Don't panic! The bottom of Chinese concept stocks may have arrived.

Hello everyone, here is the summary of this week's core information on Dolphin Research's portfolio strategy:

-

Last week, amid a global market decline, Chinese assets did not escape the downturn and experienced even larger declines. From the triggering factors, whether it is weak exports or a significant depreciation of the renminbi exchange rate, Dolphin Research believes that these factors are already in a marginal state that is difficult to worsen.

-

The decline in the renminbi exchange rate last week was mainly due to the strength of the US dollar. The underlying reason behind the strength of the US dollar is the weakness of local currencies in non-US regions caused by weak economic data. In contrast, the renminbi exchange rate index against a basket of currencies actually appreciated.

-

From a fundamental perspective, whether it is the bottoming out of export growth, the simultaneous MoM improvement of CPI and PPI, or the recovery of social retail data after the government bond issuance, coupled with the yet-to-be-reflected effects of relaxed real estate policies, the domestic economy has gradually transitioned from a policy bottom and is slowly moving towards a low economic state. It may not be easy for deflation expectations to turn into reality, and trades based on deflation expectations may gradually correct.

-

If prices continue to rise in the future and the deflationary expectations in trading during this period remain only as expectations without materializing, there is hope for a gradual recovery of Chinese assets.

The following is the detailed content:

I. Gradual Confirmation of the Bottom for Chinese Assets?

In last week's strategy weekly report, "US Unemployment Rate Rises, Hope for Chinese Assets Arises" (link: https://longportapp.com/topics/9617937?app_id=longbridge&channel=t9617937&invite-code=276530), Dolphin Research believed that Chinese assets were valued above the freezing point and had greater resilience for recovery under the easing of interest rates and substantial domestic policy support. However, the actual situation last week was a deep adjustment for Chinese assets.

The background of the correction in Chinese assets last week was the renewed decline in the renminbi exchange rate, which clearly fell below 7.3, as well as the continuous outflow of northbound funds. However, in reality, the decline in the renminbi exchange rate against the US dollar was mainly caused by the decline in other non-US currencies, and the renminbi exchange rate index against a basket of currencies actually appreciated.

The reason for the general decline in non-US currencies is that in the past week, including the bankruptcy declaration of a large local government in the UK, the economic data released by most countries has been rather disappointing.

And it's time to look at one of the most important economic data points in China in August - the prices of goods have quietly changed.

And it's time to look at one of the most important economic data points in China in August - the prices of goods have quietly changed.

In August, both CPI and PPI prices in China showed a month-on-month increase. In terms of CPI, apart from the inflationary pressure caused by poultry and other food prices rebounding, housing and medical prices have also shown a marginal recovery, while transportation and communication prices have continued to rise due to increased fuel costs. However, the growth rate of education, culture, and entertainment prices has slowed down due to a slowdown in tourism-related price increases.

Currently, the prices of clothing and household appliances are still declining on a month-on-month basis, while PPI has stabilized. There are signs of a bottoming out and a rebound in domestic prices. It is not easy for deflation to transition from expected to actual transactions.

In addition, looking at the latest import and export data, US dollar-denominated exports in August fell by 8.8%, which is within expectations. Moreover, from the trend perspective, it is already in a recovery trend.

Furthermore, the most important thing is that the recently released social financing data (the effect of real estate stimulus has not yet been reflected) seems to indicate that the bottom of China's credit has already formed:

With the government's efforts in project implementation, social financing has finally shown a slight recovery, reaching a monthly increase of over 3 trillion yuan. However, RMB loans have not yet returned to a net increase state. Of course, the structure of RMB loans in August is still a long-standing issue, with a significant decrease in long-term loans and relatively weak long-term loans for individuals. However, considering the series of demand-side loosening policies recently introduced and the upcoming peak season for real estate sales, social financing data is expected to continue to rise.

In fact, from the above-mentioned price and social financing data, it can be seen that the deflation expectations that have been persistently traded in the market for some time may be difficult to materialize if prices continue to rise.

Looking at the current 10-year treasury bond yield hovering around the historical long-term bottom of 2.6% (the last time was during the global outbreak of the pandemic in April 2020, and before that was around 2016), compared with the current price of government bonds, it can be said that Chinese equity assets are highly cost-effective. Moreover, from the perspective of PE percentile, the entire Hang Seng Index is still at a historically low level over the past five years, indicating visible valuation attractiveness. Also, therefore, although Chinese concept assets performed poorly last week, Dolphin Research believes that the sell-off of Chinese assets based on the weakness of non-US currencies in the periphery is not reasonable. It still sees the resilience of Chinese concept assets during this period and believes that the crazy inflow of funds from the south in the past two weeks is reasonable.

2. Portfolio Returns

On August 28th, Alpha Dolphin's virtual portfolio returns declined by 2.1%, which is basically in line with the Hang Seng Technology Index, but significantly lower than the CSI 300 (-1.4%), MSCI China Index (-1.2%), and S&P 500 Index (-1.2%).

Since the start of the portfolio testing until last weekend, the absolute return of the portfolio is 24%, and the excess return compared to MSCI China is 42%. From the perspective of asset net value, Dolphin Research's initial virtual assets were $100 million, and currently it is $126 million.

3. Contribution of Individual Stocks' Profits and Losses

Last week, under the strong US dollar, global assets experienced a general decline. Among the companies covered by Dolphin Research, there are two types of assets with significant declines. One type is high-quality assets with reasonable valuations, such as Ctrip and Pinduoduo. The other type is small companies with growth potential, such as Beike, NIO, iQiyi, and Bilibili, which exhibit a typical "kill valuation" decline.

Specifically, the companies with the highest increase and decrease in stock prices are summarized by Dolphin Research as follows:

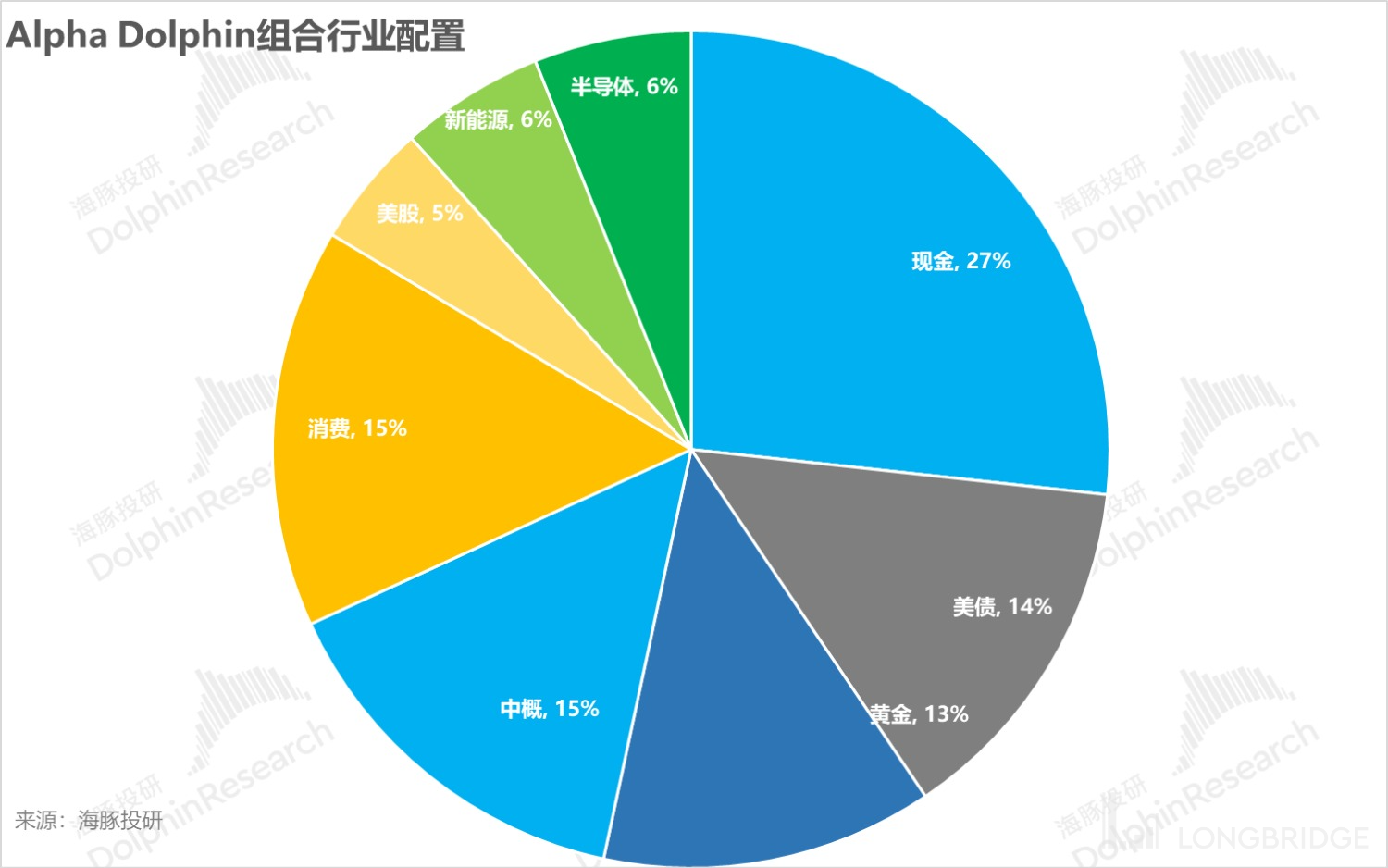

4. Portfolio Asset Allocation

After the portfolio was adjusted this week, it is allocated to 22 stocks, including 3 stocks with standard ratings and 19 stocks with low ratings. The rest are allocated to gold, US bonds, and US dollars.

As of last weekend, Alpha Dolphin's asset allocation and equity asset holding weights are as follows:

!

!

{kind=link}

Risk Disclosure and Statement of this Article: Dolphin Research Disclaimer and General Disclosure

Please refer to the recent Dolphin Research portfolio weekly reports:

"US Unemployment Rate Rises, Hope for Chinese Concept Stocks"

"Inflation vs. Drainage, Tough Times Ahead in the Second Half of the Year"

"Is the US Government Spending Money Like Water? The Backlash Has Arrived"

"Is There Still Redemption for Hong Kong Stocks?"

"Fitch Ratings is Just a 'Paper Tiger', Chinese Concept Stocks Still Have Hope"

"After the Violent Rebound, Should We Stay or Leave Hong Kong Stocks?"

"Has the US Reached the Peak of Interest Rate Hikes? Is There Hope for Hong Kong Stocks?" 《Reality Strikes, How Far Can the Rebound of Chinese Stocks Go?》

《Look Further, Will US Rate Hikes Aggravate Stagflation?》

《Decoding the Mystery of Low Savings in the US, Is It Sustainable?》

《US Housing Market: Subprime Sins, Why Is It Resilient This Time?》

《Unraveling the Recession: Where Did It Go and Can It Come Again?》

《Micro Essays Influence the Market? Extreme Pessimism Leads to Overcorrection》

《Endless Celebration in US Stocks? Economic Schizophrenia, Beware of Joy Turning to Sorrow》

《Inferno vs. Celebration, What Are US and Hong Kong Stocks Really Trading?》

《US Stocks Pulling Valuations, Hong Kong Stocks Killing Beta? Don't Despair, Reversal Is Imminent》

- High interest rates put into another bank? The chances of a soft landing are even greater

- ChatGPT vs. Performance release, can the giants support the US stock market?

- Is the plan of "US recession, China recovery" going to fail?

- The direction of the US recession is already determined, it's just a minor setback, but a major setback will be detrimental

- US service consumption collapses, and the US stock market celebrates?

- Fed rate cut: Is it just a matter of time before the US version of Yu'ebao strikes?

- US stocks are going to decline and interest rates are going to be cut? In any case, the trading has already taken the lead

- Silicon Valley Bank's run on deposits crisis: Is the US recession going to arrive in a hurry?

- After giving back gains from trading, global markets can finally catch their breath 《Inflation Rising: A Confirmation? Adversity Brings Opportunities》

《 Putting Inflation Aside, Signals from Alibaba and Baidu Are More Important》

《 Weak Performance in Hong Kong and the US, Is the Wolf Coming Again?》

《Macro Puppeteers: The US Stock Market as a Puppet Market》

《 A Bullish Candlestick Changes Beliefs, Can Tesla Lead the US Stock Market to a Comeback?》

《 How Far is the US Stock Market from the "Dangerous" Turning Point》

《 No Lunar New Year Rally in the US Stock Market, But Earnings Reports Are Just Around the Corner》

《 Uncovering the Root Cause of the US Stock Market's Stagnation》

《CPI Has Fallen, Why is the Fed Still So Stubborn?》

《Is Service Inflation Really That Easy to Eliminate? Beware of Market Overcorrection》

《Has the Hong Kong Stock Market Finally Found Its Backbone? Independent Trends May Continue》

《The Darkest Hour Before Dawn: Focus on the Darkness or the Dawn》 《 US stock market "hit back" with reality, can emerging markets bounce for how long?》

《Global Valuation Repair? There is also a hurdle of Performance Inspection》

《Chinese Asset Violence Boosts, Why Are China and the United States Different?》

《Policy turnaround expectations: unreliable "Strong USD funds" GDP growth?》

《Southward takeover vs. Northward crazy run, it's time to test "determination" again》

《Slow down and raise interest rates? The American dream was shattered again》

《 Reacquaint with an "Iron-blooded" Fed》

《 Sad Second Quarter: "Eagle Sound" Loud, Collective Crossing Difficulties》

《Falling into doubt about life, is there still hope for despair and reversal?》

《 The Fed's Violent Hammering of Inflation, Domestic Consumer Opportunities are Coming Instead?》 Global markets plummet again, labor shortage in the US is the root cause

The Federal Reserve becomes the number one bear, global markets collapse

A bloodbath triggered by a rumor: risks are far from eliminated, searching for sugar in broken glass

US leans left, China leans right, cost-effectiveness of US assets is back

Layoffs are too slow, the US must continue to decline

Rate hikes enter the second half, "earnings thunder" begins

Epidemic resurgence, US recession, capital reversal

Current state of Chinese assets: "No news is good news" for US stocks

Growth is already in a frenzy, but does it mean the US is definitely in recession?

The US in 2023: recession or stagnation? 《US Oil Inflation, Can China's New Energy Vehicles Grow Stronger?》

《Fed's Rate Hike Accelerates, China's Asset Opportunities Arise》

《US Stock Market Inflation Soars Again, How Far Can the Rebound Go?》

《This Is the Most Down-to-Earth, Dolphin Research Portfolio Is Launched》

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.