Another fierce battle for ByteDance, MEITUAN-W's defense is stronger than Alibaba

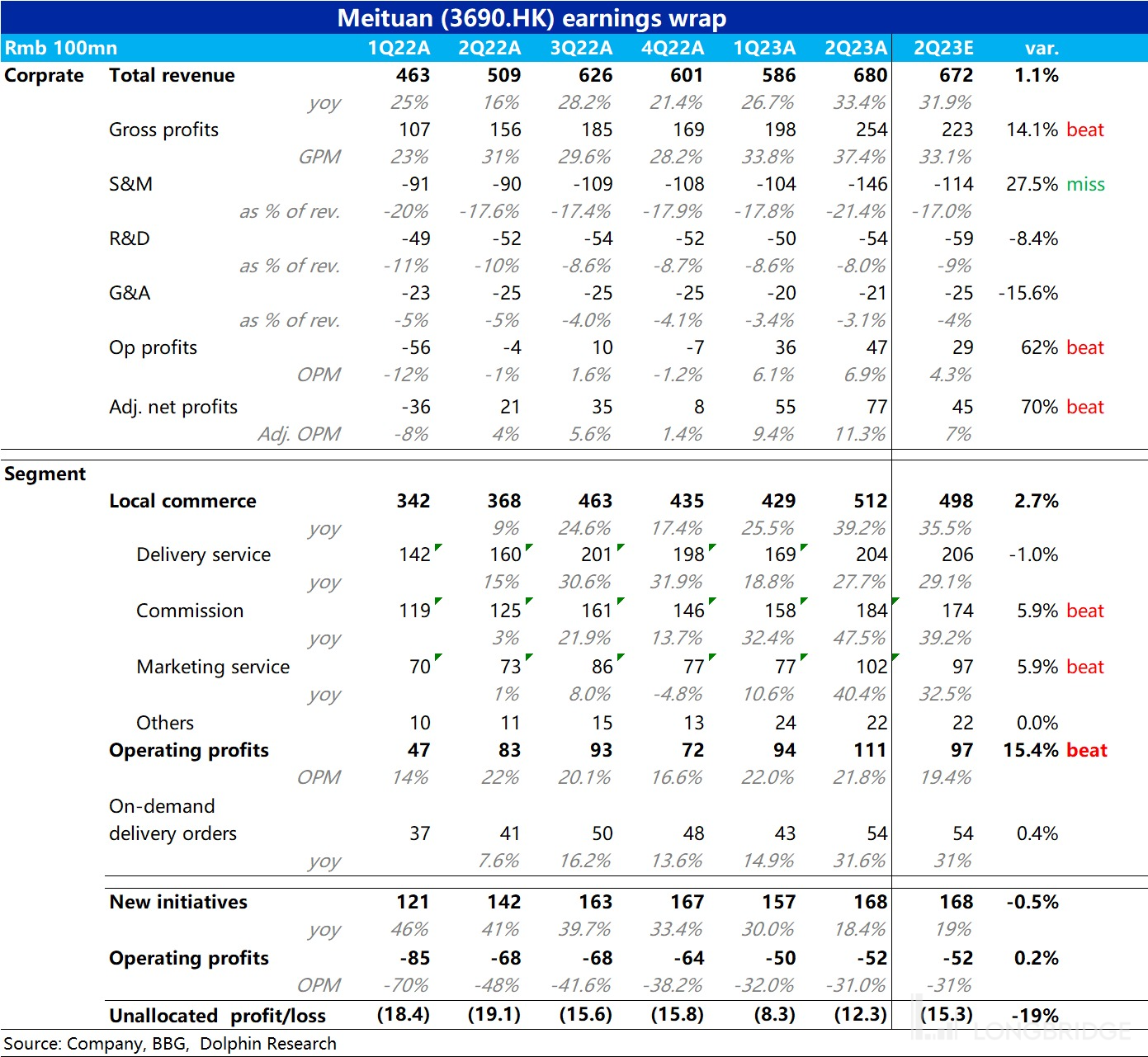

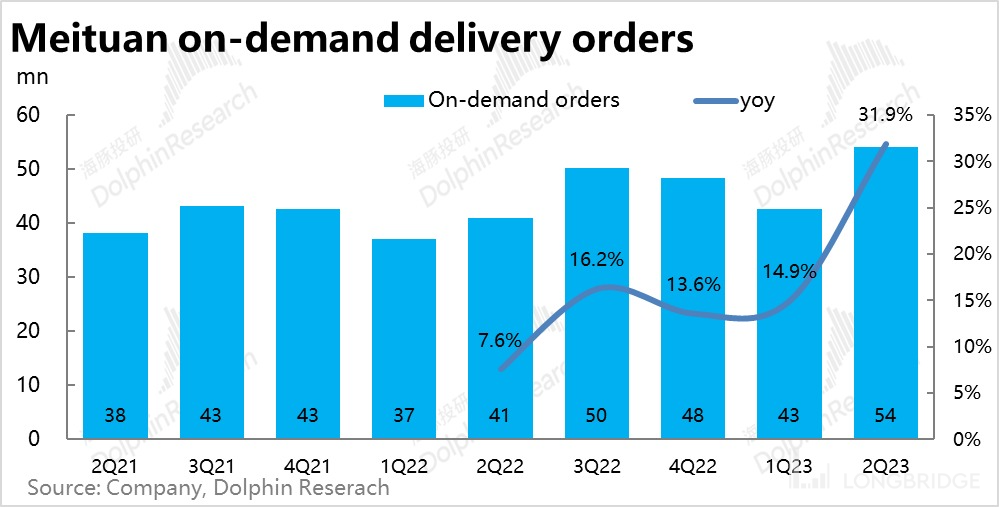

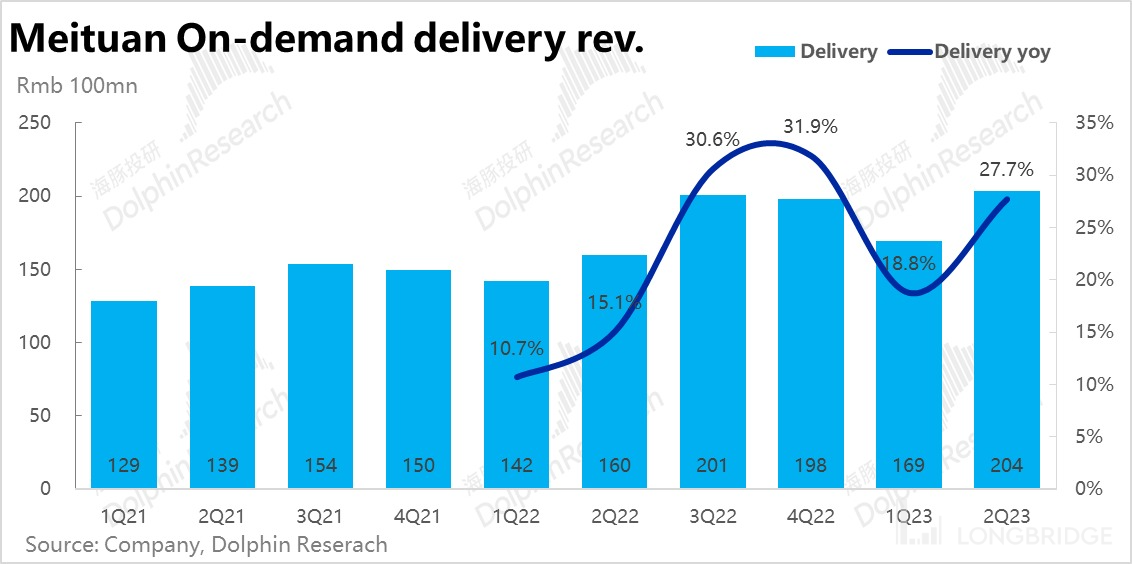

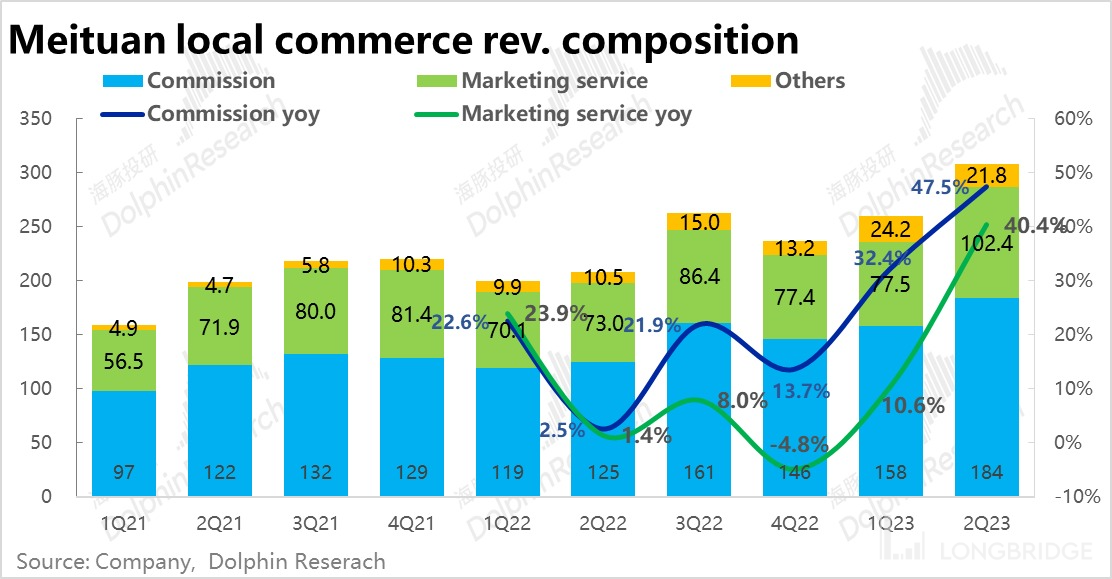

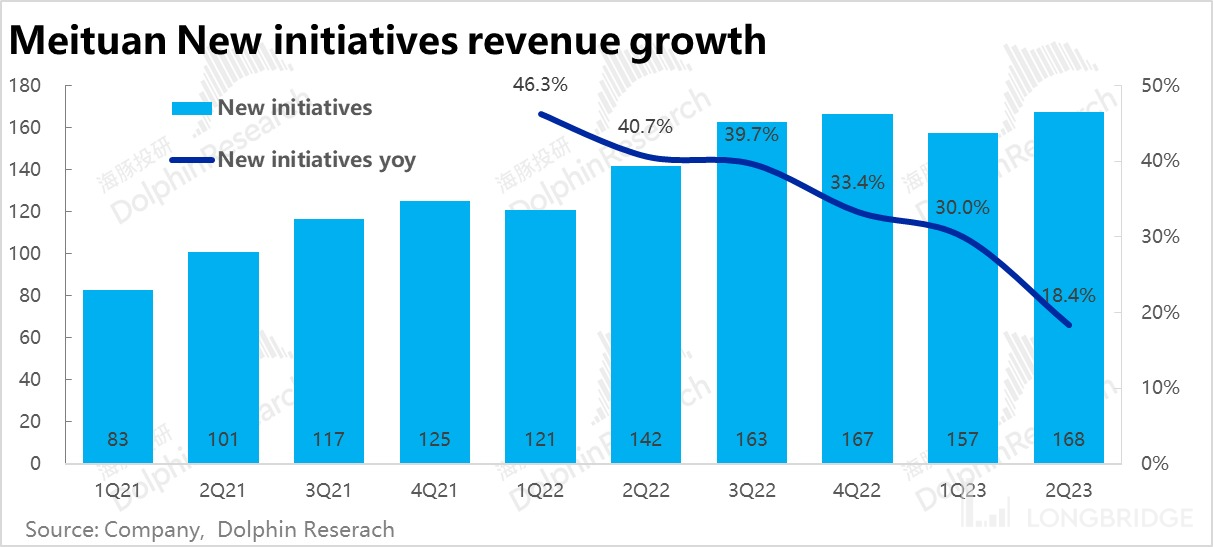

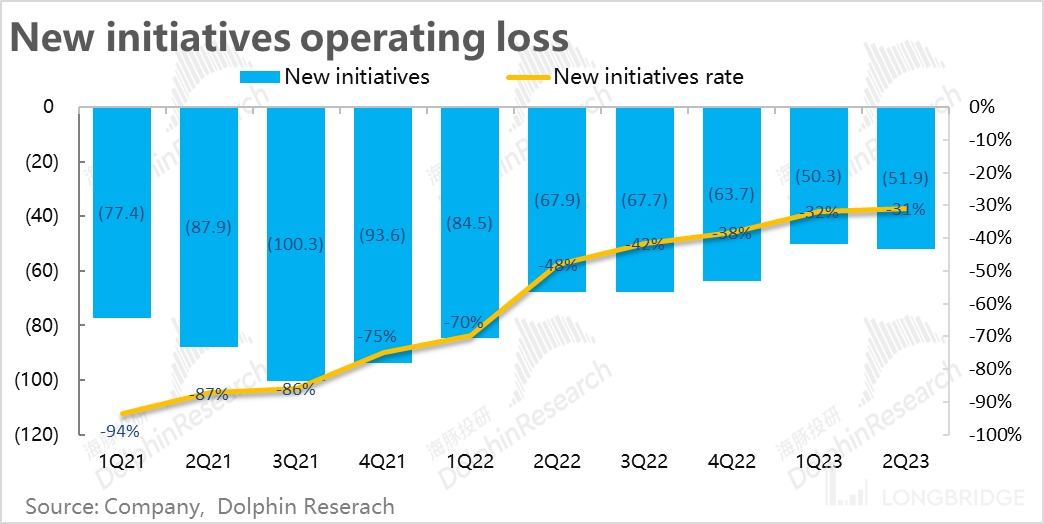

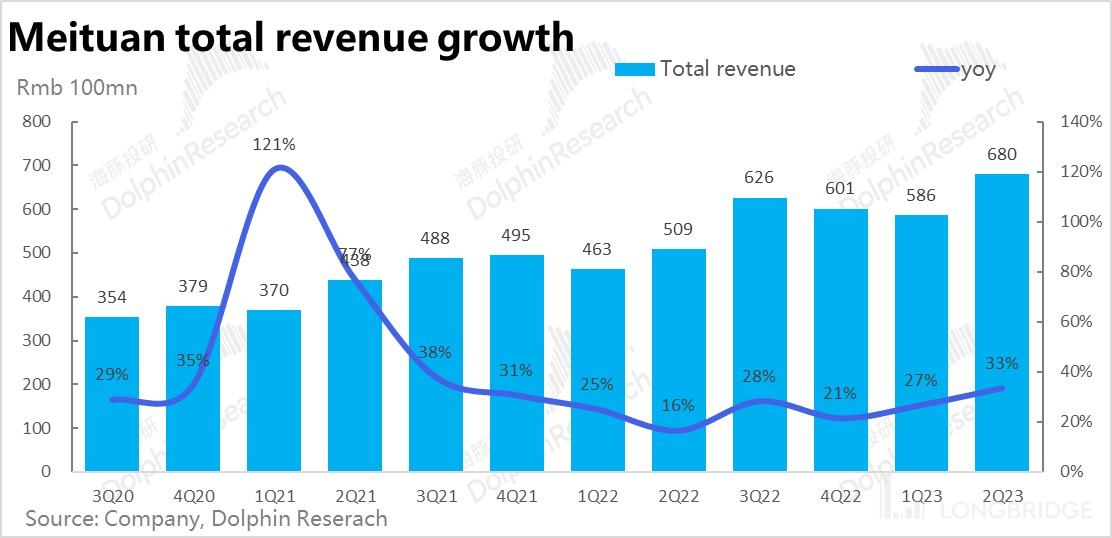

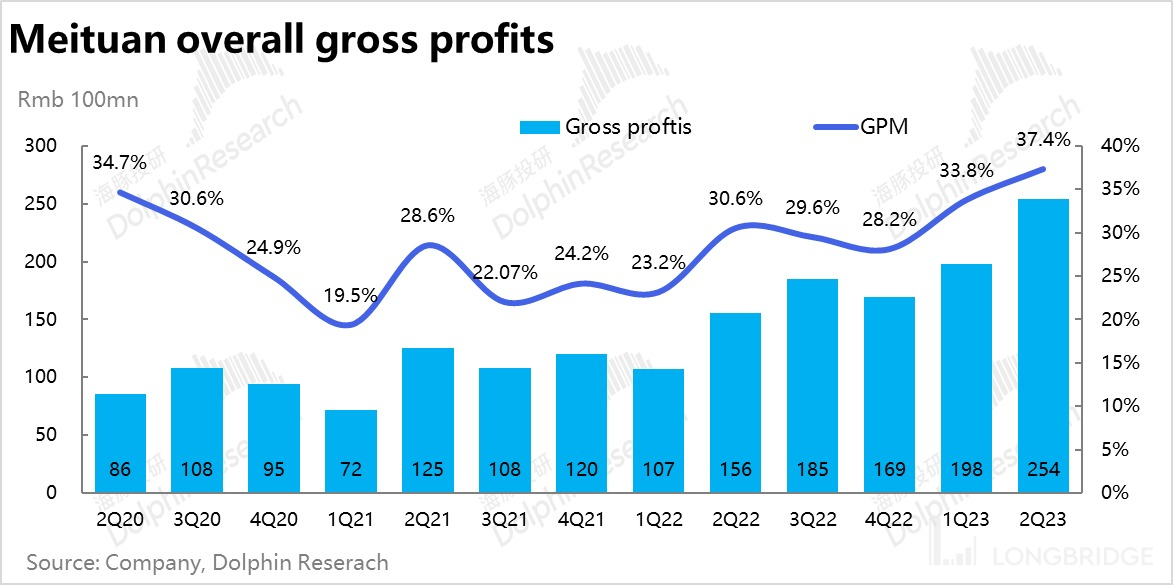

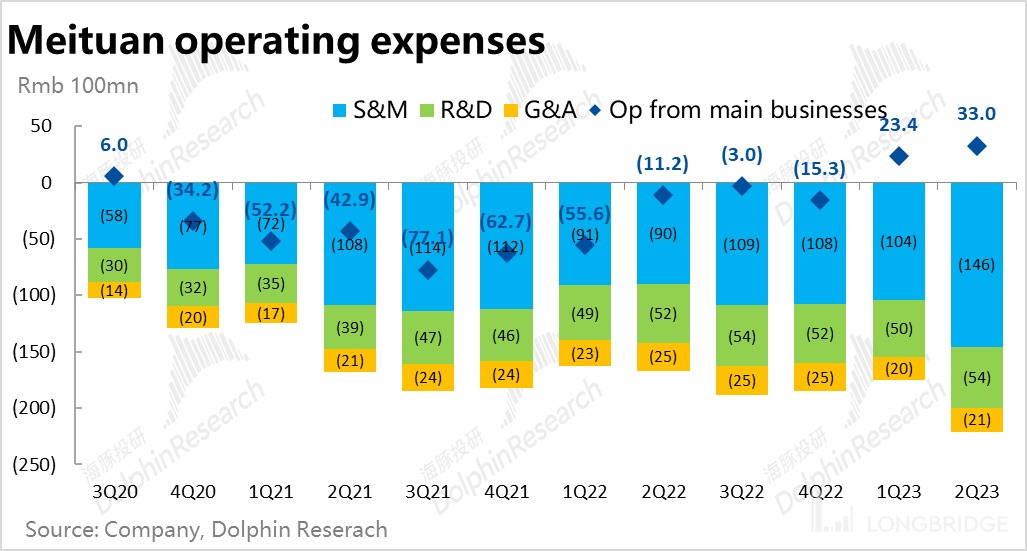

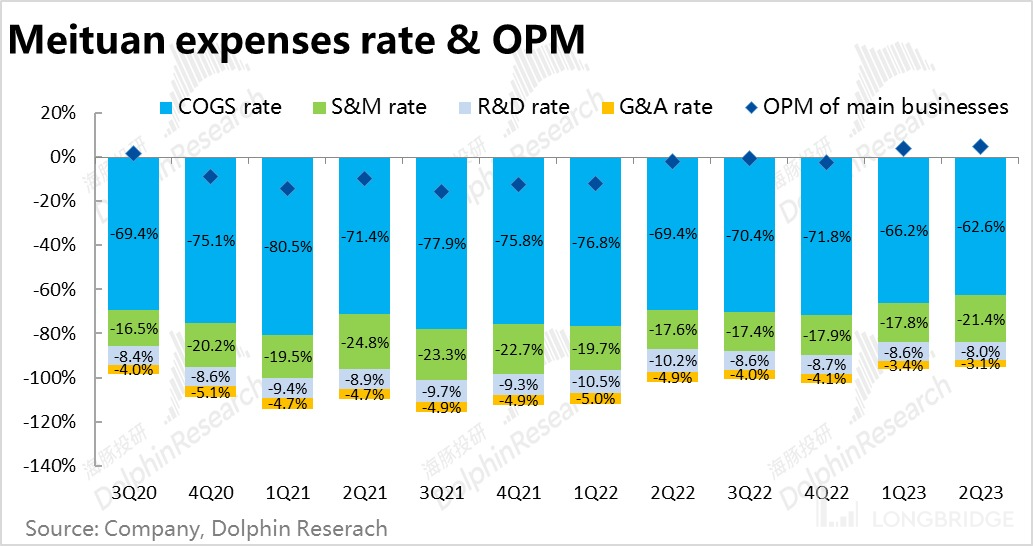

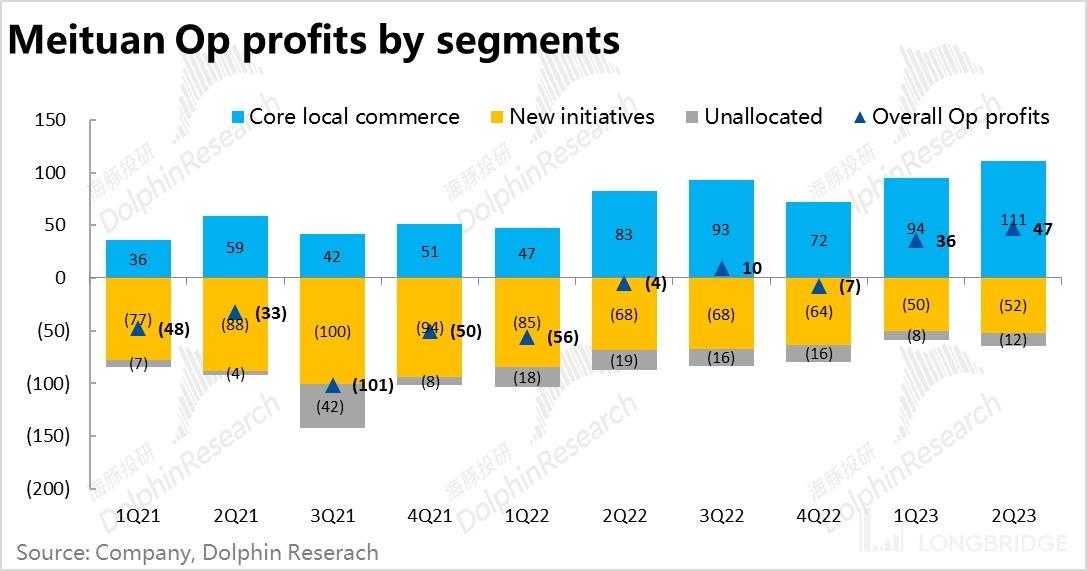

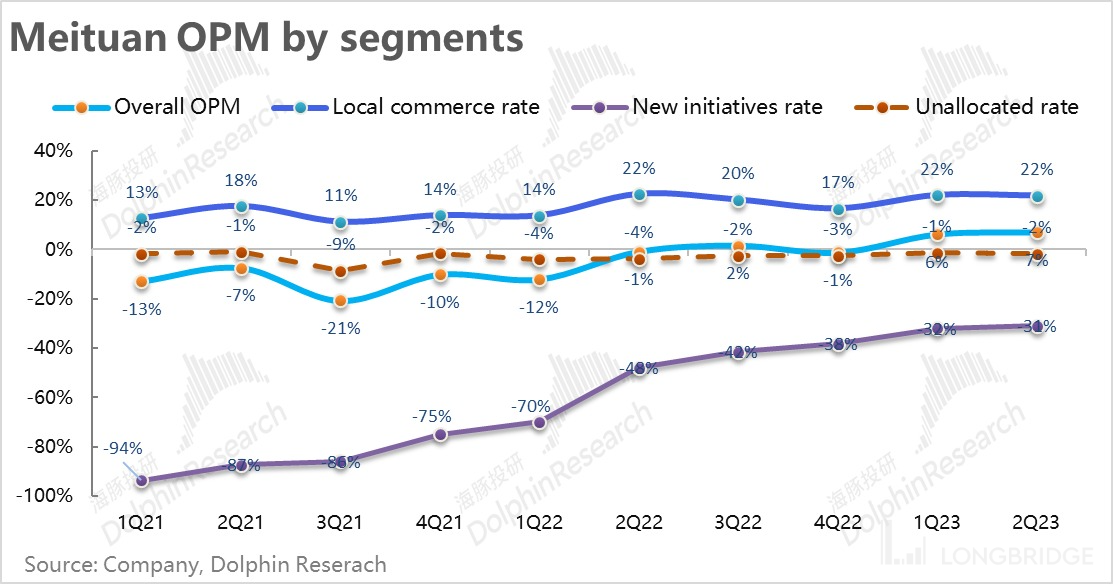

After the Hong Kong stock market was held on August 24, the US group released its financial report for the second quarter of 2023 * , * the key points are as follows: * * 1. It is also revenue in-line and profits are booming, but this time it is different: * * look at the overall performance first, * * the total revenue for this quarter is 68 billion, up 33% year on year, slightly higher than the company's previous guidelines and market expectations, but the gap is small. * * But * * The overall operating profit reached 4.7 billion yuan, far exceeding the expected 2.9 billion. **Overall seems to be the same as in the quarterly report, with flat revenue and exploding profits. However, Dolphin Jun believes that compared with the results of the previous quarter, the company's stock price did not rise but fell, and the market will give positive feedback to Meituan this time. 2. In-store-the worst days of competition are (temporarily) over?: Since the fourth quarter of last year, TikTok's erosion of Meituan in the in-store business (especially advertising revenue) has been the core issue that the market is most worried about for the company. The biggest highlight of this earnings report is that the revenue (especially advertising revenue) and profit of the store business exceeded expectations at the same time. **Specific to the results, the second quarter as the" post-epidemic era "of the first full holiday season, although the market has been quite high expectations for store and wine travel, but the actual performance is still strong beyond expectations. This quarter, the total turnover (GTV) of the US group's store-to-store business (meal, comprehensive and wine tour) increased by more than 120 percent year on year. On revenue, commission income from the local business sector reached 18.4 billion, up nearly 48% year-on-year, about 17.4 billion higher than market expectations. Advertising revenue also reached 10.2 billion yuan, up 40% year-on-year, also higher than the expected 9.7 billion. It can be seen that the previous three consecutive quarters of advertising revenue growth has lagged behind commission revenue growth has been significantly reversed. This means that, at least in the second quarter, the erosion of the US group's advertising revenue has been significantly reduced. Although, in the second quarter of the industry's high business climate, the huge growth of the industry's broader market will weaken the impact of peer competition to some extent. But on the one hand, in response to the competition of the sound, the U.S. group after the first quarter to increase the discount rate of group purchase coupons, to give merchants fee relief, to carry out video live broadcast and other positive measures * *. On the other hand, recent third-party research also shows that * * due to the flow distribution mode of chattering head merchants, it is difficult for merchants at the waist and below to survive on chattering, and a large number of them have begun to return to the US group platform. **** At the same time, the company has said that because it will increase investment to cope with competition, it is expected that the profit margin of the store business will drop sharply from 48% in the first quarter to about 30%. In reality, however, the local business sector's operating margin was 21.8 per cent, a slight decrease of only 0.2pct from the previous month, **far from falling as sharply as guided. * * The combination of accelerated advertising revenue growth and higher-than-expected local commercial profits * * * implies that although the competition in the store-going business of tremolo (and perhaps other platforms) is likely to continue for a long time, the speed and extent of erosion of the US group may not be so serious under the counterattack of the US group and after the initial bonus period of tremolo (other platforms). * * * * 3, home-take-out brother is still many, but the performance is not surprising: * * after the full liberalization of the offline economy, * * the other side of the strong travel demand is the decline of the "home economy", * * so whether it is catering take-out or flash shopping business did not benefit in this quarter, the performance was mediocre. Specifically, this quarter * * is the total quantity of about 5.4 billion orders, with a daily average of about 59 million orders * *. Due to the low base in the special environment last year, the year-on-year growth rate accelerated significantly to 32%. However, from the perspective of poor expectations, **the actual single volume is exactly in line with the company's earlier guidance and market expectations and is not surprising. * * At the same time, it is worth noting that the growth rate of the catering market revenue in the second quarter also reached 30%, * * the growth rate of the US group that is matched with single volume has no obvious lead compared to the growth rate of the catering market. I'm afraid it needs careful thinking about how much room there is for food and beverage takeout to further increase penetration. On the other hand, the downward trend in the average revenue of the US group that is to be distributed continues. * * This quarter * * Meituan's distribution revenue was 20.4 billion yuan, a growth rate of 27.7, but lower than the 32% growth of single volume. * * If we assume that the proportion of self-employment in the US group remains unchanged for all ready-to-match orders, the calculated * * single average distribution revenue fell by nearly 5% this quarter from the previous quarter. (According to Dolphin Jun's calculation, it has fallen by 3% month-on-month in the first quarter). Dolphin Jun believes that **the year-to-date large increase in the supply of takeaway brother, resulting in capacity from shortage to surplus is the main reason for the continued decline in the amount of single-average distribution. However, the company may also have increased the freight relief for competitive reasons. However, the decline in distribution costs should still be higher than the decline in average revenue per unit, and the probability that the gross margin of Meituan's distribution business has not declined, and may even increase further. * * * * 4, the home economy is declining, the growth of new business and the reduction of losses are mediocre: * * due to the high demand for "food hoarding" under the special environment last year, offline shopping is more convenient this year. **The new business segment, which is dominated by Metuan Preferred (community group buying) and Metuan Buying (self-employed front positions), performed flat this quarter * *. Specifically, new business revenue 16.8 billion this quarter, with year-on-year growth falling significantly to 18.4 per cent, in line with market expectations. And while revenue growth has slowed, **the progress in reducing losses has not been impressive. * * This quarter's operating loss was 5.2 billion yuan, and the loss rate narrowed by only 1pct month on month, which was also not better than market expectations. According to the company's explanation, **the main reason is that the decline in revenue from the community group buying business has led to dieconomies of scale, while the easier loss of fresh food in summer and higher cold chain distribution costs have also dragged down profits. * * * * 5, marketing expenses skyrocketed, why profits still exceeded expectations: * * cost level, * * this season's marketing expenses as high as 14.6 billion, an increase of about 40% from the previous quarter, marketing expenses accounted for 21.4 of revenue, has been close to the 21 years when the 100 group war community group purchase investment. It can be seen that in order to cope with the competition, the US group has indeed increased subsidies and promotion costs significantly. So why does Meituan's profit still exceed expectations? Because, Meituan's gross profit this quarter is 25.4 billion yuan, higher than the expected 22.3 billion, and the gross profit margin is also as high as 37.4, a record high. **On the face of it, the gross margin exceeded expectations due to 1) the fact that the business of going to the store exceeded expectations and going to the home and grocery shopping was relatively weak, making the high gross margin commission and advertising revenue in the revenue structure higher than expected. What's more, for businesses with almost zero marginal costs such as commissions and advertising revenue, incremental revenue can basically be fully converted into profits, and 2) the abundant supply of takeaway boys leads to continued improvement in the gross margin of the distribution business. * * But the more essential reason is that the competition in the store business in the second quarter was not as fierce as the management originally expected. * *! Longbridge Dolphin Jun's View: **As mentioned earlier, while this quarter's earnings report looks similar to last quarter's at first glance, with flat revenues but higher-than-expected profits, the internal structure of the earnings report is the complete opposite. The core shortcomings of last quarter's earnings report were the rapid slowdown in advertising revenue growth and management's pessimistic guidance on future profit margins. **** The internal structure of this quarter's earnings report is that the revenue from the store business (mainly advertising revenue) exceeded expectations, and even if the investment increased, the profit margin showed no signs of deterioration. Therefore, compared with the last quarter's financial report clearly points to the deterioration of competition in the store business, this financial report points to the improvement of the competitive landscape. **** Although Dolphin Jun admitted that this quarter's special to-the-store wine and travel industry's extremely high business climate may have weakened the impact of competition. However, at least in the summer vacation season in the third quarter, the high demand for wine travel to the store is still continuing, so the current performance trend of the US group will probably continue. **** Therefore, at least in the fourth quarter of the market can once again verify the sustainability of travel demand, the valuation of the United States group is very likely to be from the current undervalued level, to neutral valuation interpretation. * * * * 1. Meituan's financial report how to start * * Meituan from the second quarter of 2022 once again significantly adjusted the financial report disclosure caliber, so Dolphin Jun first to give you a brief introduction to the latest business classification of Meituan, of which red is from the original innovative business into the core local business. The strategic ideas and future ideas revealed behind the company's adjustment of its financial report can be referred to the previous analysis **** Meituan's domineering hand-in? That is, matching is the real soul **" **.! image/x-emf picture format is not supported * * 2. home is better to go out, and the home business will hand in the papers as scheduled * * first look at the core home business (take-out and flash purchase) of the us group. this quarter's * * is a total of about 5.4 billion orders, equivalent to a daily average of about 59 million orders * *. Due to the low base in the special environment last year, the year-on-year growth rate accelerated significantly to 32%. However, from the perspective of poor expectations, the actual volume of this quarter compared to the company's earlier guidance and market expectations are exactly the same, no surprise. Dolphin Jun believes that after the full liberalization, the other side of the strong demand for going out is the "home economy" of the decline, **so whether it is food and beverage takeaway or flash shopping business in this quarter did not benefit, it is reasonable. However, it is worth noting that in the second quarter, the growth rate of food and beverage market revenue reached 30%, **this quarter, the U.S. group's instant distribution volume growth rate compared to the food and beverage market growth rate has no obvious gap. I'm afraid it's not very optimistic how much room there is for food delivery to further increase penetration. * *! **On the other hand, the downward trend in the average revenue of the US group's instant distribution orders continues. * * This quarter * * Meituan's distribution revenue was 20.4 billion yuan, a growth rate of 27.7, which was lower than the 32% growth of single volume and about 1% lower than expected. * * In the first quarter of this year, we have seen the US group's single-average distribution revenue begin to decline (by about 3% month-on-month, according to Dolphin Jun). And if we assume that the proportion of all ready-to-match orders owned by the U.S. group remains unchanged, it means that * * single average distribution revenue fell by nearly 5% this quarter. Dolphin Jun believes that the year-to-date large increase in the supply of takeaway brother, resulting in capacity from shortage to surplus is the main reason for the continued decline in the amount of single-average distribution. However, whether the company has increased the freight reduction due to competitive considerations may also be one of the reasons. However, Dolphin Jun still believes that the decline in distribution costs is higher than revenue, so although the average revenue per unit has declined, the probability that the gross margin of Meituan's distribution business has not declined, and may even increase further. **As long as the supply of takeaway boys remains plentiful, the above benefits should continue.! 3. to the store: the boom, the worst days of competition are over? Although the performance of the home business was not outstanding, the second quarter, as the first full holiday season in the "post-epidemic era", maximized the pent-up travel demand of residents. Whether it's dining at a restaurant, wine travel, or all kinds of attractions, concerts, to the comprehensive consumption is quite hot. The company has already guided the total transaction volume (GTV) growth rate of all in-store business (to meals, to comprehensive, wine travel) in this quarter to be higher than 100, while the actual growth is more than 120, and continues to exceed expectations in high expectations. * ! * * Due to the extremely hot demand and prosperity of the entire in-store wine and travel industry, the US group's in-store business has also delivered quite gratifying answers this quarter. * * Specifically: * * 1) * This quarter * * Commission income reached 18.4 billion, up nearly 48% year-on-year, higher than the market expectation of about 17.4 billion * . The commission income of the takeaway and flash business is anchored by the single volume, and the growth should also be around 30%. Therefore, the strong performance of the store and wine travel business is the main driver of growth. (The company also pointed out in its quarterly report that the revenue growth rate of the store's wine tour was between 56% and 58%) * * 2) * Reflecting the traffic distribution and promotion ability, the revenue of * * advertising and marketing was as high as 10.2 billion yuan this quarter, * * breaking 10 billion yuan for the first time under this caliber, * * also higher than the market expectation of about 9.7 billion. And more critically, the gap between advertising revenue and commission revenue growth narrowed sharply to just 7 percent this quarter. Reverses the situation that the growth rate of advertising revenue based on information distribution has lagged behind the growth of commission revenue in the previous three quarters. This means that, at least in the second quarter, the advertising revenue of the US group did not reflect the obvious erosion of the sound from the sound. Although the second quarter of the high business climate, the industry's considerable increase in the market to a certain extent will weaken the impact of peer competition **(if everyone can enjoy considerable growth, naturally will not tend to each other" grab food "). But from another angle, it may also mean that the most serious stage of the impact of the sound on the United States has passed. **** On the one hand , in response to the competition of trembles, Meituan has taken a variety of positive measures such as increasing the discount rate of group purchase coupons, giving merchants fee reductions, and launching live video broadcasts. On the other hand, * * recent third-party research also shows that due to the flow distribution mode of chattering head merchants, it is difficult for merchants at the waist and below to make profits on the chattering platform, and a large number of them have begun to return to the US group platform. Therefore * *, whether due to the response of the US group itself to increase investment, or the return of merchants after the bonus period on the tremolo platform, it means that although the competition from tremolo (and perhaps other platforms) in the store business is likely to continue for a long time, the speed and extent of erosion may also have slowed down. * * * * 4. is also affected by the "home economy" decline, new business growth, loss reduction performance is mediocre * * * * * due to the second quarter of last year when the "hoarding" peak, and this year to go shopping is also more convenient. The new business sector, which is dominated by Meituan Preferred (community group buying) and Meituan Buying (self-employed front position), performed flat this quarter * *. Revenue 16.8 billion in the quarter, with year-on-year growth slipping significantly to only 18.4 per cent, in line with market expectations. According to the company's explanation, the main drag is the U.S. group's priority business revenue fell month-on-month, but the taxi business to give up self-management to the aggregation mode should also be a drag.! And while new business revenue growth is flat, **the progress in reducing losses is not outstanding. * * This quarter realized an operating loss of 5.2 billion yuan, with the loss rate narrowing by only 1pct month on month, which did not exceed the market expectation. According to the company's explanation, **mainly due to the decline in revenue from the community group-buying business, which led to dieconomies of scale, while the easier loss of fresh food in summer and higher cold chain distribution costs were also drag factors. * *! * * 5. revenue grew steadily, to the store business to help profits hit a new high * * overall performance, * * this quarter's total revenue was 68 billion, up 33% year-on-year, slightly higher than the company's previous guidelines and market expectations, but the gap is very small. **While store-to-store revenue exceeded expectations, it was more than half offset by the drag on distribution revenue and new business.! 2) However, the performance at the profit level was quite gratifying, * * this quarter achieved a gross profit of 25.4 billion yuan, with a gross profit margin of 37.4 per cent, a record high. Gross profit was also significantly higher than expected 22.3 billion. * * Dolphin Jun believes that the main reasons for * * gross profit exceeding expectations are * *: the proportion of high gross profit in-store advertising commission revenue increased in 1., while the proportion of low gross profit distribution revenue and new businesses such as grocery shopping decreased, 2. the supply of takeout brothers was abundant, and the gross profit margin of distribution business was also improving. 3., according to the company's disclosure, the gross profit of self-operated retail (mainly grocery shopping business) commodities also increased this quarter.! **3) At the cost level, the high cost of sales indicates that Meituan has indeed significantly increased its subsidies and promotion efforts. Marketing expenses this quarter are as high as 14.6 billion, up about 40% from the previous quarter. Marketing expenses also accounted for 21.4 percent of revenue, returning to the marketing rate level of more than 20 percent during the 21-year community group buying war. **** As for management expenses and research and development expenses of 2.1 billion and 5.4 billion respectively, there was no particularly significant increase from the previous quarter. Although the company's overall revenue increased significantly in the quarter, but in addition to marketing costs are still relatively cautious. * *! ! 4) guided profit decline did not occur. * * In the first quarter financial report, in the face of aggressive competitive pressure, * * the company's management has said that the second quarter will significantly increase investment, so the operating profit margin of the wine travel business to the store will drop sharply from about 48% in the first quarter to nearly 30%. But while it is true that marketing expenses have increased significantly, the local business segment actually has an operating margin of 21.8 per cent, a slight decrease of only 0.2pct from the previous month, far from the sharp decline as guided. The reason for this is that, on the one hand, the revenue from the store-to-store business this quarter was stronger than originally expected, and the revenue that exceeded expectations can basically be fully converted into excess profits. In addition, Dolphin Jun speculated that the management originally expected that it might be enough to increase investment to keep the pattern of the US group from deteriorating, but there were actually signs of marginal improvement. So actual profits are not as bad as originally feared. In the end, core local business's operating profit was 11.1 billion, about 1.6 billion higher than expected, while unallocated expenses at the group level were 1.23 billion, also about 0.3 billion less than expected. As a result, the overall operating profit of the group reached 4.7 billion yuan, significantly exceeding the expected 2.9 billion.! ! * * Dolphin Investment Research Past [Meituan] Related Research * * * Financial Report Season: * * May 25, 2023 Telephone Conference "Meituan: Confident in 2023 Consumption Recovery, Hope to Fly in the Wind" May 25, 2023 Financial Report Review "Exploding Takeaway Brother, Can You Help Meituan?" March 25, 2023 Telephone Conference "Meituan: full of confidence in the face of competition?(4Q22 Call Minutes)" March 24, 2023 Financial Report Review "Meituan: Kingdom Efficiency Still Reliable but Not" Iron Wall "" * * November 25, 2022 " * * Meituan: Competition in Stores Has Unique Differentiation, Will Communicate Meituan Value with Naspers (Minutes) * * * * * * * * November 25, 2022" * * Meituan: Profits Explosive, why is faith "bad"? * * * * * * August 26, 2022 " * us group domineering hand in papers? That is, matching is the real soul * * * * * * August 26, 2022" * * US group: instant retail profit exceeding the standard is the stimulus of the epidemic, it will go down in the third and fourth quarters * * * * * June 2, 2022 "store loss, hotel worst, flash purchase outbreak, consumer voucher valid"June 2, 2022 "It's enough for the US delegation not to drop the chain, it's more important to return blood quickly" March 25, 2022 Everything Home: Flash Purchase is the new star sea of the US delegation? (Minutes of Telephone Meeting) "March 25, 2022" Meituan 2021 Q4 Performance Telephone Meeting " * Depth: * * * * June 2, 2023" * * * * * Facing the trembles, Meituan can't make Ali's mistakes again * * * * * * * * December 16, 2022 " * * * * finally let go, can Meituan return as king? * * * * * * * * September 22, 2022 * * Ali, Meituan, Jingdong and Pinduoduo all resigned? Also get big luck * * * * * April 22, 2022" us group, jingdong, with what stock fight but outstanding? "April 13, 2022" to cycle "decay", how much value do Ali Tencent have left? "October 22, 2021" Pay Fines, Get Social Security, What Belief Does the US League Have? "September 22, 2021" kill crazy Ali, meituan and pinduoduo, is there a real barrier after the e-commerce traffic melee? "Risk Disclosure and Statement for this article: Dolphin Investment Research Disclaimer and General Disclosure

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.