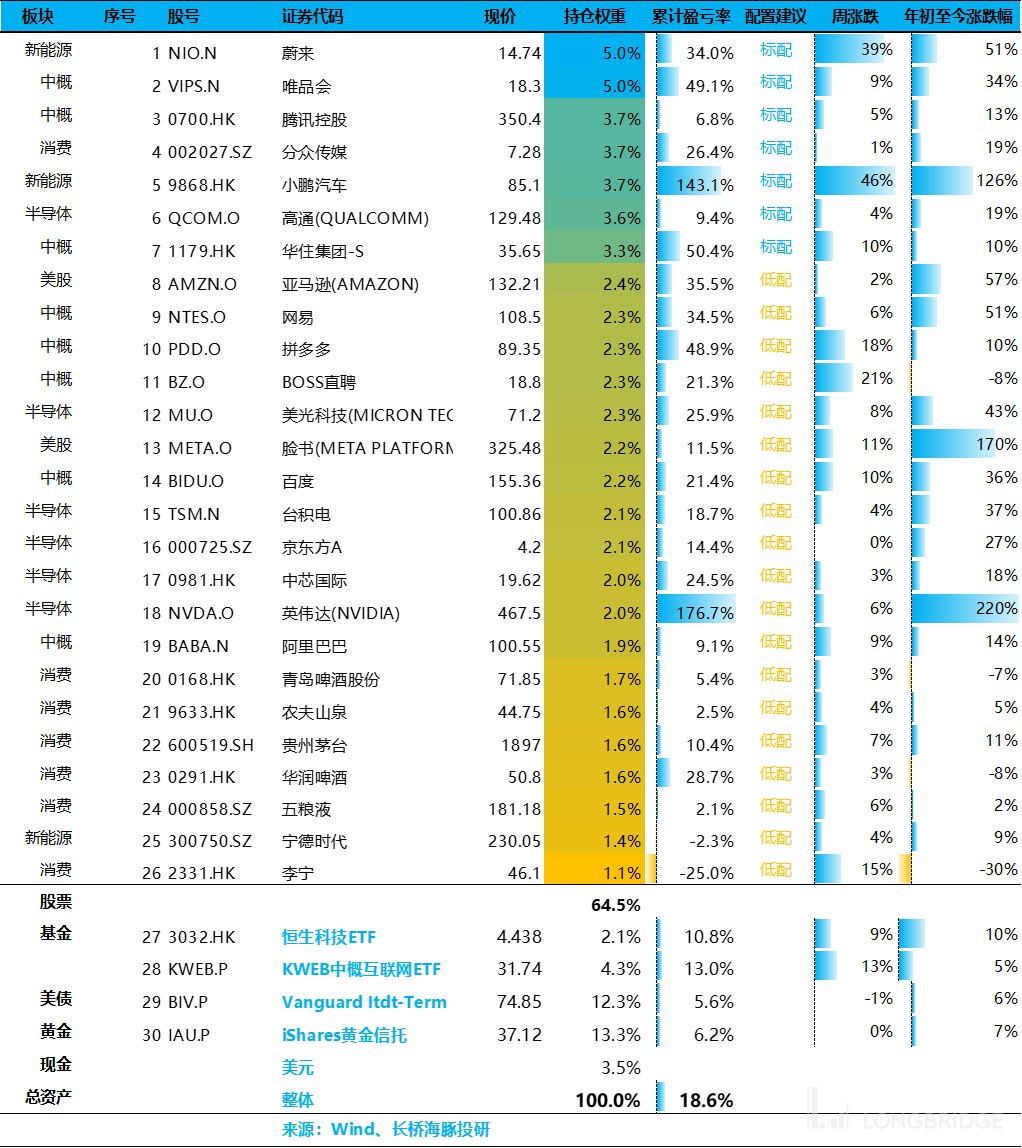

- Hello, everyone, the following is the core information of this week's portfolio strategy summarized by Dolphin Jun this week: * * * 1)* Behind the fact that the US economy exceeded expectations in the second quarter (2.4 year-on-year discount from the previous quarter), the domestic demand of enterprises was relayed (investment demand was significantly positive due to the return of manufacturing industry + technology investment, at the same time to inventory came to an end) the relatively weak consumption of goods on the residential side, driving economic growth in the second quarter but stronger than in the first quarter. * * 2)* * From all dimensions, the U.S. economy seems to have fallen to a position close to the normal level except that labor inflation has not reached the target level due to the tight labor market. "U.S. residents have oversaved surplus food, prices in the whole society have fallen, and GDP as a whole is still there." The second quarter is what Dolphin Jun calls the most "ROSY" perfect period. The magnitude of the subsequent slowdown still depends on whether the savings rate will go down after the depletion of excess savings in the United States and the decline in the marginal employment of residents, thus suppressing double-depressing consumption, but the overall probability of a soft landing is already the benchmark scenario from the current progress. 3) U.S. interest rate hikes to the top, domestic policy bottom is now, overseas Chinese assets are undervalued enough, superimposed on the RMB exchange rate repair, last week there was a sense of a violent rebound in Chinese assets at the beginning of the year. Dolphin Jun has increased its position in overseas Chinese assets based on the judgment of previous valuation repairs (see text for details). From the perspective of repair rhythm: a) molecular side influencing factors: this week, there was no centralized data release in domestic macro, with little negative interference and continuous release of policy stimulus; B) on the influence factors of 10-year U.S. debt at the denominator end: there was new non-agricultural employment data for July this Friday. with the national debt interest rate already at a high level of 4%, the downward probability of the yield will exceed the upward probability unless the employment data further burst, the U.S. employment data for June has tended to be normal; c) The Hang Seng Index, as well as the segmented Hang Seng Technology and other sector indices, are still at historically low levels, such as the 5-year PE split, which is from 4% to 6% after the Hang Seng Technology rally, is still clearly undervalued. Therefore, although the market still has frequent policy documents but insufficient policy landing concerns, but the short-term macro interference factors are not large, its own valuation is still low, so there is still room for repair. However, due to the strong expectations of weak reality at the beginning of the memory is more profound, Dolphin Jun believes that this week can focus on some of the fundamentals are stronger but still relatively undervalued pan-consumer stocks, but before the economic repair data verification, such opportunities are still partial band opportunities. Here are the details: 1. corporate domestic demand relay, the U.S. economy instead slightly accelerated From the second quarter of the U.S. GDP growth rate, the U.S. economy instead slightly accelerated, the second quarter ring growth rate reached 0.6 percent (corresponding to 2.4 percent year-on-year). Among them, service consumption, as always, is mainly stable, while commodity consumption performance is relatively weak, and high-frequency residential consumption data is not much deviation.! The biggest marginal change in the second quarter was the restart of corporate domestic demand, which contributed to GDP by the same amount as commodity consumption (18%). Domestic demand of enterprises is divided into: **a) investment in fixed assets: ordinary enterprises to build factories, tangible assets to buy equipment, intangible assets to buy IP; Residential investment. * * In these categories, residential investment has actually stabilized in the last quarter after three quarters of continuous destocking. In the second quarter, construction investment, which is mainly to expand the nature of factory buildings, has been pulled for two consecutive quarters, and equipment purchases have begun to restart obviously. However, the intellectual property investment of enterprises is almost of an anti-cyclical nature. No matter what the cycle is, the IP investment of American enterprises has always been a Poseidon needle.! **B) Inventory investment: * * As inventory is easier to adjust than fixed asset investment, inventory changes have been relatively large: after the United States entered the interest rate hike cycle, except for the replenishment of petrochemical enterprises in the fourth quarter of last year, the inventory of enterprises has basically been reduced in the past year and a half, especially in the first quarter of this year. However, in the second quarter, the de-stocking of enterprises has come to an end. Under the condition that residents' consumption continues to be strong, the de-stocking of enterprises has bottomed out. The inventory in the second quarter increased by 9.3 billion, an increase of 6 billion US dollars over the quarter.! This also corroborates with the current channel inventory status in the United States: the current inventory of various channels has been de-stocked for some time, compared to the pre-epidemic is still relatively high mainly intermediate link wholesalers inventory levels. Looking at the destocking progress of wholesalers in detail, the year-on-year growth rate was 4% in May, while the month-on-month growth rate has been restored from negative growth to 0 growth, which also shows that destocking is nearing the end.! ! Combined with the above, it can be seen that the real core behind the key of GDP exceeding expectations in the second quarter is that under the condition that domestic demand of residents continues to be cut off, domestic demand of enterprises begins to return, especially when inventory bottoms out while fixed asset investment shrinks month-on-month for a full year, and the increase in investment is greater. **But if the outlook is from a corporate domestic demand perspective, the subsequent big probability will depend mainly on the repair of auto manufacturing and the continued return of high-tech manufacturing under the IRA and Semiconductor Acts. And fixed asset investment in the residential sector, from the downstream of the latest 1. of second-hand housing data, although the inventory is at a low level, but high interest rates under the * * * slow sales * * is still a fact, June quarter after the new house sales, sales prices, as well as second-hand housing sales, again into the ring down state. Overall **, although the enterprise to inventory has entered the end of the stage, but high interest rates under some industries are still difficult to enter a significant pull up state, the subsequent marginal change in the magnitude of the return to the residents of domestic demand. Next, let's take a closer look at the performance of domestic demand in June. * * * * June 2. U.S. domestic demand: durable goods counter-attack * * June inflation-stripping real consumer spending was clearly strong, with a 0.4 percent month-on-month increase significantly higher than in the previous four months. The key to growth is mainly the consumption of durable goods in commodity consumption. After a downturn in May, durable goods consumption pulled up again, by 1.7 percent month-on-month, while non-durable goods consumption was relatively flat and service consumption was relatively weak. A closer look at the sub-items, mainly durable goods in the car, including new and used cars, repair is strong, while durable goods in the entertainment goods (audio and video, 3C digital, etc.) consumption growth is also relatively strong.! * * Americans continue to buy in buy buy, driven by the high employment rate driven by the strong recruitment demand of enterprises, and the growth of personal income is better * *: personal income (nominal, quarterly, discount year) increased by 70 billion in June compared with may, mainly driven by the increase in residents' salary income, which is essentially a better increase in employment and salary.! In June, the outflow direction of personal income increased by US $100 billion in individual consumption, and the increase in consumption was significantly higher than income. The main reason here is that the household savings rate declined in June.! The household savings rate fell again to 4.3 per cent in June. In the wake of the U.S. stock epidemic, the savings rate has hovered around 4-4.5 percent after repairing from a June 2022 low of 2.7 percent to 4 percent, and the savings rate is no longer rising further. The last wave of savings rates that fell so low basically dates back to 2005-2007, when U.S. credit consumption was super strong. The overall debt ratio of the residential sector is low, which is different from the last credit consumption. Behind the scenes, in Dolphin Jun's view, it should still be the excess security brought about by full employment + excess savings + asset appreciation.! * * 3. PCE: Confirms Price Falling * * In June, the Federal Reserve was more concerned about the price index PCE entering less than 3% year-on-year, while the core PCE also fell back to 4.1% year-on-year; On a month-on-month basis, the growth rate of core PCE and Headline PCE was 0.17 and 0.16 respectively, both have fallen between the Fed's target of 0.15-0.2 per cent (corresponding to 1.8-2.4 per cent year-on-year). And the Fed's concern about human inflation, from the second quarter of the latest worker employment cost index, the quarter-on-quarter adjustment has further fallen back to 1%, corresponding to about 4% year-on-year, although down but still significantly higher than the pre-epidemic historical average of about 0.5-0.7 percent.! On the whole, it can still be clearly seen that among the constituent elements of prices, the current elements of resources (food, oil), capital (housing), and technical prices (electricity, transportation, etc.) have all clearly entered the inflation release channel, leaving only one human element that seems to have been released, and the progress is much slower than other elements. In terms of the current interest rate vs price contest: core inflation within 4 per cent, compared to the policy rate of 5.25-5 per cent, the real yield is already in the positive territory and the interest rate has reached a restrictive level. The key to solving manpower inflation is to stay at high interest rates for a period of time, to see that the job market gradually tends to balance, and to ensure that manpower also enters an obvious de-inflationary channel. * * Summary: * * * Overall, at present, the U.S. economy seems to have fallen to a position close to the normal level except that the labor market tension has caused manpower inflation to fail to reach the target position from all dimensions. "U.S. residents have over-saved surplus food, prices in the whole society have fallen, and GDP as a whole is still there." The second quarter is the perfect period for what Dolphin Jun calls the most "ROSY. **This is also the core reason why the market is now generally trading a soft landing in the United States, and the subsequent slowdown still depends on whether the savings rate will go down after the depletion of excess savings in the United States and the decline in the marginal employment of residents, thus suppressing double-depressing consumption. And in turn look at the domestic economy, through a series of policy documents to promote consumption, promote private investment, can already clearly see the urgency of economic repair, the policy bottom is very clear, and the remaining key is to see the gradual realization of the macro high-frequency data. Judging from the latest forward-looking indicators, although the official manufacturing PMI data in July did not reach the watershed of 50, it was slightly repaired compared with June, and key sub-items such as new orders, production and business activity expectations, and procurement volume have been repaired to a certain extent, which is a slight benefit.! Fourth, where did the market trade go? After the US interest rate hike peaked last week, indices around the world are on the rise, while Chinese assets have risen more because of their previous adjustment and undervaluation.! Whether the gains can be preserved after the valuation repair depends on the extent to which the economic data is on the ground. Especially in the context of this year's interest rate hike, the global economy as a whole is still within the tight currency cycle, there is no basis for the dollar water buffalo, the final asset increase is mainly to see the degree of fulfillment of fundamental expectations. But in the short term, this week's macro domestic PMI performance on Monday was barely OK, with the latest January employment data from the US on Friday. And last month there was a cooling trend in new U.S. employment, which, if consistent with the June forecast, will not affect expectations of a repair to the denominator side of China's assets. At the same time, with the U.S. 10-year Treasury note still at a high level of close to 4%, if the number of new jobs in July is not enough, it will not be enough to further raise the yield of long-term Treasury bonds. Under such circumstances, Dolphin Jun thinks that the restoration of Chinese assets still has hope to last for a few days. The core is that the current valuation cost performance is still good. In the restoration in early January, the PE valuation of Hang Seng Technology Assets returned to 50% of the historical level, while the current level is still at 6%. The Hang Seng State-owned Enterprises and Hang Seng Index are less than 30% of the historical level from the 10-year dimension. However, unlike last week's general rise, Dolphin Jun tends to think that it is necessary to select sectors and individual stocks at present, and it is necessary to find out that the fundamentals are performing well, but some social services such as tourism and catering, which are seriously valued, and the consumption of necessities such as beverages, which are less affected by the cycle.! * * 5. portfolio position adjustment * * Based on the judgment of relieving the pressure on the numerator and denominator of Chinese assets, Dolphin Jun transferred positions and increased positions in Chinese assets last week. The specific reasons for the increase in assets are as follows: among them, Wei Lai is undervalued on the one hand, but the key is due to fundamental repair, delivery starts to start, and buying short-term valuation repair logic; The BOSS direct employment core is also undervalued, the industry is greatly affected by the macro, but its own industry competitiveness is strong, the company's execution is reliable.! * * 6. Portfolio Income * * In the week of July 28, Alpha Dolphin virtual portfolio income rose 7.1 per cent, outperforming the S & P 500 Index (+1 per cent), the Shanghai and Shenzhen 300(+4.5 per cent) and the MSCI China Index (+6.7 per cent), but slightly below the Hang Seng Technology Index (+8.8 per cent).! Since the portfolio was tested to the end of last week, the absolute return of the portfolio was 31% and the excess return compared to MSCI China was 48%. From the perspective of net asset value, Dolphin Jun's initial virtual asset is 0.1 billion US dollars, currently 0.133 billion US dollars.! 7. individual stock profit and loss contribution Last week's portfolio rose a lot, whether it's the Internet or consumer, have got the growth + undervaluation style production, or both. On the contrary, the fundamentals are sound, the previous decline is not high companies rose little, last week's overall valuation of the characteristics are very obvious.! For the companies with the highest rise and fall, Dolphin King sorted out the reasons as follows:! 8. Portfolio Asset Distribution After this week's portfolio transfer, 24 stocks or ETFs were allocated, of which 8 were rated as standard, 19 were rated low, and the rest were gold, U.S. bonds and U.S. dollar cash. As of the end of last week, Alpha's Dolphin asset allocation allocation and equity asset position weights were as follows:! ! * * 9. this week's key events: * * This week's macro data entered a new month, mainly setting the tone for the follow-up data on the new employment population and hourly wages in July. In the earnings season, the company covered by Dolphin Jun entered the Internet receipt pile-up week, leaving only Apple and Amazon on the big ticket, plus AMD, which currently has a high degree of attention. Specific concerns Dolphin Jun is organized as follows, when you can pay attention to Dolphin Jun's first financial interpretation.! Risk disclosures and statements in this article: Dolphin Investment Research Disclaimer and General Disclosures For a recent article in the Dolphin Investment Research Portfolio Weekly, please refer to: "U.S. interest rate hike to the top, Hong Kong stocks are saved?" How far can China rebound when reality strikes? " Look further, will US interest rate hikes add to stagflation?" Decoding the Mystery of Low U.S. Savings, Is It Sustainable? " The U.S. Housing Market: Subprime Original Sin, Why Resist This time?" "cocooning: where did the recession go and can it still come?" "Small composition about the market? Extreme pessimism followed by overcorrection is the core" U.S. stock orgy? The economy is fine, beware of extreme joy and sorrow Purgatory vs Carnival, what are US and Hong Kong stocks trading? " U.S. Stocks Pull Valuation, Hong Kong Stocks Kill Beta? Don't despair, a reversal is imminent" High interest rates put in a bank again? The chances of a soft landing are greater" ChatGPT vs Performance Release, Can Giant Zha Push hold up U.S. Stocks? "Does the good" US recession, China recovery "have to be ruined?" U.S. Recession Direction Set, Just Small Decline, Big Decline "U.S. Service Consumption Collapses, U.S. Stocks Celebrate?" "Fed rate cut: just one short of a U.S. version of the balance sneak attack moment?" U.S. stocks to recession, to cut interest rates? Anyway, the deal is already in place "Silicon Valley Bank Run Crisis: Is the U.S. Recession to Run?" U.S. stocks back to spit out trade rush, the world finally can breathe "" Inflation heads up real hammer? It is an opportunity to turn away from Thailand "Inflation aside, signals from Ali and Baidu are more important" "Hong Kong, America, Qi Qi Weak Chicken, Wolf Coming Again?" High-frequency macro marionettes, U.S. stocks are puppet cities "" A positive line changes faith, Tesla led U.S. stocks to kill back? "How far is the" crisis "and" opportunity "of US stocks" US stocks are not red for the New Year, but the performance hammer is just around the corner? "Picking the Roots of Stagflation in U.S. Stocks" CPI Has Fallen, Why Is the Fed Still on This Axis? " Is service inflation really that easy to eliminate? Beware of market overkill Hong Kong stocks finally have a" waist? The independent market can go a while " " The Darkness Before Dawn: Mentality Refocuses on Darkness or Dawn "" U.S. stocks "beat back" reality, how long can emerging markets jump? "Global Xiti Valuation Repair? And the performance test" "China's asset violence pulls up, why China and the United States glacial two days" "Amazon, Google, Microsoft superstars fall? U.S. stocks" meteor shower "still have to go down" "Behind the policy shift expectations: weak" strong dollar "GDP growth?" "South to take over vs. North to go crazy, it's time to test" concentration "again" "Slow down and raise interest rates? Dream Shattered Again" Re-understanding a "Iron and Blood" Federal Reserve "" Tragic Second Quarter: "Eagle Voice" Loud, Collective Difficulties "" Falling to Doubt Life, Is There Any Hope of Reversing the Length of Despair? " 'Federal Reserve Violent Hammer Inflation, Domestic consumption opportunities instead? "The world has plummeted again, and the lack of people in the United States is the root cause of the disease" The Federal Reserve has become the number one short seller, the global market has fallen to its knees A bloody case triggered by a rumor: the risk has never been clear, and sugar is found in the glass slag The United States goes left, China goes right, the price/performance ratio of U.S. assets is back layoffs are too slow to take over, and the U.S. has to continue to "decline" U.S. stock-style "funeral": recession is a good thing, the fiercest interest rate hike is a bad thing interest rate hike enters the second half, "Performance Thunder" opens Epidemic to Counter, U.S. to Recession, Funds to Reverse "Chinese Assets Right Now: U.S. Stocks" No News Is Good News " " Growth Has Bold, But Is America Must Be a Recession? " " Is the United States in 2023 a recession or stagflation? " U.S. Oil Inflation, China's New Energy Vehicles Bigger and Stronger?" "Fed raises interest rates faster, Chinese asset opportunities come instead" U.S. stock inflation has exploded again, how far can a good rebound go? " This is the most grounded gas, the dolphin portfolio has run away

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments