Is the US government spending money like water? The backlash has arrived!

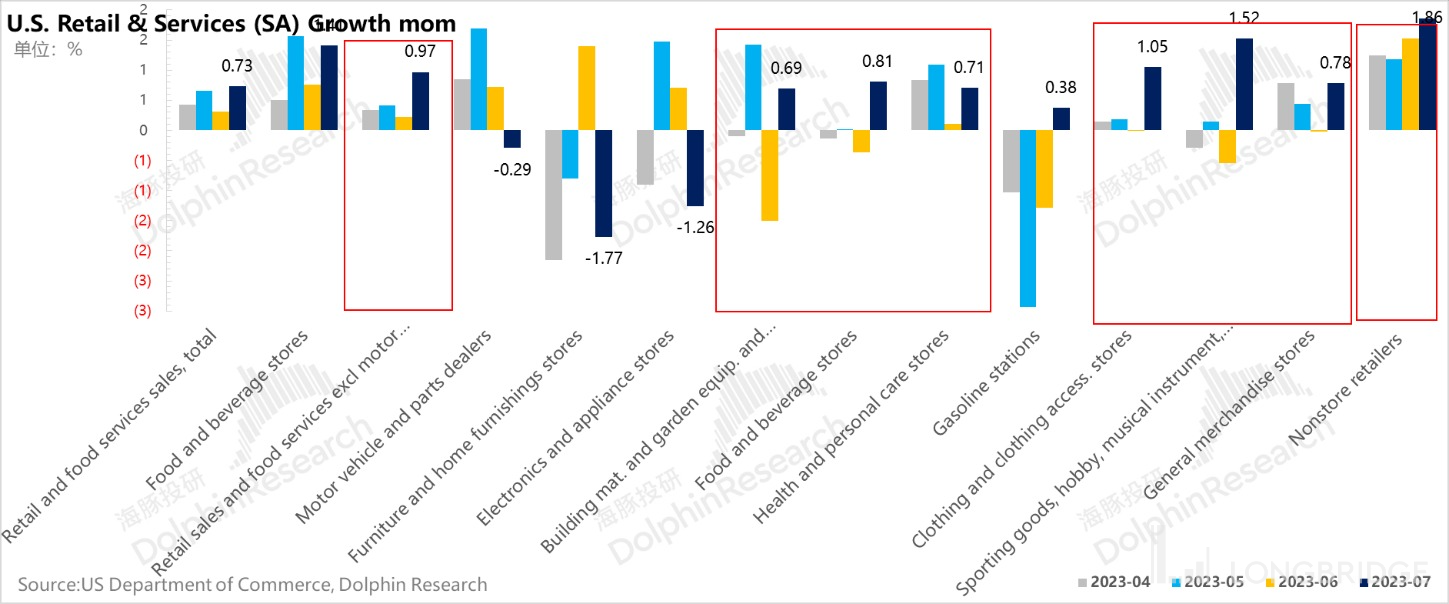

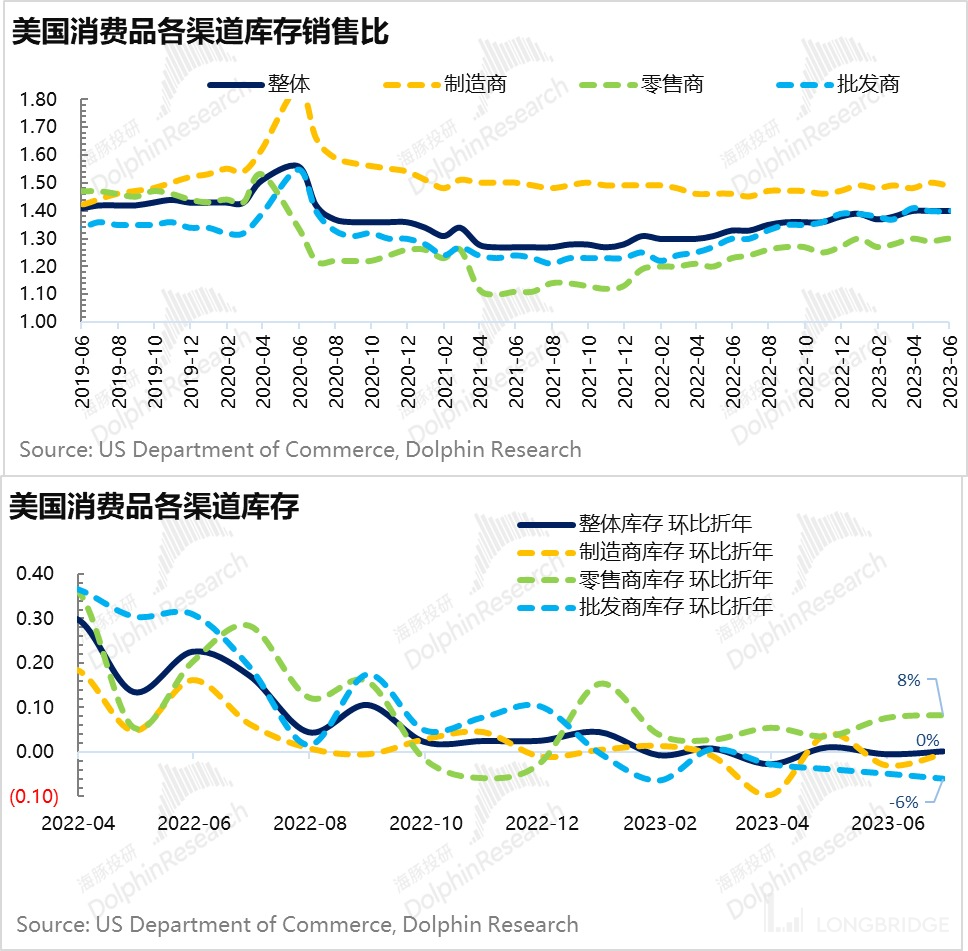

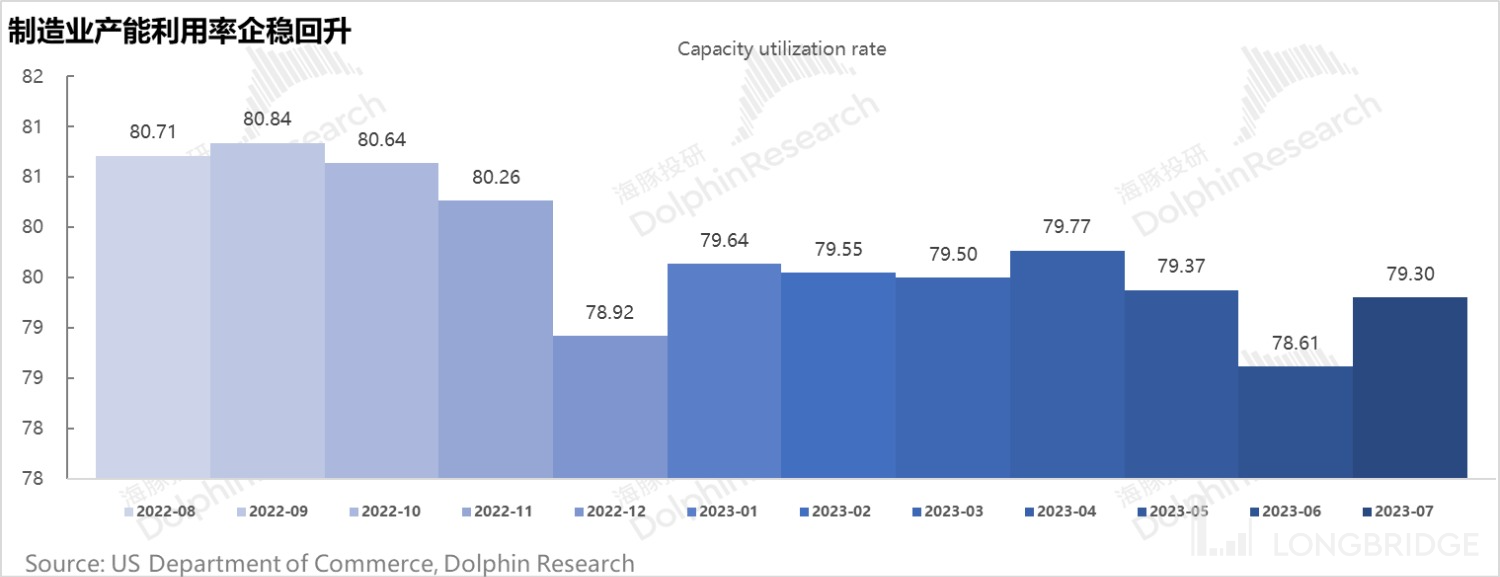

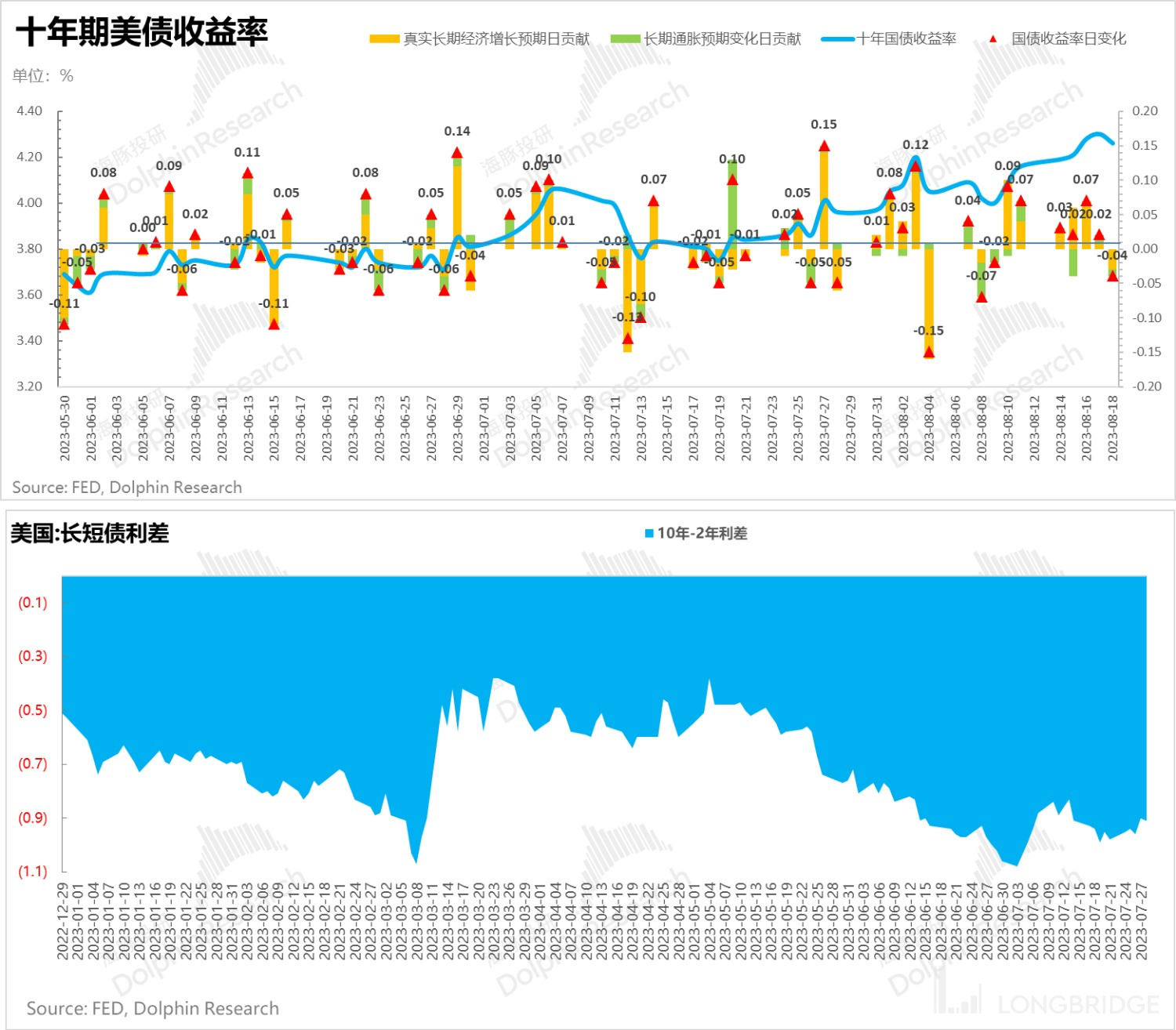

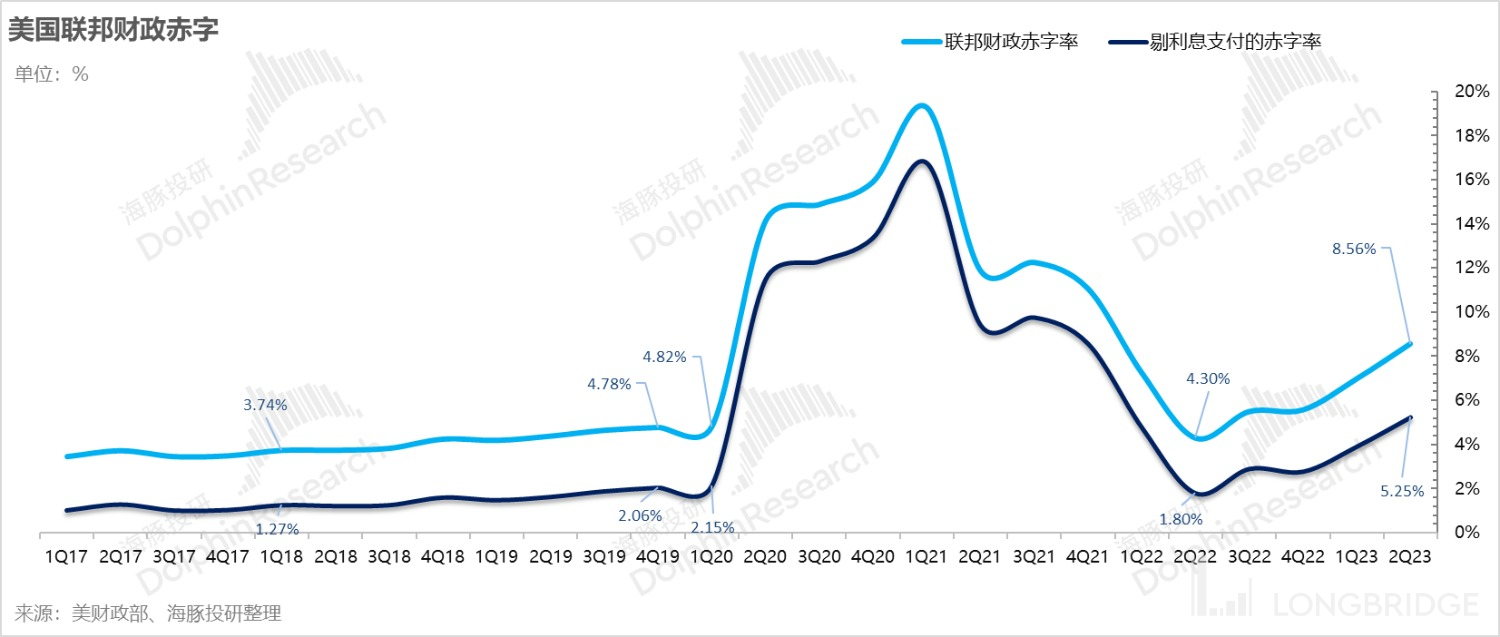

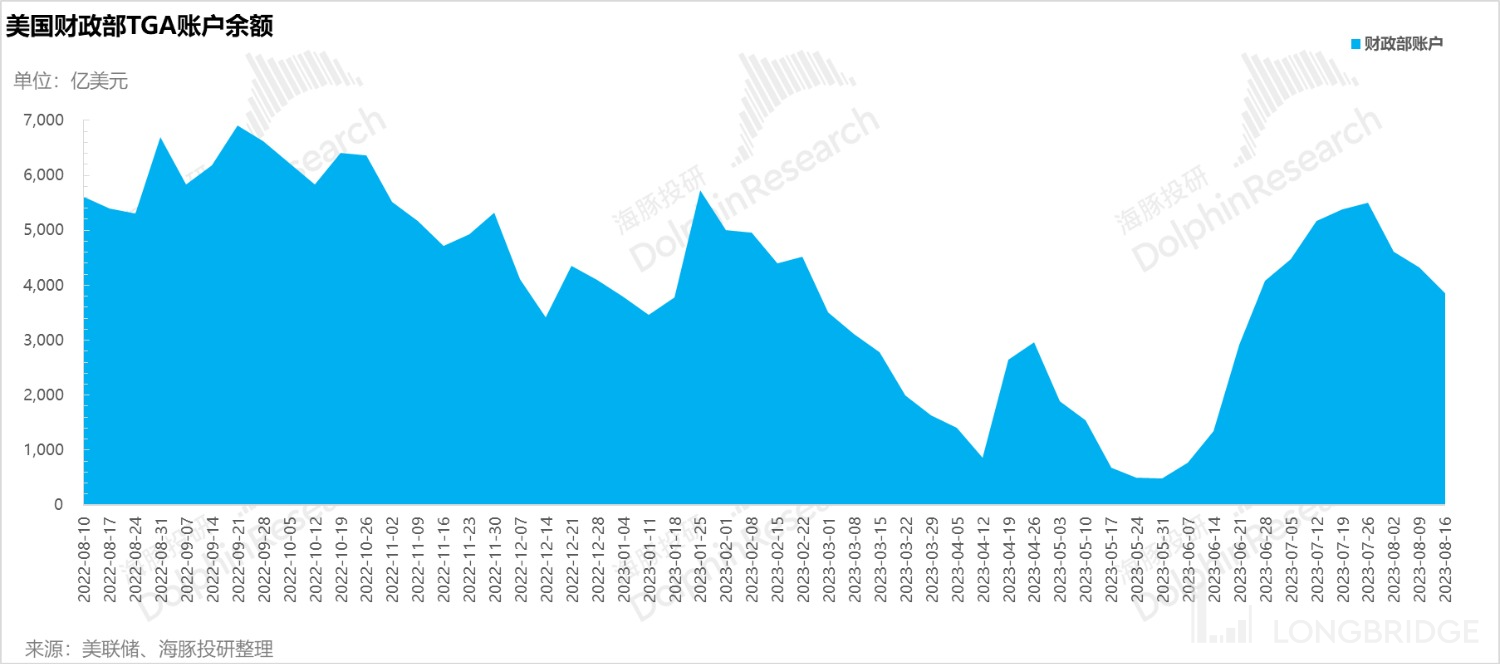

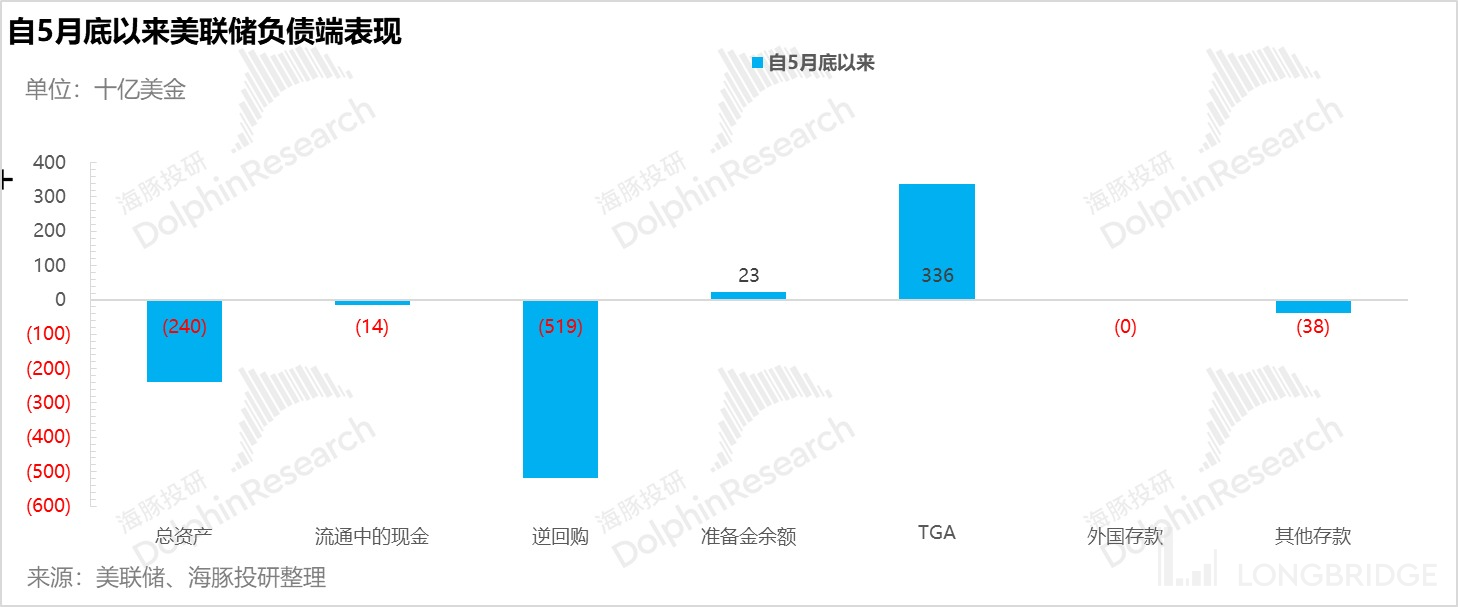

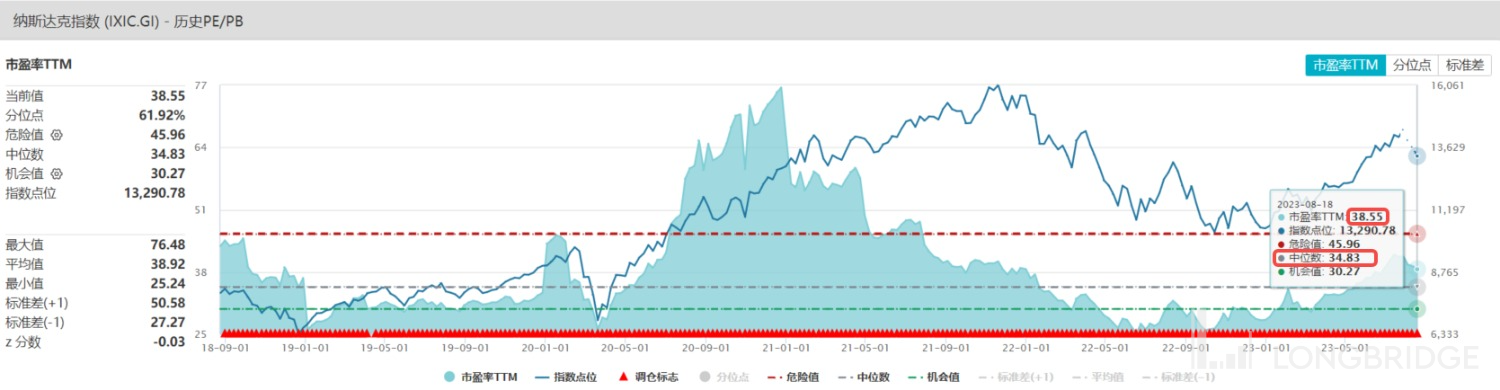

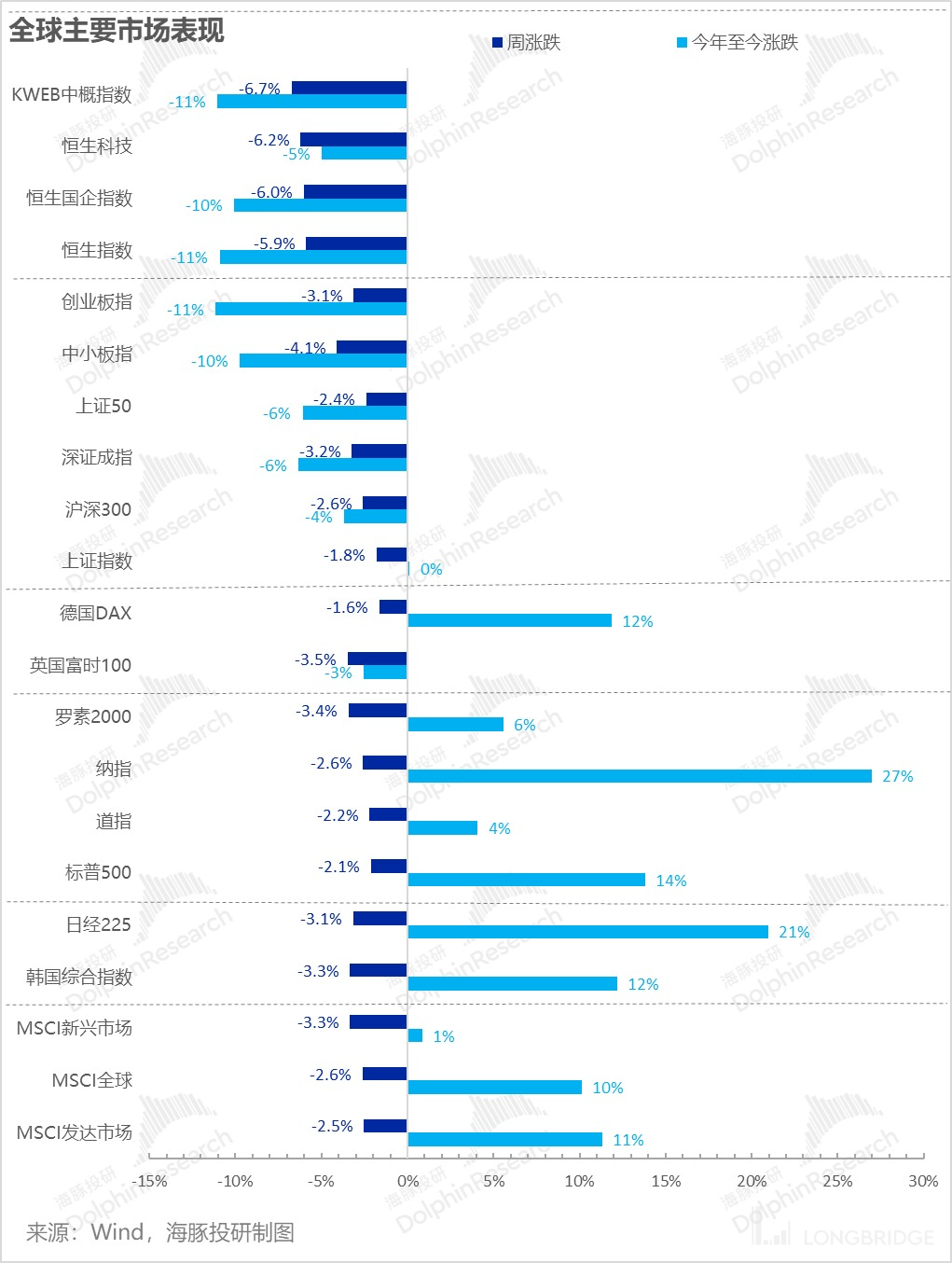

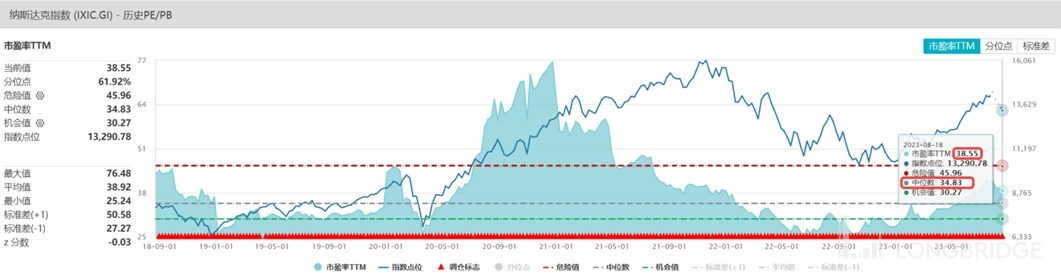

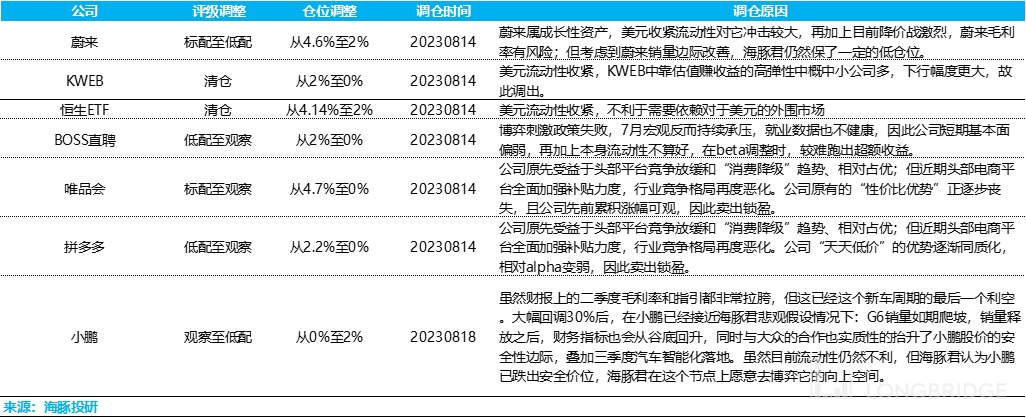

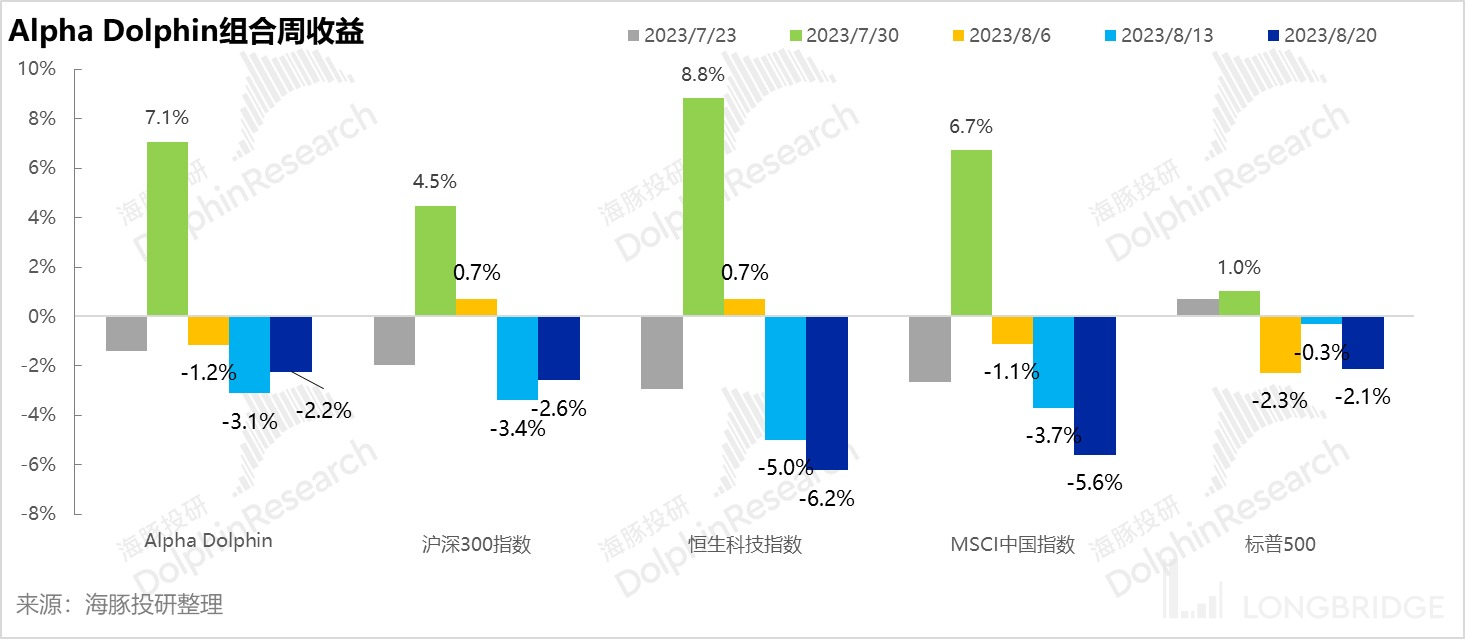

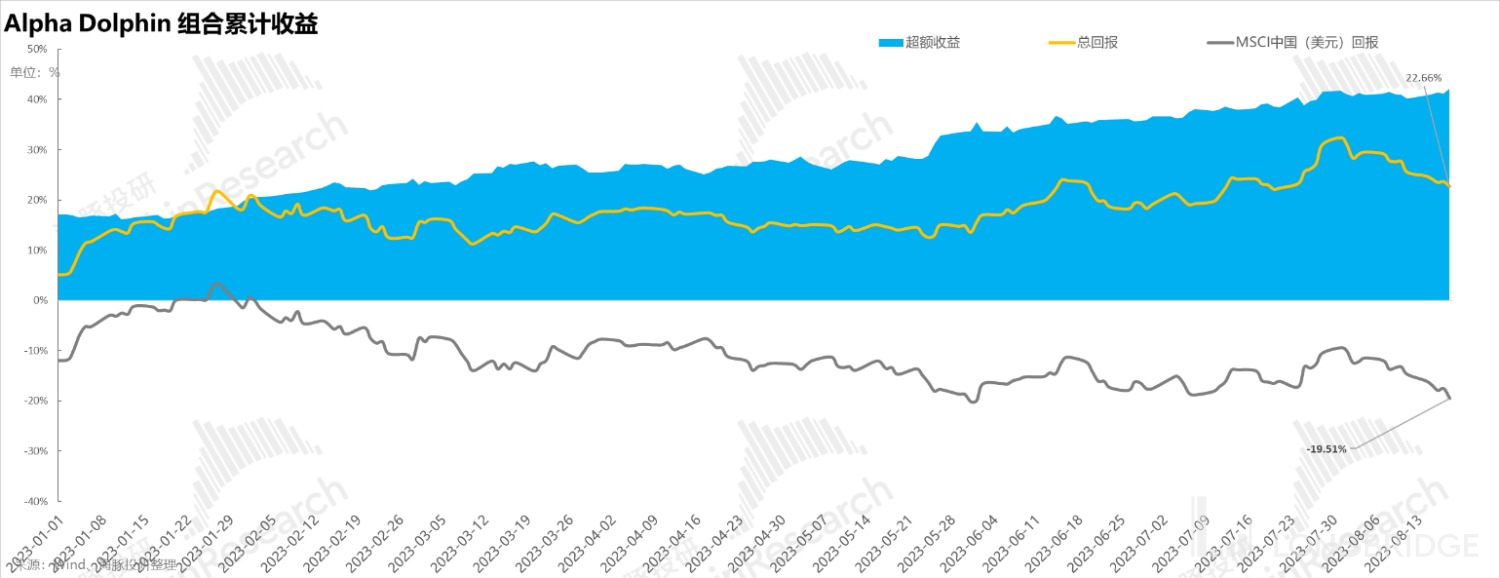

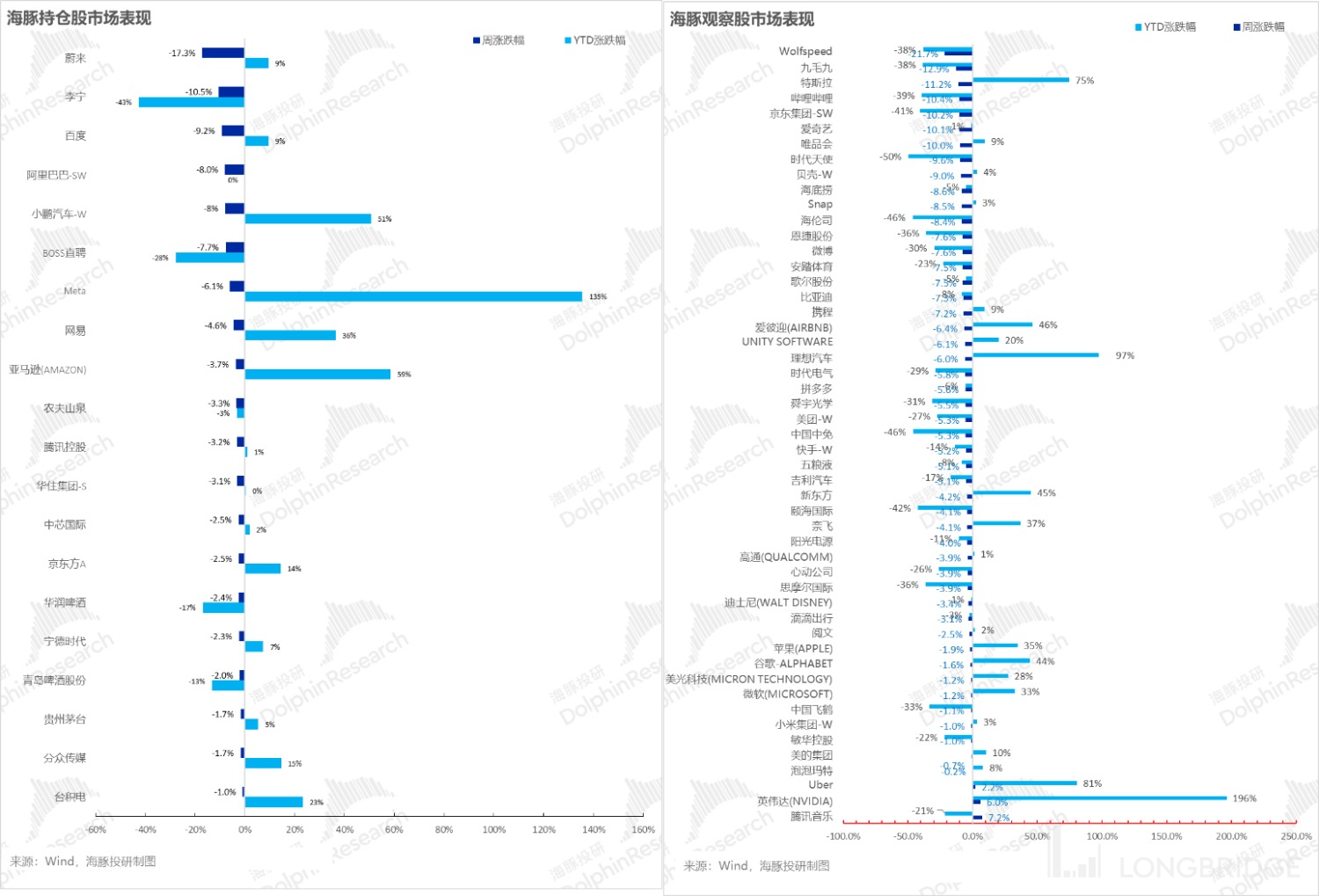

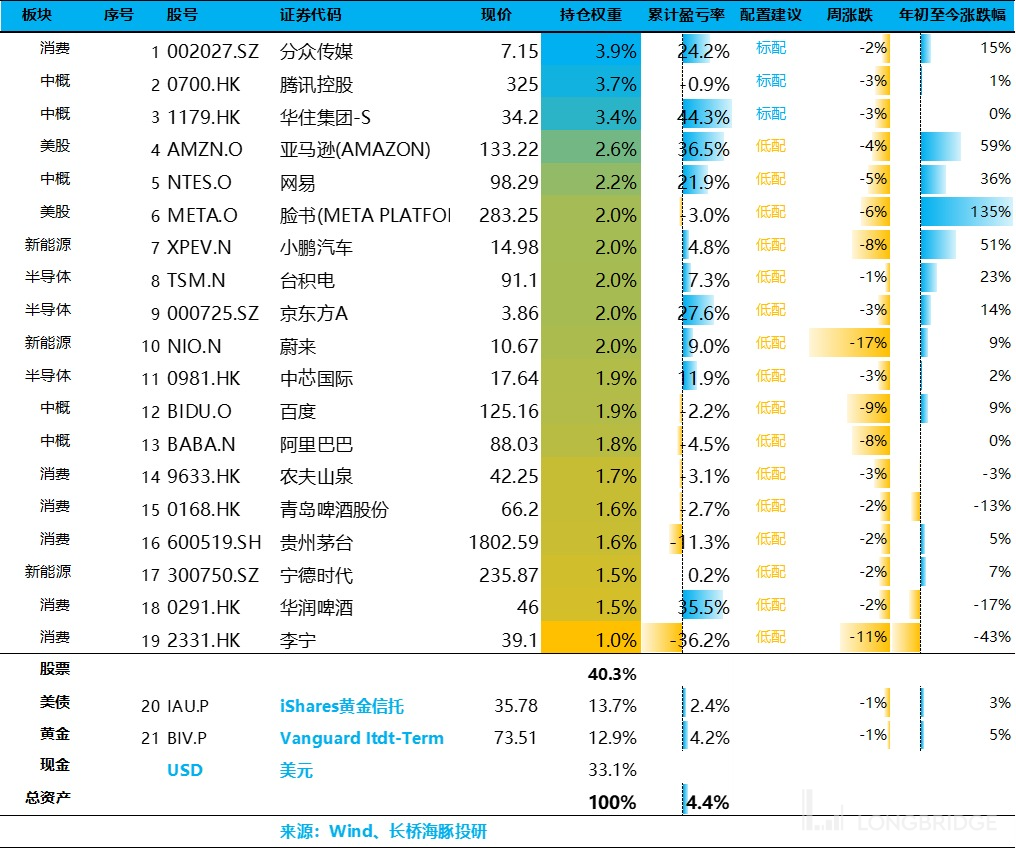

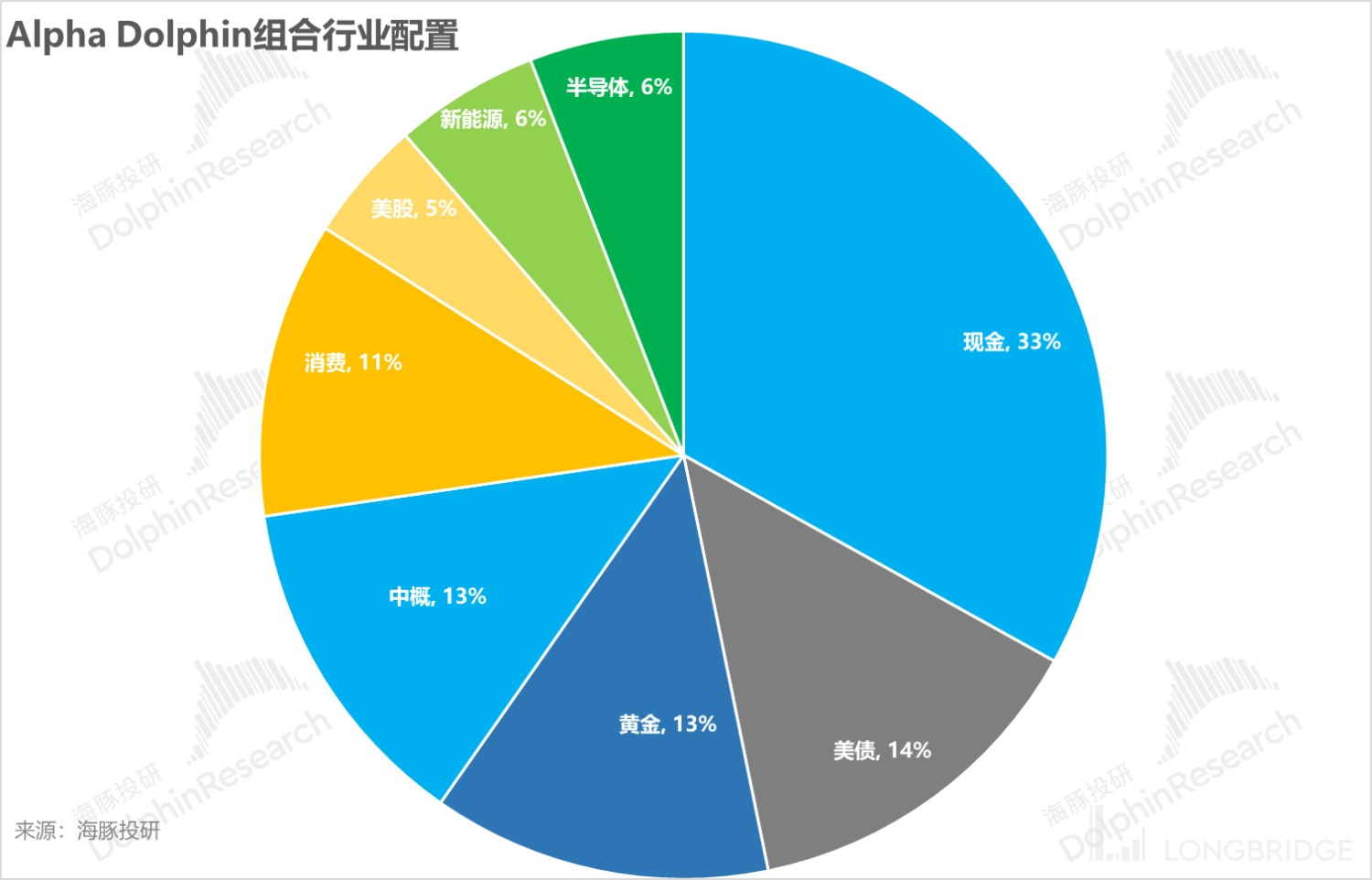

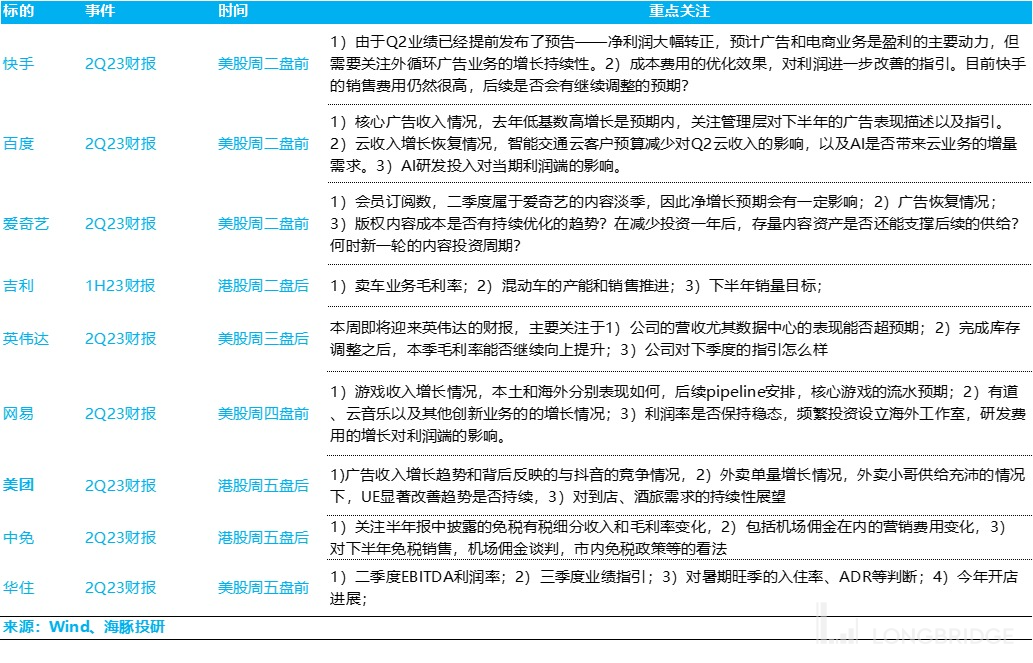

Hello everyone, the following is the core information of this week's portfolio strategy summarized by Dolphin Jun this week: 1) From the economic fundamentals, the United States is still in the perfect combination period: inflation is down, consumption is still, and last week's U.S. social zero data once again confirmed this situation. After the July quarter adjustment of the U.S. society zero discount year-on-year as high as 9%, the previous weaker must-have, optional have returned to significant positive growth, including building materials, clothing, sports hobbies and other options, but also video medical and daily necessities and other must-have. Last month's relative weakness was mainly in automobiles and parts, furniture and home appliances. * * 2)* * But the bursting social zero did not support the stock market. Last week, not only the United States, but also the global capital market were plummeting. The reason behind this, according to Dolphin Jun, is that the liquidity expectation in the second half of the year has changed significantly-the macro policy combination in the first half of the year is tight currency and consumes the broad finance under TGA, which may be unsustainable in the second half of the year. Under the two scenarios assumed by Dolphin Dolphin the year: A) Continue to maintain or even increase the deficit + rebuild the TGA balance: the subsequent borrowing efforts may be further widened, and after rebalancing the issuance of long and short bonds, it will only further absorb the liquidity of the real economy; B) fiscal policy will shift to tightening: this is more likely, and the borrowing intensity may no longer exceed expectations, but in this case, the cash balance will still be rebuilt, resulting in liquidity being sucked up. But fiscal tightening will have an impact on the real economy, and it is possible that economic fundamentals will go down. * * 3) Whether the US dollar liquidity is sucked up under the condition of higher-than-expected borrowing, or the US fiscal tightening, it is very unfavorable to the current equity market, and the decline of external dependence on US dollar funds will be especially tragic, such as Hong Kong stocks; Based on this, Dolphin Jun significantly lowered the position of Chinese assets after lowering the position of AI shares in US stocks before, and closely observed the subsequent safety margin. Here are the details: 1. U.S. economy: still in perfect mix **July, while inflation is down, it seems that consumption is still hot. In the United States, social retail (after seasonal adjustment), which is dominated by commodity retail, ushered in the largest month-on-month increase (0.73 per cent, corresponding to a year-on-year discount of over 9 per cent) in July, far exceeding the normal growth rate of about 0.2-0.4 per cent. In terms of breakdown, in addition to the continued high growth in food and beverage and online retail, **last month's weaker mandatory and optional options returned to significant positive growth, including building materials, apparel, sports hobbies and other options, as well as video medical and daily necessities. Last month's relative weakness was mainly in automobiles and parts, furniture and home appliances. * *! Judging from the inventory level of consumer goods as of June, a) retailers' inventory has already passed the stage of active inventory removal, B) the month-on-month growth rate of manufacturers' inventory has changed from negative to positive, coupled with the increase in manufacturing capacity utilization rate, which indicates that manufacturers' active inventory removal is also nearing the end. At present, the inventory removal is mainly from social channels in the intermediate links.! ! or if the cooling of commodity consumption continues to be slow, then the inventory downward cycle around manufacturing and commodity consumption has come to an end, and after the end, the pressure of this wave of commodity cycle will also weaken a lot (the corresponding commodity CPI inflation may also bottom out), but after the inventory bottoms out, the strength of the repair still depends on the strength of the overall social consumption power. Judging from the economic data as of July, the US economy is still on the principle of "soft landing. 2. the economy is strong, why the market face? The economy is not out of the question, why the stock debt double kill, only the dollar alone? The appearance is that the U.S. Treasury to increase the supply of long bonds, U.S. long bond yields continue to rise, term spreads continue to narrow, from the two-year U.S. bond yields to pick up the upward trend is expected to raise interest rates again.! But the real reason behind it, Dolphin Jun, on the other hand, is that increased debt issuance + changes in the structure of borrowing (from short to long bonds) have led to liquidity being sucked out of the real economy, and that the room for fiscal easing in the United States may have been limited after increased debt issuance. 1) The Fed began formally tapering in June last year, and U.S. fiscal policy was in sync with the Fed by the end of last year-tight money, tight fiscal. But from the beginning of this year, the U.S. fiscal deficit rate bottomed out and began to shift significantly to easing, especially in the second quarter, even excluding the increasing pressure on interest payments, the deficit rate directly related to fiscal inputs has reached 5% +, almost twice as much as before the epidemic. It can be imagined that the money may have entered the hands of residents through enterprises, and has been spent by residents, or bought stocks.! The fiscal money keeps being spent, so where does the deficit money come from? 1) Due to the limited issuance of new debt on the debt ceiling in the first half of the year, the money spent by the Treasury in various forms and the resulting deficit needs to be paid out of its own pocket, which is the fiscal deposit (account opened at the Federal Reserve-account name TGA "Treasury General Account"). The money was originally in the central bank and had no money multiplier effect, but was spent in the form of deficits, amplifying the money multiplier effect.! 2) In normal years, the balance of TGA account should be kept above a certain amount to ensure smooth payment of various expenditures. However, in the first half of the year, as the financial ceiling was not resolved, the U.S. Treasury Department, in addition to relying on income to maintain expenditure, spent extra money (deficit), as long as it relied on its own pocket, resulting in TGA running out by the end of the first half of the year. At the end of the first half of the year, after the U.S. debt ceiling issue was resolved, the Treasury Department replenished the TGA account, which, according to reason, will have liquidity pumping, and it should be noted that the money borrowed in the first half of the year was mainly short-term debt issuance. As can be seen from the liability side of the Fed's balance sheet, the reverse repo on the liability side of the Fed's balance sheet reconstruction process has fallen sharply since early June, which is equivalent to the Fed constantly returning the money it borrowed from banks to banks, and because of the favorable spread between reverse repo and short bonds, banks can easily use the money to buy short bonds. That is to say, in the process of rebuilding the statement with short bonds, a) the big buyer, the Federal Reserve, will not sell or buy; 2) Finance is equivalent to financing the fiscal deficit with overnight reverse repurchase funds, and the money originally in the primary market is also less effective than the money multiplier effect of the deficit. 3) Short-term debt to rebuild TGA balance draws relatively little water from the real economy. After turning to long bond financing; A) the original big buyer, the Federal Reserve, is not not selling or not selling, but the main seller; 2) When the Ministry of Finance looks for money from the market, due to the high cost of interest rate inversion and overnight reverse repurchase funds, and the need for long bonds to match funds with longer maturities to buy these treasury bonds; That is to say, when long bonds are issued, the sucking effect of TGA reconstruction on the real economy's funds is really beginning.! 3) And for another question-whether the fiscal deficit rate will continue to widen: in the first two quarters of the first half of this year, the U.S. GDP growth rate is basically above 2%, but the U.S. fiscal or with loose monetary policy, **or pro-cyclical period" rare "with counter-cyclical policy. * * * * (As the above logical chain is relatively difficult to understand, Dolphin King will give a more detailed interpretation later, please pay attention.) * * * * Next, there are two reasonable scenarios: * * **a) Continue to maintain or even increase the deficit: * * Because the deficit causes the US TGA account to be consumed while rebuilding, the Ministry of Finance is forced to increase the supply of long-term bonds with slightly lower interest costs; However, this time the Ministry of Finance has said that the TGA balance will be filled to US $650 billion by the end of September and US $750 billion by the end of December, which is currently less than US $400 billion. In order to increase the deficit and rebuild the cash balance, the subsequent borrowing efforts may be further widened. After rebalancing the issuance of long and short bonds, it will only further absorb the liquidity of the real economy. * * B) Fiscal Tightening Transfer: * * Dolphin Jun tends to think that this is more likely, especially considering the use of counter-cyclical stimulus policies in the pro-cyclical period. If the economy turns downward due to interest rate hikes, the deficit rate would have been passively raised, and there is much room for fiscal easing. In this case, the main reason is that rebuilding cash balances will suck liquidity and borrowing may no longer exceed expectations. However, fiscal tightening will have an impact on the real economy, and it may be that the fundamentals of the economy are downward. And whether the borrowing strength of the dollar liquidity is sucked, or the U.S. fiscal turn to tightening, are very detrimental to the current equity market, and the peripheral dependence on the decline in dollar funds will be particularly tragic, such as Hong Kong stocks. And looking at the current overall Nasdaq valuation score, which is still above 60% of the past five years, there is still a risk of killing valuations under the liquidity water. In the period of killing valuation, the fundamentals are relatively flat, and companies that are mainly pulled up by stories will be killed more.! 3. market trading trend also because of the Treasury TGA account reconstruction process of liquidity pumping expectations, last week the global equity market can be described as a plunge, the general decline is around 3%, the more small tickets, the more growth, the more the peripheral dollar market, the greater the decline. In this case, in addition to the dollar, the other regardless of the valuation will be killed.! After this wave of liquidity pumping, Dolphin Jun believes that the valuation of the oversold plate is more likely to fall out of the medium-and long-term margin of safety, many companies that can only hope and sigh will also appear "grounded" prices, Dolphin Jun will continue to pay attention to the opportunity of oversold in the process of decline.! 4. portfolio transfer is also based on the above logic, Dolphin Jun significantly lowered the general asset position, liquidated Dolphin Jun believes that the fundamentals may be marginal downward company, the Dolphin Jun believes that there is a chance of the company only do low position configuration. Specific adjustments are as follows:! * * 5. Portfolio Income * * In the week of August 18, Alpha Dolphin virtual portfolio income fell 2.2 percent, basically in line with the S & P 500 Index (-2.1 percent), better than MSCI China Index (-5.6 percent), Shanghai and Shenzhen 300(-2.6 percent) and Hang Seng Technology Index (-6.2 percent).! Since the portfolio began testing to the end of last week, the absolute return of the portfolio was 23%, and the excess return compared to MSCI China was 42%. From the perspective of net asset value, Dolphin Jun's initial virtual asset is 0.1 billion US dollars, currently 0.124 billion US dollars.! 6. individual stock profit and loss contribution Last week global assets were generally killed, and the Dolphin Jun ticket pool also basically did not rise, just the difference between large and small declines. Companies with high valuations or fundamental deviations have fallen more.! For the companies with the highest rise and fall, Dolphin King sorted out the reasons as follows:! 7. Portfolio Asset Distribution After this week's portfolio transfer, 21 stocks were allocated, of which 3 were rated as standard, 16 were low, and the rest were gold, U.S. debt and U.S. dollar cash. As of the end of last week, Alpha's Dolphin asset allocation allocation and equity asset position weights were as follows:! ! 8. Key Events of the Week: The mid-week earnings report continues, with a focus on Nvidia, Meituan, Netease and Baidu. Specific concerns Dolphin Jun is organized as follows, when you can pay attention to Dolphin Jun's first financial interpretation.! * * risk disclosure and statement of this article: * * * * dolphin investment research disclaimer and general disclosure * * please refer to the recent article of dolphin investment research portfolio weekly: is there any redemption for Hong Kong stocks Fitch is just a "paper tiger", there is still hope in China after the violent rebound, is Hong Kong stock going or staying? " U.S. Interest Rate Hike to Top, Hong Kong Stocks Saved?" How far can China rebound when reality strikes? " Look further, will US interest rate hikes add to stagflation?" Decoding the Mystery of Low U.S. Savings, Is It Sustainable? " The U.S. Housing Market: Subprime Original Sin, Why Resist This Time?" "cocooning: where did the recession go and can it still come?" "Small composition about the market? Extreme pessimism followed by overcorrection is the core" U.S. stock orgy? Economic Scores, Beware of Passion Purgatory vs Carnival, What Are US and Hong Kong Stocks Trading? " U.S. Stocks Pull Valuation, Hong Kong Stocks Kill Beta? Don't despair, a reversal is imminent" High interest rates put in a bank again? On the contrary, the chances of a soft landing are higher "ChatGPT vs performance release list, can giant Zha push hold up US stocks?" Does the good "US recession, China recovery" have to be ruined? "U.S. Recession Direction Set, Just Small Decline, Big Decline" U.S. Service Consumption Collapses, U.S. Stocks Celebrate? "" Fed rate cut: just one short of a U.S. version of the balance sneak attack moment? " U.S. stocks to recession, to cut interest rates? Anyway, the deal is already in place" Silicon Valley Bank Run Crisis: Is the U.S. Recession Going to Run? "[U.S. Stocks Spit Back to End Trading Rush, Global Can Finally Breathe](https://longbridgeapp.com/topics/4355034?App_id = longbridge & channel = t4355034 & invite-code = 276530) Inflation Head Up Real Hammer? It is an opportunity to turn away from Thailand "Inflation aside, signals from Ali and Baidu are more important" "Hong Kong, America, Qi Qi Weak Chicken, Wolf Coming Again?" High-frequency macro marionettes, U.S. stocks are puppet cities "" A positive line changes faith, Tesla led U.S. stocks to kill back? "How far is the" crisis "and" opportunity "of US stocks" US stocks are not red for the New Year, but the performance hammer is just around the corner? "Grabbing the Roots of Stagflation in U.S. Stocks" CPI Has Falling, Why Is the Fed Still on This Axis? " Is service inflation really that easy to eliminate? Beware of market overkill Hong Kong stocks finally have a" waist? The independent market can go a while " " The Darkness Before Dawn: Mentality Refocuses on Darkness or Dawn "" U.S. stocks "beat back" reality, how long can emerging markets jump? "Global Xiti Valuation Repair? And the performance test" "China's asset violence pulls up, why China and the United States glacial two days" "Amazon, Google, Microsoft superstars fall? U.S. stocks" meteor shower "still have to go down" "Behind the policy shift expectations: unsecured" strong dollar "GDP growth?" "South to take over vs. North to go crazy, it's time to test" concentration "again" "Slow down and raise interest rates? Dream Shattered Again" Re-understanding an "Iron and Blood" Federal Reserve "" Tragic Second Quarter: "Eagle Voice" Loud, Collective Difficulties "" Falling to Doubt Life, Is There Any Hope of Reversing the Length of Despair? "" Fed Violently Hammers Inflation, Domestic Consumption Opportunities Instead? "The world has plummeted again, and the lack of people in the United States is the root cause of the disease" The Federal Reserve has become the number one short seller, the global market has fallen to its knees A bloody case triggered by a rumor: the risk has never been clear, and sugar is found in the glass slag The United States goes left, China goes right, the price/performance ratio of U.S. assets is back "layoffs are too slow to take over, the U.S. has to continue to" decline " U.S. stock-style" funeral ": recession is a good thing, the strongest interest rate hike is called" bad news " " interest rate hike enters the second half, "performance thunder" opens " 《 Contagion to fight back, U.S. to recession, money to change mind Chinese assets right now: U.S. stocks "no news is good news" Growth is already a binge, but is the U.S. necessarily a recession? " " Is the United States in 2023 a recession or stagflation? " U.S. Oil Inflation, China's New Energy Vehicles Bigger and Stronger?" "Fed raises interest rates faster, Chinese asset opportunities come instead" U.S. stock inflation has exploded again, how far can a good rebound go? " This is the most grounded gas, the dolphin portfolio has run away

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.